in March 2015 I subscribed to a 3rd pillar (CHF 6768.- per year) coupled with a life insurance at PAX. This is probably what I consider the biggest mistake of my life so far

Below are the main conditions about this contract:

→ Minimal technical rate of the savings: 1.25%

→ Minimal payment per year: CHF 1200.-

→ Waiver of premium in case of earning incapacity: ~400 per year

→ Currently I’d lose almost CHF 13’000 if I drop out of this contract.

I wrote to PAX at the beginning of November 2020 asking them:

→ To reduce the payment from 2021 to the minimum (CHF 1200.-)

→ To supress the waiver of premium in case of earning incapacity (~ 400 per year)

→ A view of the evolution of my capital with regard to the two above mentioned changes and until the end of my contract (01.04.2054).

→ Information concerning the evolution of my capital from the entry into force of the contract until today.

They replied to my at the beginning of December 2020 telling me they received my letter and needed some time to come back to me. So far they haven’t came back yet.

Nonetheless, I made my calculation according to the financial plan I received from them in 2015.

→ Option 1, I keep the payment at 6768.- per year and supress the premium in case of earning incapacity. The remaining amount that I can put in my 3rd pillar and deduct from my taxes will go to VIAC.

→ Option 2, I delete the contract completely and invest the full amount to VIAC.

→ Option 3, I reduce my payment to the minimum of 1200 per year and invest the rest to VIAC.

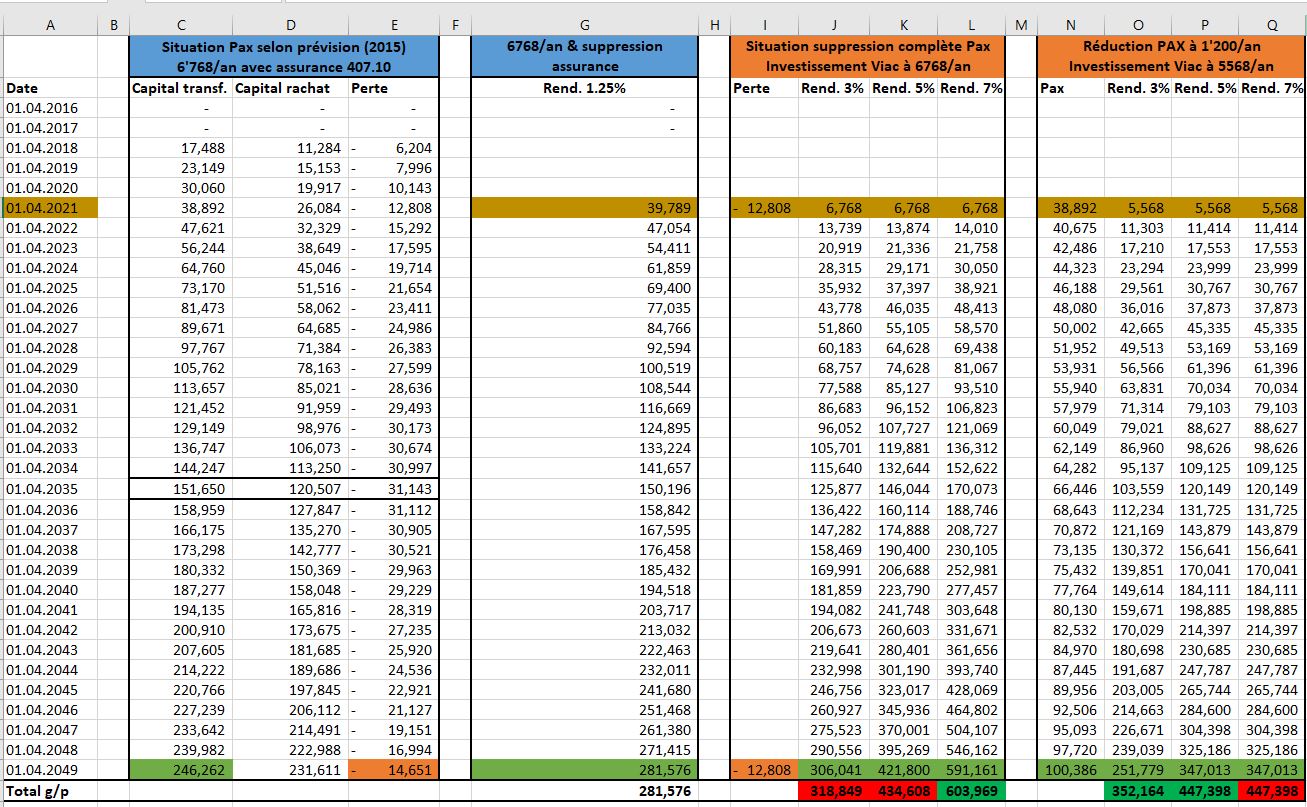

According to my calculation, it’s financially worth choosing Option 2 if my VIAC investment generates an average of 7% interest annually. At a 5% interest annually, it is financially better to choose Option 3. I attached a picture of my calculation as Excel attachment aren’t allowed.

