I bet most of you don’t have one, but I am thinking I should finally give in and buy travel insurance.

One thing that I want is the car rental excess refund. Once I used to have a single insurance just for that, but now I might be willing to cough up a bit more to get all other things like lost luggage, flight cancellation, etc…

Is it at all worth it (we travel by plane/train a few times a year)?

Any offer that you can recommend for or against?

What about credit cards that come with one? Maybe it’s cheaper that way, but perhaps the coverage is more limited?

I do not have an answer unfortunately (I do not have a travel insurance either, but exactly this weekend I told my wife that we might look into this as we plan on doing an extended trip outside Europe soon)

I am specifically looking into coverage for:

Car rental has always been a nightmare in my case (we do only use Mobility here in Switzerland). Rental companies always try to up-sell insurances.

I plan on bringing some expensive photo/video equipment. So I need coverage for theft.

Then if I am not mistaken and I want some COVID-19 coverage (repatriation, etc…) I heard that travel insurance is the way to go!?

For travel insurance, check the Ikea Credit card post. It’s better than the Cumulus one (which is similar to a health insurance insurance).

For the Excess coverage of rented car, there is a british company that covers that and it’s cheap. I don’t remember it unfortunately. I google with 0 deduction or something like that.

This is the whole insurance, I’ve seen one that covers only the deductible, which in some case is nicer since you can use the insurance offered with the car and use this only for the deductible.

I have that piece (and most others like luggage, electronics, sports stuff - both damage and theft) as part of my household insurance.

And travel-wise, I only have travel cancellation insurance separate.

I’d take a look at the Liberty Plus credit card. It has an annual fee, but rewards for travel (including gas, SBB, etc.) are high. You can redeem these for useful vouchers (SBB, gas, SWISS, etc.) at good rates. I calculated around 2% cash back value for travel purchases and redemptions.

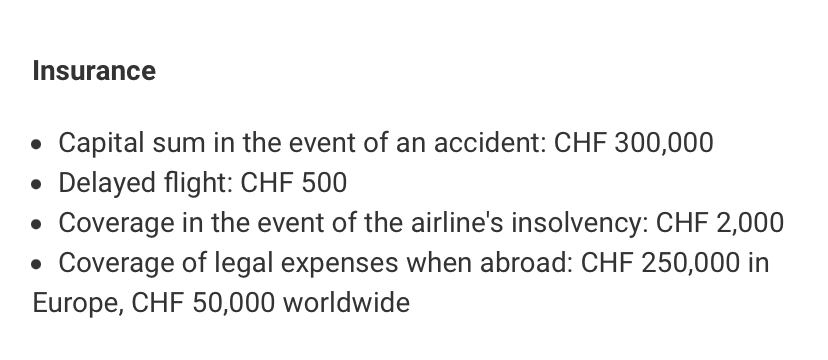

You get a rental car collision damage waver, plus trip cancellation/interruption, coverage for extra expenses during trip delays, travel medical insurance, travel legal insurance, luggage insurance, search and rescue insurance. You also get a few other perks like Avis discounts, bicycle insurance, a concierge service, etc.

I used it for a long time. When I was going to cancel after the first year with the introductory 50% annual fee, they offered to let me keep the 50% fee if I kept the card. So in the end I was paying 75 francs but saving around 100 francs in travel insurance per trip (I have a big family), and 30-50 francs on CDW per car rental. The rewards covered the annual fee. Also, you are covered by the insurance even if you do not use the card to pay.

You can compare Swiss annual travel insurance offers here, but from my research you only get much more coverage than what you get with the above-mentioned credit card with the top-end policies: Travel Insurance Comparison Switzerland - moneyland.ch

The going CHF/EUR exchange rate is accounted for in the moneyland.ch credit card comparison. The foreign transaction fee is lower than average (1.75% instead of the common 2.5%), though I wouldn’t recommend using a Swiss credit card for foreign purchases (better to use TW/Revolut, etc.). Rewards are exceptional for travel (gas, public transportation), but otherwise average. It’s really the insurance which makes this card worth looking at.

There are cheaper travel insurance policies, but AFAIK none which include a collision damage waiver. That’s generally only included in the CHF 200+ travel insurance offers.

I’ve got this on my list to investigate more (I don’t have a lot of experience) but just based on COVID experience: do not get the TCS ETI Livret. This was really strongly recommended to me but in the end I found out it was more based on a lot of people having it, rather than actually having had to use it. TCS drew out the process literally 18months and tried to make it as painful as possible so that I would give in. After trying every trick in the book to try and get me to lose interest/out wait me, they finally paid me what was in the policy to pay. Terrible experience.

In the end my credit card company was the reason they paid at all and were extremely professional. I forget the term, but the credit card company and TCS were on the same level of responsibility and so had to split my claim 50:50. The credit card company actually paid right away and then put pressure on TCS since they would have to cover if TCS didn’t pay.

Interesting options, thank you all. My travel insurance with Zurich will run for 12 months, but next year I’ll look at the alternatives again.

It’s a bit painful, because I find that you actually have to check the fine print. Especially the cheaper ones exclude a bunch of things, so their coverage might look comprehensive, but actually isn’t. They might exclude certain illnesses directly or indirectly (e.g. excluding coverage if an illness could have been diagnosed when booking) or excluding coverage in case of airline bankruptcy etc.

On that basis I excluded the insurance you can get with a UBS Gold card, which includes CDW out of the box, even though I don’t remember what exactly was wrong there. The Liberty card does look interesting, however. I’ll check the fine print there.

Thank you everyone for sharing your thoughts. I am also thinking along similar lines. Didn’t come to any conclusion yet, but would like to share some thoughts for discussion.

Cornèrcard Visa Platinum

500 CHF per year

Cashback 1.5%

Assuming a cashback 0.75% better than free AMEX + other credit cards, turnover 30000 per year, we get actual cost around 275 CHF per year. And this comes with lots of insurances for the whole family, which conditions I didn’t read in details yet.

A disadvantage for me is that additional cards are for free, but it is Gold, so 1% cashback. 2 Gold cards are 240 CHF per year, 1% cashback. Insurances are also for a family, but limits are lower. Silver cards are coming with individual insurances only.

I had for many years the cornercard card and you can buy the travel insurance for CHF 30/single or 49/year family, that has included CDW excess refund. Useful for some countries like Australia/NZ were you have 3000+ in cdw excess.

Pricing has changed but you can get some frequently running promotions, and at year end if you spend enough and nudge them, they will keep you the lower price.

Service wise corner was excellent, but I cannot talk about the insurance since I’ve never had an accident.

So, at the first selection round I disregard all travel insurances linked to credit cards, as they always require that a trip should be paid by that credit card for an insurance to be responsible. Which is kind of expected, but it is not what I want. I want to be flexible in payment methods, and if there is a 20 CHF discount for using a specific payment processor (a real example), being able to use it.

Then I narrowed on Axa and Zürich travel insurances. After comparing their conditions, I chose Zürich Relax Assistance, which is cheaper and seems to have a bit better conditions.

I am looking to book a larger flight soon, for which I would like to be covered in case we need to cancel (due to illness/pregnancy).

Seems that my current insurance with Axa only covers my illness or death in family, and it is only personal - i.e. doesn’t account for illness/pregnancy of my fiance for example.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.