If you want a secure income for the rest of your life, you have a few options:

An annuity - perfect, but very expensive recently due to low interest rates. Takes care of longevity risk.

Government bonds. You can ladder your bonds. Again, was expensive recently due to low interest rates.

Real estate. Has benefits of inflation protection.

Dividend stock portfolio (tax inefficient in Switzerland)

Speculative/Growth portfolio. Too volatile on its own but if you tamper down the volatility with 1-3, then you can offset the low returns of 1-3 and mitigate the sequence/volatility of a growth portfolio.

I’m not sure if I’ve missed anything, but I’m personally going for a bit of everything.

I’m doing point 2 (2nd pillar) involuntarily.

I’m actively doing 3-4-5 with a 50-10-40% split for now (roughly), that will slowly turn 60-30-10% by the time I’m 55-ish, for the exit strategy.

At least that’s the plan now. Going into real estate has left a LOT of money on the table since my first deal in 2005, but at least I had a place to sleep

I haven’t check annuities much but as you mentioned they seem to be too expensive. More than the second pillar.

Isn’t second Pillar a “form” of Government bonds?

Does it? better than stocks?

And are you talking about REITs or real real estate?

In what way dividend stocks are different from the non-dividend ones? Dividends are not free money. They reduce the stock price when they are paid. + You are being taxed on marginal rate!

I don’t see the reason behind focusing on Growth stocks (vs market cap or factor tilt)

If you only consider return and risk on the surface, kind of. But inside the investment strategy is RE, bonds, stocks etc. During accumulation phase, it is basically a mixed asset fund, with a guarantee (not sure however what happens if a fund really goes down the drain)

If you check it out as a pension (instead of capital withdrawal), it would turn into an annuity.

Yep, this what I meant. From return and risk point of view it is kind of a government Bond. If you do not cash it then it will turn into annuity.

I checked the underlined assets: a mixture of domestic and international Bonds, Stocks, Real estate, gold and Private Markets!

The not so funny “fun fact” is that the last 5 years it under-performed VT by a factor 3+. And at the end it provided only half of that performance to the owners! (something like 1-1.5% per year)

So I think it make sense not to bother at all with the underline investments of the 2 pillar fund and just consider it as a safe government bond…

It’s not quite as bad. The performance of VT between end of 2018 and end of 2023 was 8.36% p.a. in CHF. The average pension fund performance was 3.56% p.a. according to Pensionskassen-Performance | UBS Focus. Could certainly have been better¹ but they obviously can’t invest it all in the stock market. And the negative interest era (+ the interest rate increase to move back to positive interest rates) hurt pension funds with their bond allocations. Hopefully, that era is over.

¹ E.g., the Pictet LPP 2015-60 index (60% stocks) averaged 5.07% p.a. in the same time span.

First, a strategy doesn’t need to be fixed in terms of asset allocation. Personally I plan to steadily reduce my stock allocation and move it to cash/bonds at one point.

Second, I believe that if the US market crashes by 30-50%, most other markets will crash as well due to the interconnectedness of our world, maybe not as hard, but they will for sure be hit as well.

Third, by changing your strategy you might as well miss an unseen 20 years bull market in the US or you could change into a market that crashes hard, while the US still performs good or any other of 1000s of scenarios.

Fourth, your strategy should fit your risk profile, if you can’t stomach such a massive crash, you need to adjust your strategy.

My main concern is not so much about the underperformance due to the asset allocation but about not passing the full performance to my personal assets.

I am not an expert about what happens in the backend but I think part of my money is used to finance existing pensioners’ relatively high and locked conversion rate.

Combine that with the chance of FIRING/retiring abroad with 40+% tax rate and you understand why 2nd pillar doesn’t seem the greatest option for me…

Yes, that misappropriation is really bad. The pending BVG reform will at least slightly improve it by reducing the BVG conversion rate from 6.8% to 6.0%, however, I suspect the majority will vote against it.

There are infinite scenarios and we all agree that we cannot predict the future.

What we know empirically - though with some noise - is that:

High Valuations → Low Expected Returns and in some cases big crashes

Common US Cap weighted indexes → Currently Very High evaluations

So the logical question emerges: By accepting the above, is there something we can do to probabilistically improve things?

e.g. tilt towards lower evaluations (Lower US part %, tilt towards Value, use home bias, something else …)

As very clearly some noted, the problem is higher when you have less than 10-15 years to Fire/Retire and your already invested capital if far bigger than the one that will be invested the next years.

Another way how you can mitigate both the US Tech MegaCap Risk as well as the current, excessive weight of US Shares in current Market Cap:

The return is slightly below Market Cap return. If you scaled this Portfolio down and augmented it with an equal Nasdaq 100 ETF, this to get the US back to 60% weight - you would probably get the same return than the world - but withouth the current mega cap risk we face right now and as well at a much lower PE valuation.