For this reason, I tend to choose Option 2 as a way to diversify a part of my 3rd pillar with a secure 1.25% interest rate, which is also financially more profitable in case my VIAC investments do not provide a 7% interest rate annually. I consider this as rather probable knowing that I foresee to gradually reduce my exposure to my VIAC 3rd pillar invested in share the closer I’ll get to the “official retirement age in Switzerland”. In addition to that, Option 2 give me the possibility to use the capital invested with Pax for a mortgage if I decide to buy an apartment (which isn’t in my plan now but one never knows). In that case should, does somebody know if I should take into account the value of my capital at PAX (currently: ~38’000) or the surrender value of my capital at PAX (currently: ~26’000) ?

I’d be very interested in having some critical thoughts and advice about my situation before coming back to PAX.

Thank you very much in advance and I wish you all my best wishes for the year 2021!

I did it. And it made me realise the mistake I did. Then when I did the math with my own situation I realised that in my case the best option might not be to completely opt out, but rather to reduce my yearly payment to the minimum. But there is maybe something that I’m not seeing correctly, which is why I wanted to write here about my situation and seek some advice.

Wouldn’t half the money with this option still be gone towards insuring your poor life rather than building savings?

Even if all goes to savings, if you’d rather invest the money in stock market, their 1.5% promised return vs expected stock market return will amount to enormous difference over a 2-3 decades. The stock market historically would have doubled your money every decade, give or take. And with their 1.5% interest (subject to T&Cs bla bla bla and continued company existance etc i’m sure) it’d take, oh, about a lifetime for a single doubling

No, the money would not be gone towards insurance. The minimum payment per year at Pax (1’200) would increase my current capital at Pax and would benefit from a minimum interest rate of 1.5%. I do agree that 1.5% is ridiculous if you compare it with the estimated historical average interest rate of 6-8%/year.

I take into account (1) the uncertainty about the interest rate when I’ll want to withdraw my 3rd pillar (if I maintain 100% in share and there is a crash before, I’ll loose some money; if I slowly reduce my exposure to the stock market before my “official” pension, I’ll loose money) and (2) the fact that I need a yearly interest rate of more than 5% over 30 years with VIAC to be financially profitable to completely cancel my Pax contract. Don’t get me wrong, I would be okay losing 13’000.- to change the course of my current situation for a better outcome in 30 years. However, the above mentioned points made me cautious, as the outcome would be positive only with a yearly interest rate above 5% during 30 years.

Without knowing your contract in detail: While you may have paid in close to 40’000 into the product, I doubt that you currently “have” ~38’000 CHF capital** at PAX.

I assume the 26’000 CHF in surrender value are what you “have” with them and what can be used for home ownership (a quick googling seems to support that, but do your own research).

You have a choice would you like to continue playing this farce where you pretend you didn’t lose anything for a few more years before the reality hits you, or let it hit you right now and move on

I can tell you about myself: I went to see a tax specialist when I arrived in Switzerland and sold this as a great way to optimize my taxes. I computed the equivalent annual interest rate which was 0.7% and figured that it was better than what banks were offering for 3a savings accounts. I didn’t know one could invest in funds as the time.

That’s true. But looking at the math over 30 years, isn’t the fact that I need more than 5% interest rate per year an argument to take into account in my decision ?

I consider those contract as scam and regret having fallen for it. But now I try to keep a financial and rational perspective to make my decision.

No offense taken. I was in the same situation as the one described by @Ed_Waadt and fall for it because I was financially uneducated for the reason mentioned by @kilyn.

By the way, I was serious about you being a lucky guy. Other people have surely made way worse mistakes up to that point in life - financially or otherwise (imagine killing someone by drunk driving or so).

So you’re considering throwing another 34’000 or so CHF into the scam (28 years x 1’200 CHF)?

By the way, maybe I’m not privy to the terms of your insurance or there’s something I am not quite getting in your spreadsheet calculation/projection, but there’s two questions I have:

