Actually I don’t have an account yet. That’s why I cannot check

But thanks for info

I don’t change strategies once set but the portfolio can still have turnover due to rebalancing which is driven by strategy . And everytime there will be cost to transact

The only scenario when you won’t have turnover is when you have only one fund

There is a section about conforming to BVV requirements, but nothing about using the tax treaty. There might be something in the prospectus. But I don’t have that.

I actually already replied to you less than 2 weeks ago:

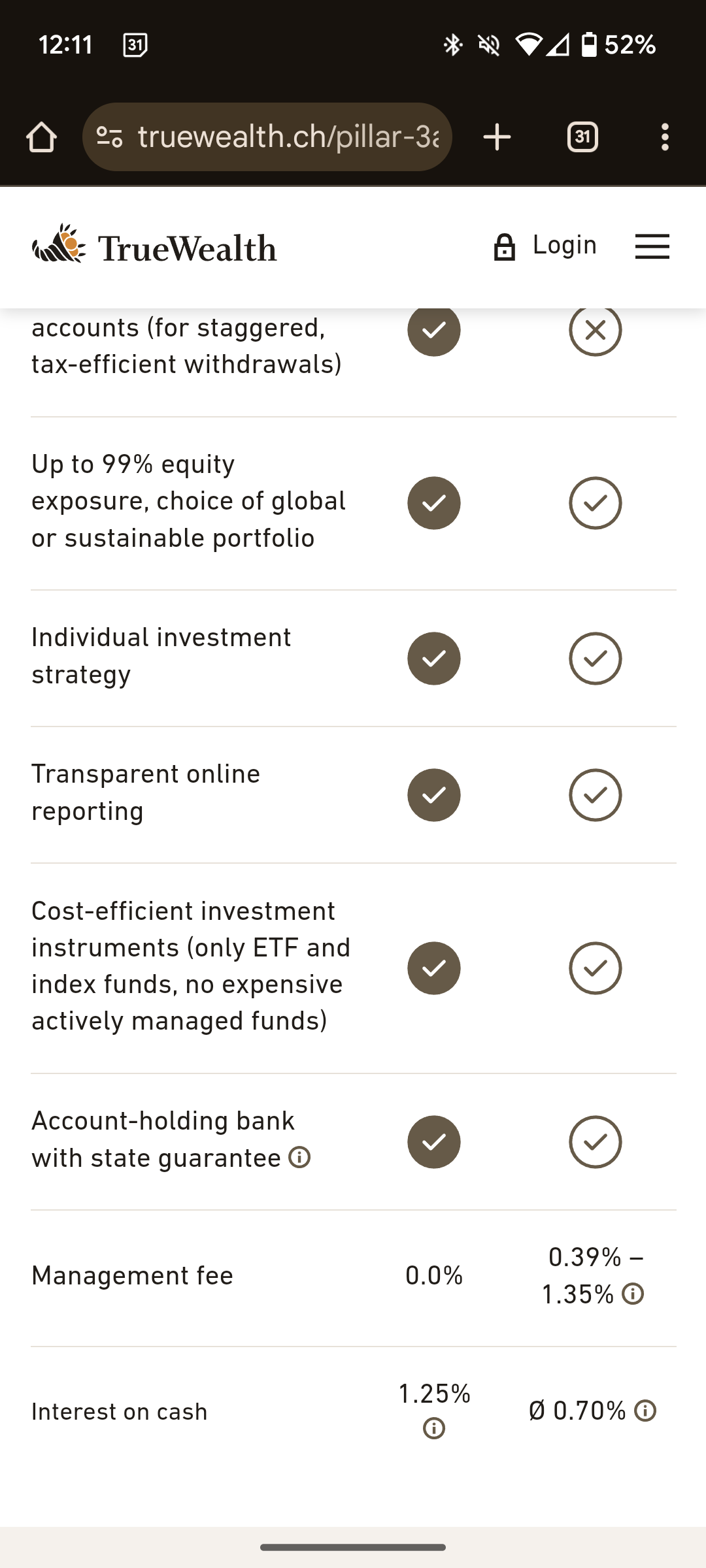

the fund on Swiss stocks is one of few (4) instruments that make sense to me.

That came from my analysis of what kind of portfolios you can construct on True Wealth.

