Truewealth have (silently?) released their 3a offering.

What do you think about it? It touts 0% fees…

Truewealth have (silently?) released their 3a offering.

What do you think about it? It touts 0% fees…

And 1% interest on cash.

Interesting, would just require a deeper dive into their ETFs (and customizability) offering.

Interesting.

They invest via ETFs. That means no preferential treatment of L1 withholding taxes.

https://finpension.ch/en/etfs-and-index-funds-compared/

With a conservatively estimated TER 0.1%, dividend yield 2%, L1 tax of 12% for a whole world ETF you are already at 0.34% p.a. total costs vs 0.39% + L1 withholding tax for some geographic segments at finpension. Most probably not worth it. Maybe for Switzerland and Pacific ex Japan (very low L1 tax), but that would be an overoptimization from my point of view.

Anyway first I would like to see the list of ETFs that they invest into.

Investment-Regulations.pdf

The investment objective of securities savings is to diversify risk by means of passively managed funds traded on the stock exchange (exchange traded funds (ETFs)) or by means of passive open-ended investment funds (index funds)

Annex-to-the-Investment-Regulations.pdf

The foreign currency share amounts to a maximum of 65 %.

Does it refer to trading currency or fund currency?

Cost-Regulations.pdf

Early withdrawal for home ownership (per case) CHF 250

Exit from the Pension Foundation within one year of entry CHF 100

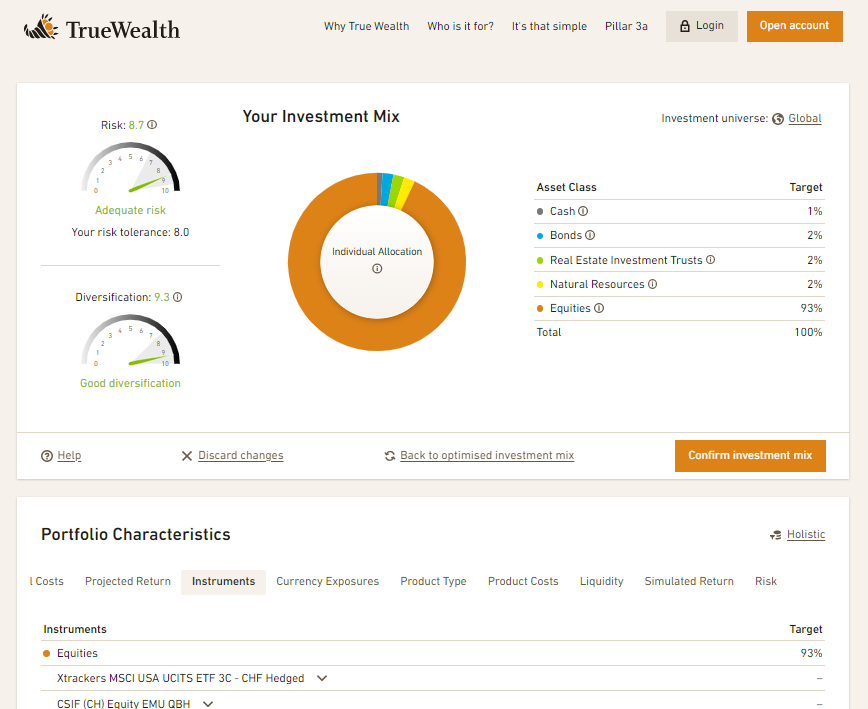

I am using their platform for the free portfolio management. I can share some insights in what they invest. Of course you are free to change the portfolio mix to change the ratio between countries you want to invest in.

Here’s a list (synthetic and physical ETFs):

Xtrackers MSCI USA, iShares SPI, iShares MSCI EM IMI, Vanguard Japan, are good.

Euro stoxx 50 is a too narrow representation of Eurozone market. Same for FTSE 100 and UK. Vanguard FTSE Developed Asia Pacific ex Japan includes South Korea, which is also a large part of MSCI Emerging Markets. And I don’t see a global Equity Fund.

My verdict is no. I have a better use for my limited amount of 3a money.

First, it’s excellent to have some competition in the market.

Buried in their Q&A, you can find an answer that relates to possibly introducing fees at a later stage. It sounds to me what we currently have is a teaser offer:

"The cost regulations of the 3a retirement savings foundation state that the Board of Trustees could introduce a management fee to a maximum of 0.225 per cent per annum on the securities portion.

Nevertheless, due to a contractual agreement between True Wealth and the Foundation, no management fee will be charged on the pension assets until further notice. If, contrary to expectations, the Foundation Board decides to introduce a management fee at the beginning of a calendar year (possibly at the beginning of 2024 at the earliest), we will inform our pension fund members of this in July of the previous year."

It could also be a way for them to attract new clients for their base product. Many non-financially-aware people nonetheless open 3rd pillar account(s) to save on taxes.

It might not the target audience of this forum, but this seems to be a great 3a solution for risk-averse people, and by a wide margin…1% interest on cash is at least 2 to 3 times higher than anyone else’s offering

Yes, 1% is really good.

I’m just afraid that is only a promotional offer for a short time.