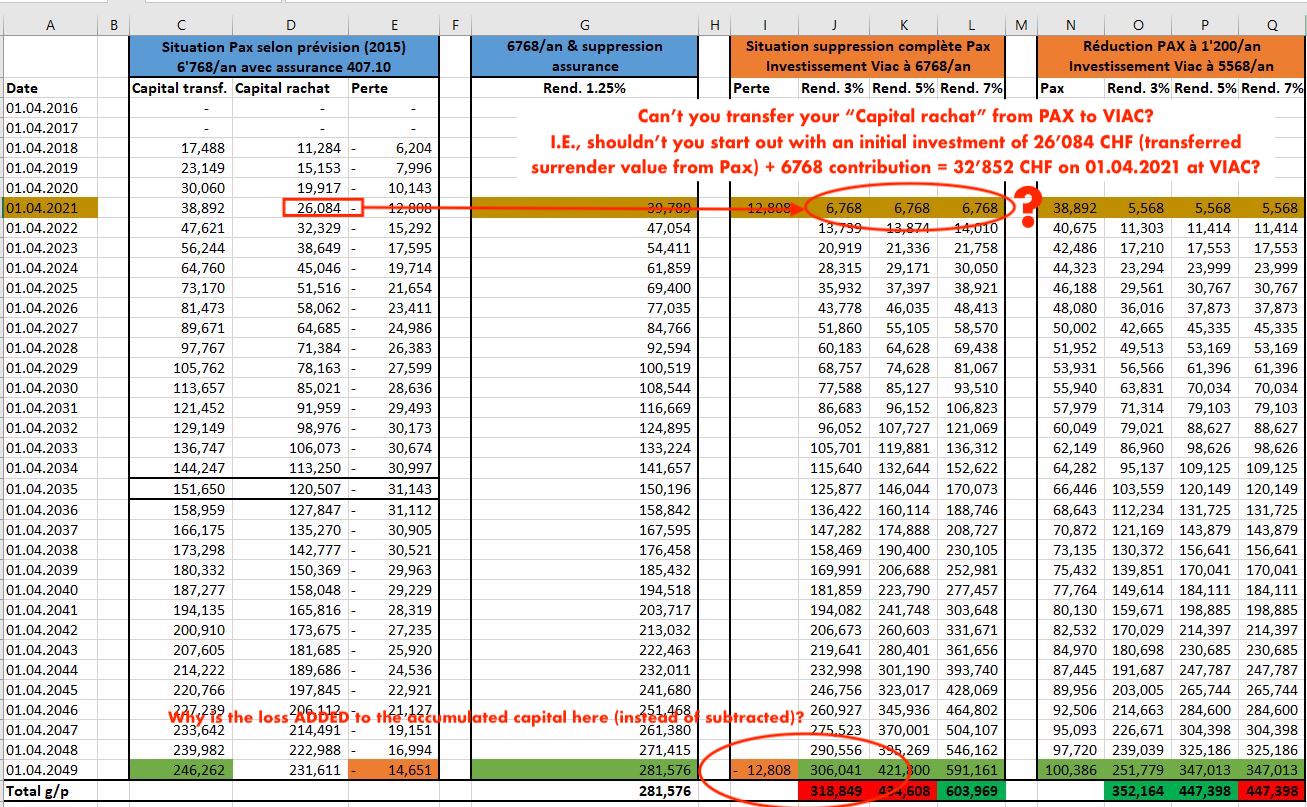

(Where) did you account for a transfer of your capital at PAX (surrender value) to VIAC? I mean, at least the surrender value of your current life insurance should be transferable to another 3a provider, shouldn’t it?

Why is the current loss of 12’808 added to the April 2049 capital projection in the second scenario, instead of substracted?

Permanent Life Insurance, like savings accounts, are hangovers from the days when direct investment was too complicated or inaccessible for most people. They were ok for the time as they gave people who otherwise had no means of earning any returns an avenue to do so. Today they’ve largely outlived their usefulness, except maybe for some people who have no interest in personal finance or investing whatsoever and just want a basic savings solution which they plan to stick to for most of their life (in which case there is generally some small return, or at least no loss).

If you want to diversify your portfolio to include insurance, then option 3 may be a consideration. An argument for this is that insurance companies have weathered past crises much better than banks, so insurance could provide a supplement/replacement to pillar 3a bank account balances for the purpose of minimizing risk.

If diversification is not a major concern or if your don’t hold significant pillar 3a bank account balances in your portfolio (nor plan to), then there is really no good argument for keeping your permanent life insurance, in my opinion. Barring a decades-long recession, the opportunity cost compared to option 2 is huge. That is especially true if you remove the premium protection rider, as that would be the only possible argument for using permanent life insurance, in my opinion (because the premium protection insurance premium is generally much lower than the premium for the same amount of disability insurance).

