…or the ones with a DTA but no refund.

In any case, you could transfer your funds to a Schwyz-based foundation later.

Wouldn’t that require a different, separate investment strategy though - something you currently (purposely) aren’t offering? I mean, you can’t offer the same (tax-privileged) “pension” funds outside of the 3a offer?

I am planning to close a normal 3a cash account at a swiss bank and transfert the amount (quite a big sum at least for me) to True Wealth but for cash only and benefit from the 1%.

Has anyone made the moove yet ? Are there any pitfalls or tiny footnote one should know before going for True Wealth ?

They ask Frs 100.-- when closing the account in the first 12 month. When closing the account later to moove the stack to an other 3a provider, will it be free of charge ? Sumed up : is the 3a cash money safe by True Wealth ?

We plan to use more tax-priviledged “pension” funds in the future with our Pillar 3y offering. For our clients also managing their free assets with us, we will use ETFs for the corresponding asset allocation.

Put another way, our clients always have one portfolio with one strategy. The implementation, i.e. which instruments are being used to execute this strategy may differ between the assets invested in Pillar 3a and the free assets.

Exactly. It’s just an important point to be aware of when it comes time to withdraw.

Overall I’m pretty impressed with the True Wealth pillar 3a offer. I’ve opened an account and will try it out to compare performance with my other pillar 3a solutions.

Here is an extract from our FAQ Your money is safe with us and the deposit guarantee is guaranteed. Even better: With us, your assets are even covered by a state guarantee. The cash is held in an account at Basellandschaftliche Kantonalbank (BLKB) – and the canton of Basle-Country is legally liable for all liabilities of BLKB.

There is therefore no upper limit to the invested cash at the custodian bank backed by the canton.

This looks surprisingly interesting. Surprisingly, since I originally dismissed it as a temporary lure, but if fees stay low forever, I guess True Wealth now is the cheapest investment 3a on offer (or is there a cheaper one)?

What I am struggling with: What will be the overall fees at the end? What will I actually save compared to, say Frankly or Viac? Say for 99% stocks. TER for the ETFs is 0.15%. Then “minimal” portfolio optimization, transaction fees (how much is minimal, 0.01% or 0.10% or what?). And then 0.10% foreign currency transaction on the foreign stock part.

So:

0.15%

0.07% FX (1/3 Swiss, 2/3 global)

0.22% total so far

0.15% TER

0.00-0.03% FX*

0.11% withholding tax**

-0.01% cash interest***

0.25-0.28% total

*The FX conversion costs are not annual since they only occur when money is added or withdrawn, the strategy is adjusted or a rebalancing is needed to correct the asset class weights. The effective FX annual costs are therefore rather in the 0.00-0.03% range (assuming you deposit new funds every year). Remark: our portfolio is currency-hedged and we aim at using CHF as trading currency as broadly as possible.

**With 99% stocks, the withholding tax on dividends is effectively about 0.11%. Remark1: this holds for about 40% allocated to US and JPN equities. Increasing/decreasing the weight of these regions increases/decreases the withholding tax. Remark2: the value we quoted above (0.14%) is higher because we use equities and REITs in the portfolio we recommend for high-risk tolerance. Without REITs, this effective withholding tax on dividends is reduced.

***We treat interest on cash as a negative cost (in this case 1% of portfolio x 1% interest).

Here’s an excellent review of the Truewealth 3a Pillar. Once again, great job, @anon95353169 ! Love your blogs, especially the ones on FIRE portfolios and safe withdrawal rates!

For me, Truewealth 3a is a big fat NO as long as they have this nonsensical CHF-limit.

“One major limitation is that you must have 35% Swiss francs in your 3a . Indeed, they are limiting foreign currency exposure to 65%. So, you must either invest heavily in Swiss shares or use currency hedging. This limitation is quite important and will hit your returns in the long term”

But I very much welcome you bringing some pricing competition to the scene, @True_Wealth !

Agreed. I love the customizability finpension 3a offers in this regard. That’s why I will stick with them as my preferred 3a choice, but the True Wealth 3a offering is IMO among the top 3 3a solutions available, and, depending on your individual preferences, is capable of being the best choice overall.

