They reclaim Swiss withholding tax, which is not due on funds in the 3a custody account.

The foreign withholding tax can be only reclaimed by a fund (class) with a controlled investor group. These have “Pension fund” in the name. 4 of such funds available at TW are listed above. And none of them is interesting to me personally.

Getting a Swiss tax credit for foreign L1WHT is something completely different than getting a refund of L1WHT. I don’t see how the former could be possible for 3a as you don’t pay Swiss taxes on 3a. The latter is presumably already done to the extent possible/worthwhile by the mentioned ‘Pension Fund’ index funds but I don’t know whether that would be possible for any stock domiciles besides US and Japan.

I.e., I don’t know whether there is any tax disadvantage investing in EU using a regular ETF in 3a compared to investing via the CSIF World Pension Fund Plus (besides stamp duty).

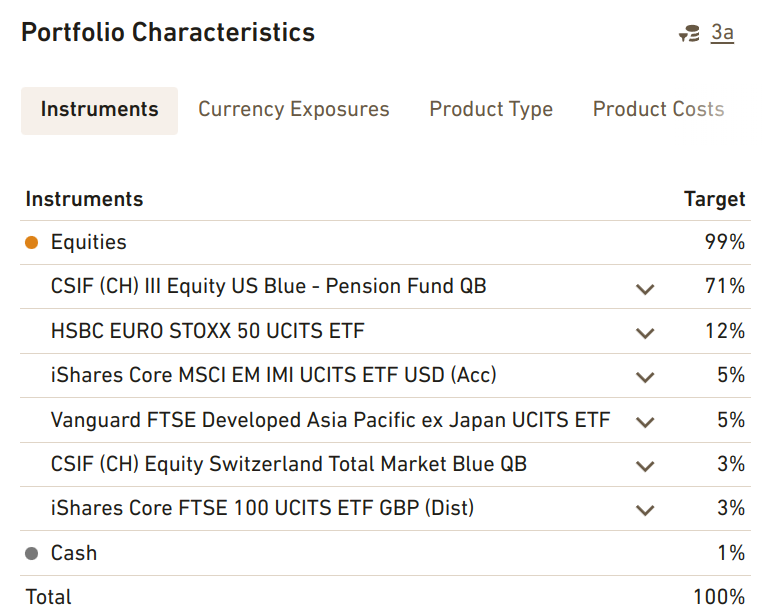

I actually think using an ETF for EU in this case makes more sense, since it is cheaper than an world index fund: CSIF (CH) III Equity World ex CH - Pension Fund QB CH0191014973 has a TER of 0.15% while HSBC EURO STOXX 50 UCITS ETF IE00B4K6B022 TER is only 0.05%. Since the ETF is with domicile IE, there should also be no lost WHT in my understanding. The downside is of course that you have to pay stamp duty, but on the other hand there is no subscription (0.08%) and redemption fee (0.03%). For me, it looks like True Wealth is using the more expensive pension funds for classes where you would loose WHT with an ETF, and for other areas cheaper ETFs when available. This makes sense to me, since it leads to a lower average TER than just using a world pension fund.

Same is for true for emerging markets: if they would use the CS index fund, you would have to pay a subscription (0.16%) and redemption fee (1.16%, which is insane) with a TER of 0.25% (CH0185709083). Instead they use iShares Core MSCI EM IMI UCITS ETF IE00BKM4GZ66 with a TER of 0.18% in my portfolio.

I would like to start a discussion about an optimal allocation using current available True Wealth 3a instruments. The following is my current allocation, with an overall / average TER of 0.13%. I am not using any currency hedged instruments, and increased the US exposure quite a bit (which is IMO very nice since they launched pension fund classes for it). What do you think about it? Any suggestions?

I tried to replicate more or less a MSCI world index (counties only), but now that you say it, you are right: I have slightly more weight on US (71% instead ~ 68%). Or are you referring to other weights?

Any other comments / suggestions regarding my allocation from above?

In the above screenshot there is an EM ETF, though, and it’s missing Japan (and other countries that are completely missing at True Wealth). So this is neither a MSCI World nor a MSCI ACWI approximation.

I still don’t understand why True Wealth is making it so painful to approximate a global market cap equity allocation. A robo advisor should be simpler, not more complex, than investing on your own.

Yes, sorry, I’m confused. This allocation is a bit a mess.

Anyways, MSCI ACWI and FTSE All-World have around 63-65% USA. So, 71% seems to be an overweight to me.

That’s what putting me off as well. They should either go pure market cap, or offer different profiles, like weights by market cap, GDP, their own intransparent method, whatever.

Just thinking out loud… Is it possible to go all in on Equity US Blue - Pension Fund on TrueWealth? It would be cheaper than Finpension, since third pillar assets are completely free. Or am I missing something here?

Sure but there is nothing “improper” about the QB share class. In the end what matters are the total fees. 0% + 0.15% TER is still less than 0.39% + 0% TER.

Just gave it a try - you can go up to 93% Equity US Blue - Pension Fund. Higher allocation seems to be not possible because diversification score goes below their requirement. Not sure though how this “requirement” is calculated… But anyway, the remaining 7% can be allocated to any other equities classes.

I have asked @True_Wealth exactly the same question, and they told me that the only difference is the TER: while finpension or VIAC charge a flat fee, you pay only the TER with Truewealth (and Truewealth does not pay CS directly instead). This makes it quite transparent for me, and in the end the thing which matters it the total fees. Paying 0.26% less fees (compared against VIAC and finpension) per year accumulates quite a bit over the years…

Received the following email from Truewealth today:

As you know, our Pillar 3a solution does not charge any asset management fees.

We are pleased to inform you that this will remain the case in 2025 and that no

management fees will be charged on your Pillar 3a assets.

We have also improved our Pillar 3a solution in other ways: we are now using

index funds that are exempt from withholding tax in our Pillar 3a investment

universe. These funds are exempt from the already reduced withholding tax of 15

percent on dividends from US equities. And the withholding tax on global real

estate equities is also being further reduced.

This is pretty good news in my opinion, looks like their “freemium” model works out and they are even investing in improving their product.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.