There are some efficient instruments for 3a. The fund on Swiss stocks is one of them, but I don’t invest in Swiss stocks in 3a.

The fund with Japan stocks is not exempt from withholding tax, which immediately make it more expensive than Japan funds in Finpension, despite the fee of the latter.

The US fund is exempt from withholding tax. It is good by itself, but not as a part of a portfolio, because US is the least preferable for holding in 3a.

My goal was actually to max MSCI EM IMI ETF holding, but because of the diversification rule, I had to dilute it with the US fund. I wanted to stay with max stocks in 3a, and that’s what everyone should do. Because US has low dividend and for MSCI EM IMI ETF you only get an advantage not to be taxed on income, all in all it came out hardly more efficient (cheaper) than Finpension portfolio with a fee, but where I can use max amount of dividend-rich funds.

I don’t know when I will be able to update my table for portfolio analysis, sorry. Until then you will have to check it yourself or believe my word, I am afraid.

That was a part joke. True Wealth 3a is only good if you use it to invest into funds on Swiss and US stocks in 3a, which I don’t.

Since you are using mixture of ETFs & Funds for portfolio construction, which one of your instruments are tax efficient and which ones are not with respect to tax treatment in foreign jurisdictions

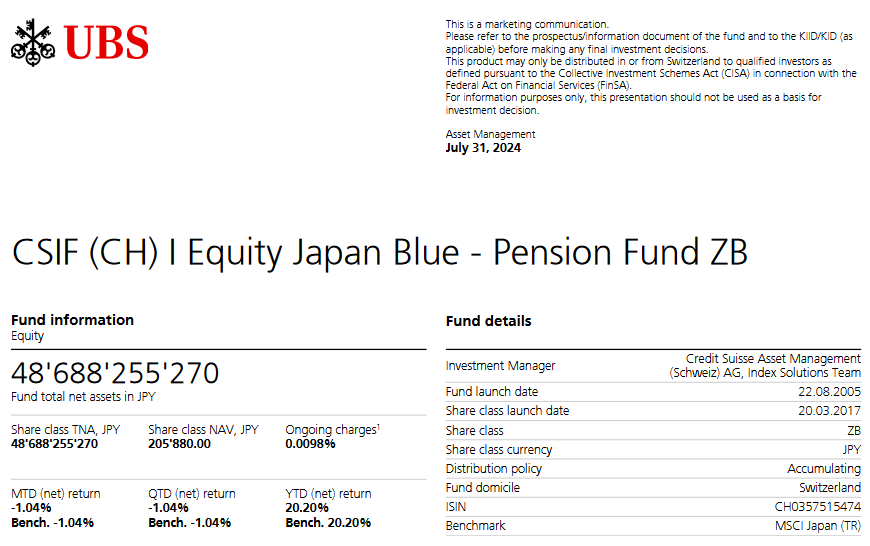

Are you sure that’s a pension fund? Here’s the one used by finpension as comparison. Notice the difference in index (net return vs. total return), and also that for the finpension one, fund and index performed 0.4-0.5% better each year.

I just checked the factsheet and it said the fund is for BVG purposes. But I will check later what exactly is this fund doing for BVG if not getting tax benefits.