After Investart, I take these too-good-to-be-true offers with a pinch of salt. Switzerland is a pretty small market, so you don’t have the critical mass factor which US services like Robin Hood, etc. benefit from.

That said, even if True Wealth does end up having a 0.225 fee, that’s still relatively cheap (just like Investart is still very competitive even after it introduced a fee). On the whole, I’m amazed at what is currently available on the Swiss market. These kinds of offers would have been almost inconceivable just 5 years ago.

One thing about the True Wealth pillar 3a: The retirement foundation which True Wealth partners with (Vorsorgestiftung 3a Digital) is in Basel which = high withholding tax.

That obviously only affects withdrawals when leaving Switzerland for countries without a relevant double taxation agreement.

Yes, I won‘t change as well.

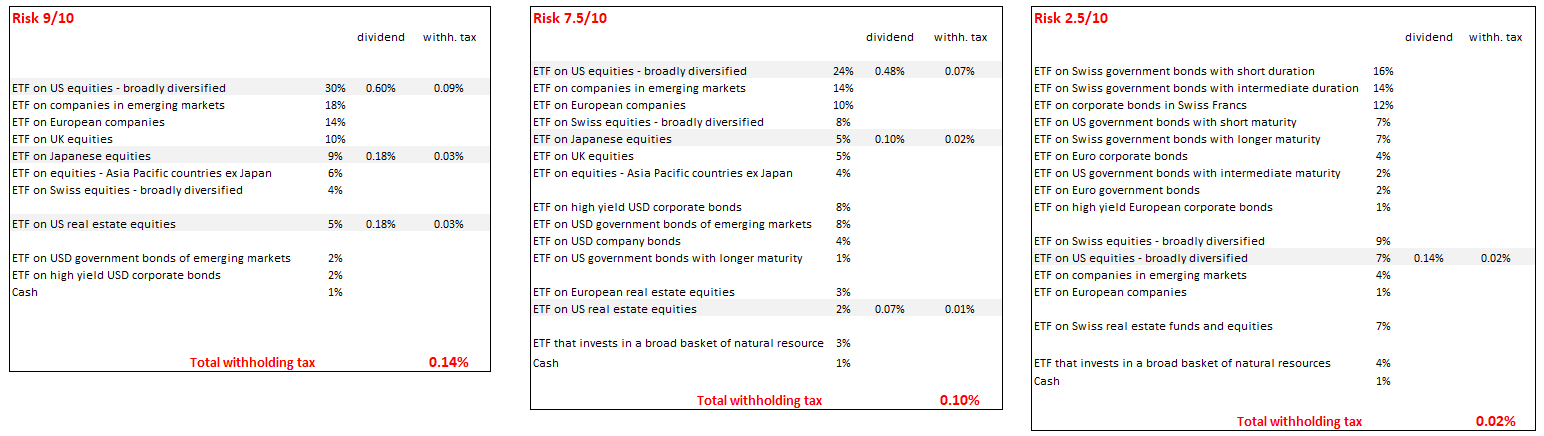

Withholding taxes on dividends apply to ETFs on equities and REIT from the US and Japan. Generally, for US equities, a withholding tax of up to 30% applies. Thanks to the tax domicile of our ETFs, the withholding tax on these dividends is only 15%. We have computed the effective foregone dividend income for three risk profiles under the following assumptions: equity dividend yield 2% p.a. and REIT dividend yield 3.5% p.a. We find the following results (values in % of the total portfolio value):

Foregone dividend income for

We are planning in the future to replace some of our ETFs with pension fund share classes of index funds for which this withholding tax can be further reduced to 0%.

You have not calculated L1 withholding taxes for other geographies (Emerging Markets, Europe). According to my research, they are significant.

Note that LU ETFs do not report gross dividends and withholding taxes separately.

And why are you using FTSE Developed Asia Pacific ex Japan and MSCI Emerging Markets in the same portfolio? An amateurish mistake, I would say.

(1) This is not completely true. We are using index funds for many asset classes already. And through pooling and netting the effective stamp duties are lower than the nominal values of stamp duty.

(2) See our earlier answer: for low-risk profiles, the effect is 0.02% p.a. whereas for higher-risk profiles it goes up to 0.14% p.a.

(3) This is not a temporary offer – our plan is to stick with it and improve it even more the future by for example using even more (pension) index funds. In the history of True Wealth, we have never increased fees for any of our offerings, but instead reduced prices two times already (minimum fees and introduced degressive pricing). Extracts from our webpage:

This applies to the currency exposure of the fund (and not to the trading currency).

@True_Wealth where can we find the index/etf lists?

I was thinking of foreign withholding tax. If you use ETFs, you can’t reclaim 100% of the US withholding tax.

To our knowledge, the only relevant regions for which more tax efficient pension funds (as compared to ETFs we are offering) are used by Pillar 3a providers in Switzerland are the US and Japan. Therefore we think that comparing withholding taxes between 3a providers using ETFs or pension funds is only meaningful for the regions US and Japan. For any other regions, whether tax-efficient ETFs or pension funds are used, the tax treatment of dividends for investors domiciled in Switzerland is very similar or the same.

We have now made this list available on our homepage.