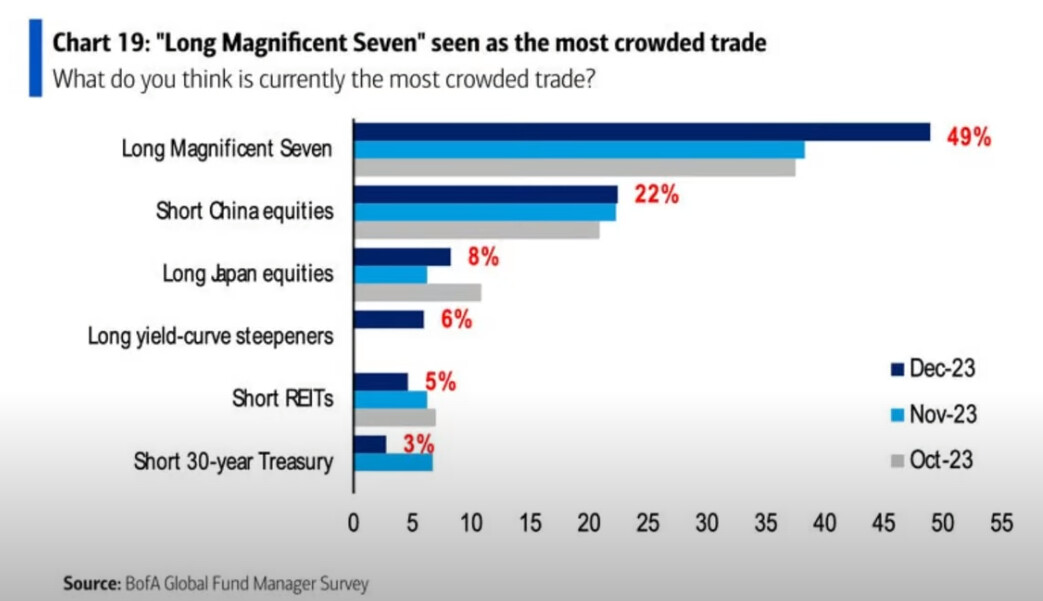

Do we really need to “mitigate” the impact of the Magnificient Seven?

They are there and expensive for a reason, what would be the trigger for them to lose their competitive advantage against the other players in the market?

I think one reason might be to avoid too much concentration in a single stock. So I could see the desire to cap any single holding to a max %. e.g. VTI has AAPL as 6.1% of the ETF. VT 3.7%.

Just did another Curvo with a “US & Tech Corrected” Equal Weight vs. VWRL. Curvo unfortunately doesn’t cover the Equal weighted Nasdaq 100 ETF; but the approximation should be relatively close:

Conclusion: Equal Weighting gives you nearly the same return than Market Weighting - but without the Magnifient 7 risk. Personally, I would probably not offset the US & Tech reduction resulting from Equal weighting - yes that would cost some performance but as well adds portfolio resilience.

Question: Is anyone else interested in Equal Weighting?

Thought hard about going with RSP+VTWO mix but in the end, too much micro management for the overall benefit. Rather keep with VTI only and accept that 2-3 of the Mag7 or Super6 correct hard (deserved) in next ~18months.

If one is going to actively not follow the index I believe there are superior approaches then under-weighting companies whose primary listing happens to be on the US stock market. Similarly the stocks clumped together by the press as “Magnificent Seven” each have very different characteristics

Tracking Difference of Vanguard’s Equal Weight Product is at about 0.1% - 0.2% p.a… To be honest, they could probably beat the Benchmark by 0.2% p.a. as they can deduct some of the Net Dividend. So net net, they probably lose 0.1% p.a. to trading (+0.2% post Tax Effects, minus 0.3% TER => -0.1% vs the -0.1 to -0.2% they achieve).

The only problem with Equal weighting is that there is no sensible Large Cap Equal Weight ETF. The Netherlands based ESG Equal Weight is mainly a problem from a tax point of view. The ESG Exclusion is probably not ideal but EMT and diversification ensure you receive the same return than if you equal weighted all large caps. The only Problem there is the NL Tax Location.

Long story short: Equal Weight is investable, but not perfect

I guess I do a bit of 3. I hold 75% VT, 15% AVUV, 10% AVDV. Mostly I do 1. and just don’t care though. Obviously a lot people think US companies are still worth investing in. Going against the market and reducing my US exposure would go against the entire point of passive investing, plus I just don’t have time or interest to track the CAPE of different regions. I use it to estimate expected returns, that’s about it.

Also FYI 2. won’t really help you as the Swiss stock market is also somewhat expensive (17.73 P/E 16.75 Fwd P/E 3.52 P/BV and most importantly half the index is three companies in a trench coat pretending to be a diversified stock market. Holding SPI is IMO fairly dangerous, because it offers much greater risk for no additional reward (VT is more tax efficient and cheaper to hold).

I am telling myself for years by now that NL gave me issuer country diversification (lets say IE blew up due to whatever reason). Yet, I didn’t buy myself yet as I as well can’t convince myself and the tax drag was just real. The only reason why I am thinking about buying again is as large caps currently return more than small cap…

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.