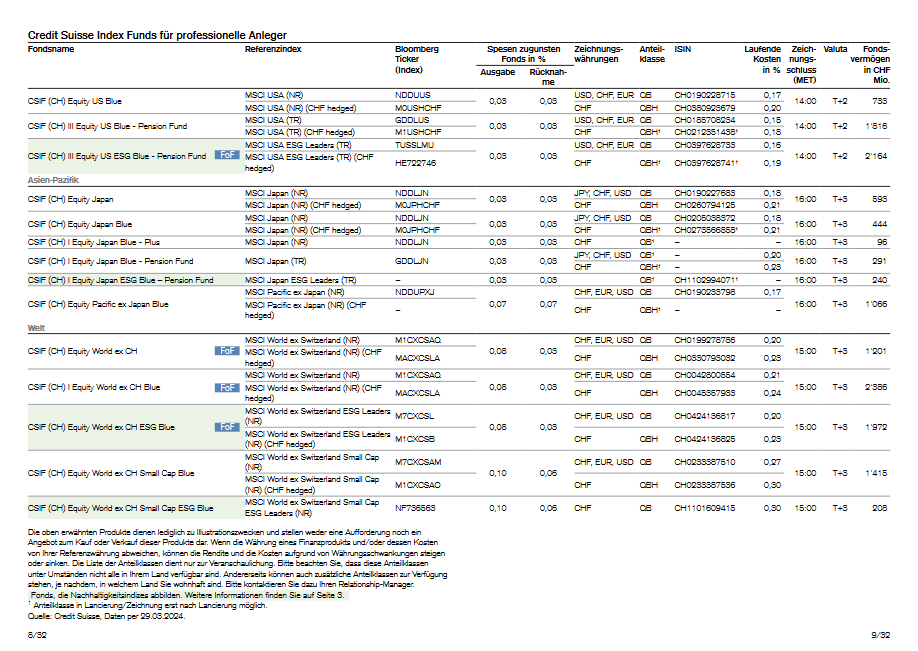

The fund (from UBS before CS merger) Truewealth should have used would be this one “UBS (CH) Institutional Fund 2 – Equities Japan Passive II I-A1”. The benchmark is MSCI Japan (gross div. reinv.)

For US and REIT, a tax-optimized Pension Fund is available in our instrument universe.

For EU, Switzerland, UK and Pacific ex Japan, we are not aware of any more tax-efficient instruments than ours.

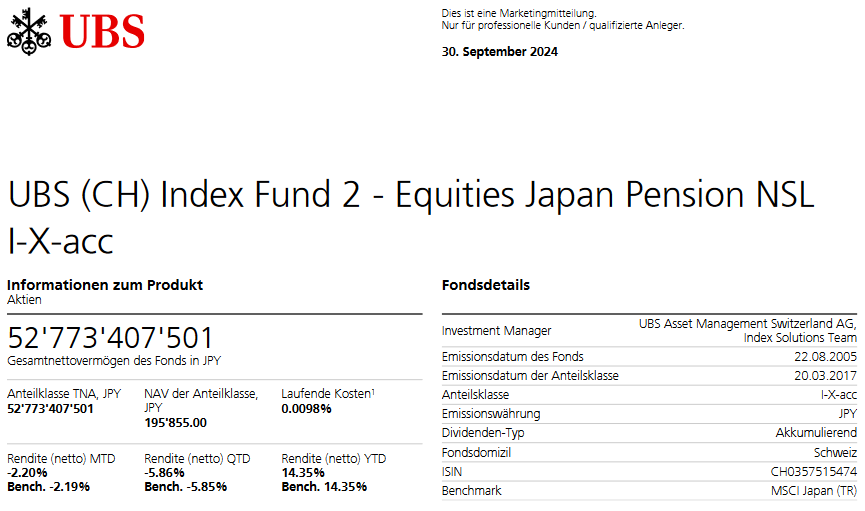

For Japan, which generally represents a relatively small portion of exposure, we currently use the fund visible in our sample portfolio UBS (CH) Index Fund - Equities Japan I-A-acc due to the lack of a dedicated Pension Fund QB share class (has not been launched yet). Link to UBS/CS index solutions product list.

We’re constantly monitoring the instrument universe and will replace an instrument if it is in the overall best interest of our clients and preserves our ability to select funds independently.

Art. 53 BVV 2 lists what investments are allowed in BVG. The note on the fund factsheet simply means that its holdings are permitted as investments in BVG. It has nothing to do with taxes.

I’m probably misunderstanding your answer, but VIAC and Finpension are using such “Pension Fund” funds. I have this in my portfolio this very instant. The ISIN is CH0357515474.

VIAC and finpension use zero-TER (ZB) fund share classes, which are only available to organizations with a contract with UBS (requiring payments, of course). TrueWealth presumably doesn’t have a comparable contract with UBS, so it can only use the QB (or FB) share class. And not all share classes are available for all funds.

I have no idea whether TrueWealth will move towards a similar contract or whether that e.g. conflicts with their goal of cost transparency or their preferred mix of fund providers.

Investors need to always try to figure out which fund is tax efficient and which one is not. Japan fund is not tax efficient. US fund is. But Hedged US ETF is of course not tax efficient as well.

Because of these inefficiencies, investor might need to try to balance across accounts (taxable accounts like IBKR, other 3a accounts). I think i can manage it but it can lead to complexities & I am losing interest

It would be best if there was a way to establish Total cost of investing instead of just average TER%

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.