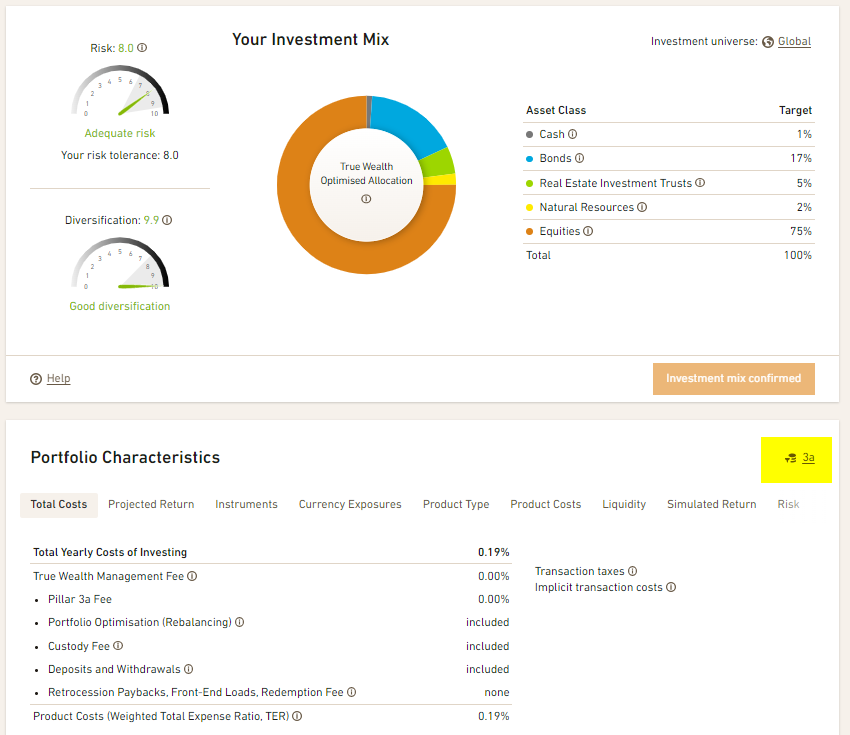

Here are the costs for 3a. Make sure you select “3a” in the portfolio characteristics (see screenshot below).

If you want to adjust e.g. your weighting of equities, click on the orange part of the portfolio. From there you move the slider appearing below the portfolio as you see fit. You can see in real time how this impacts the total cost.

Here is an extract from our FAQ about currency hedging:

Do currency-hedged investment instruments incur additional costs?

The costs of currency hedging are usually low. They arise from the fact that futures contracts (FX swaps) have to be rolled, i.e. exchanged, approximately every three months. The resulting bid/ask spreads of the forward contracts are in the range of a few basis points (hundredths of a percentage point) for the most important currencies (incl. CHF, USD, EUR, GBP, JPY). At most, for commercial reasons, the product costs (TER) are slightly higher for currency-hedged ETFs and index funds, which is why we always pay close attention to the TER when selecting investment instruments.

Sometimes, therefore, it is wrongly argued that the interest rate difference is the cost of currency hedging. This is a fallacy, because historically, currencies with higher interest rates have often depreciated against currencies with lower interest rates. If we look at the period 1989 to 2021, for example, interest rates on US dollars were higher on average than interest rates on Swiss francs, but the exchange rate loss completely compensated for the interest rate advantage.

I don’t think I have much use for your product, but there is one thing I would like to comment. It looks like you don’t offer global stocks ETFs/funds. Why? If your goal is to make investment easy and understandable, then what could be easier than one fund portfolio? VWRL? MSCI world?

The truth is, you either can’t or don’t want to offer non-currency hedged ETFs. Finpension offers me the choice. I don’t need investment advice - der Kunde ist König.

And here’s what I have to say about currency-hedging:

Personally I’d say can’t, this was discussed a while back when finpension launched. It’s still not clear to me how they justify it (maybe the FINRA punishment are small enough to take the risk). I understand that most other providers would have more conservative legal counsels.

Tbf depending on your opinion on various things it can also reflect poorly on finpension to take freedoms in interpreting the law (are they then more likely to do it for other part of their business?).

I agree. TrueWealth doesn’t seem to use any currency hedging outside 3a, not even for low-risk bonds (where it’s commonly recommended). I can’t think of another reason than regulation to deviate from this in 3a.

However, they could make it a lot more flexible. E.g. I can’t define an investment mix of 60% global unhedged equities and 40% CHF positions (could be a mix of equities, real estate, bonds and cash). I.e. hedging is enforced beyond what regulation requires.

VIAC requires 40% CHF positions, however, you can choose hedged and unhedged funds yourself, as long as you satisfy the 40% CHF requirement. That’s much more reasonable, in my opinion (although, VIAC oddly doesn’t offer hedged bond funds).

I find this strange too since the common scientific consensus is that globally diversified bonds should always be hedged and equity only for security in the short term but never in the long term.

Here is the way they justify it: The X% maximum foreign exposure limit is considered on the total assets of the foundation, not at the individual level. So, as long as the exposure is below we are good. This means that in order to have to people with higher exposure, there needs to be people with lower exposure. Since they also offer some Swiss portfolio and since many people are heavily biases towards Switzerland, this likely plays in their favor and helps them reach a lower foreign exposure while still allowing aggressive individuals to do what they want.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.