I agree. Generally speaking there is often “worse” and it helps to remember it. However, I tend to set the bar quite high, so I somehow want to hit my head very hard against the wall for that stupid bad choice from 2015. Nevertheless, it won’t have any impact (I mean a positive impact on my bad choice, because it will have a significant negative one on my head). What is done is done, and life moves on

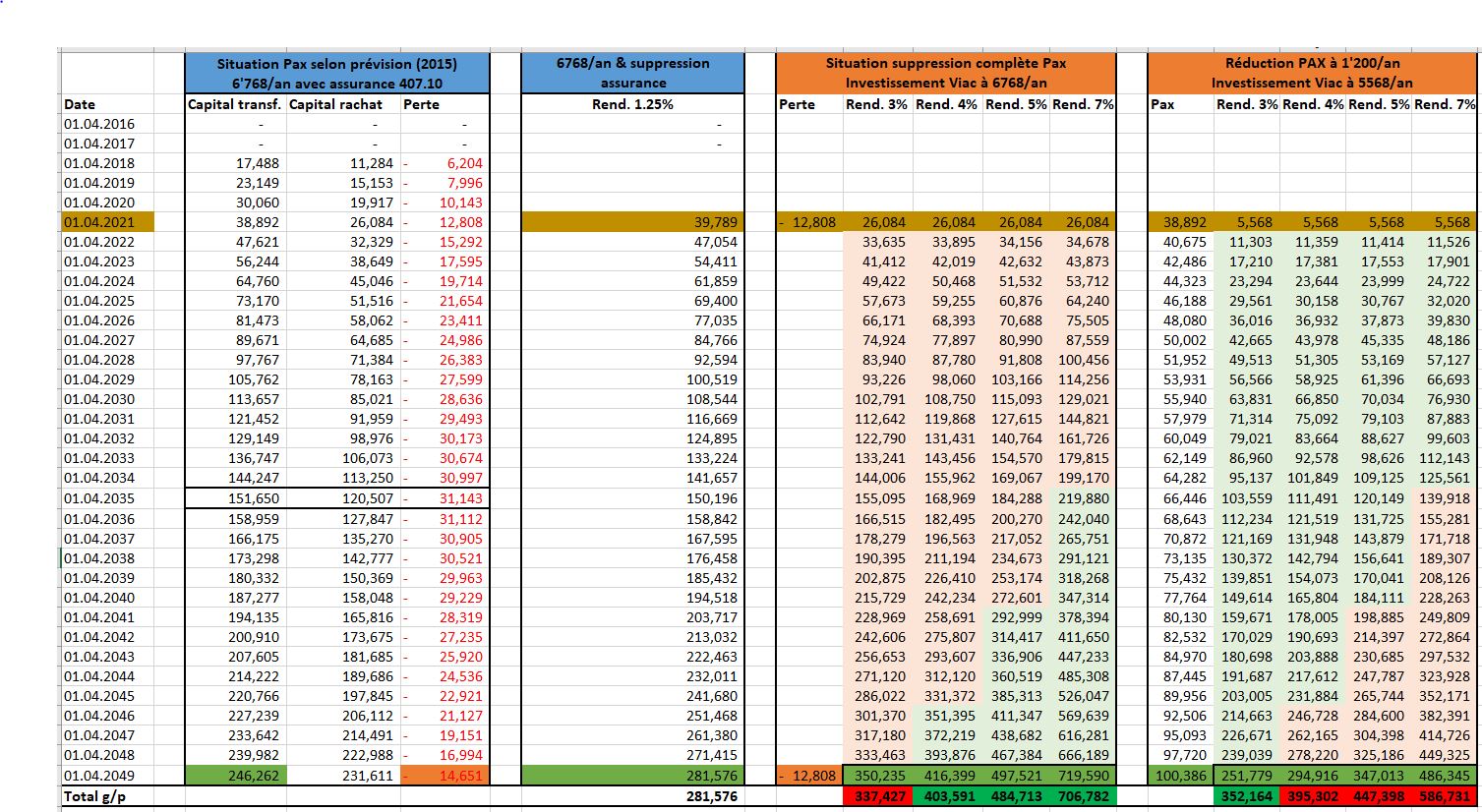

THANK YOU for noticing those two mistakes. I’m by far not “a number guy” and I feared to have made a mistake somewhere, which was indeed the case. The first one was very important as it impacted all the following calculations. The second one was due to me not noticing that “- -12,808” becomes “+ 12,808”.

Now it is much clearer. It is financially more profitable to completely cancel my current policy if the yearly average interest rate with VIAC is above 3%. Knowing that usually historically there was an average interest rate of 7-8% on the stock market, it makes more sense to cancel my policy and to move all my investments in VIAC. This also considering the current 0.52% yearly fee on VIAC.

If I’m not mistaken, you should remove the -12’808 in your revised version as well.

The transfer of (only) 26’084 CHF to Viac does imply or already “contains” that loss. It’s as if you’re subtracting it twice.

Also, the “Situation complète Pax” columns do not include your 2024 contribution (CHF 6’768) but only the transfered amount (CHF 26’084) from Pax on 01.04.2021, whereas the “Réduction Pax” ones do (CHF 5’568 contributed in 2021).

Blockquote 1. If I’m not mistaken, you should remove the -12’808 in your revised version as well.

The transfer of (only) 26’084 CHF to Viac does imply or already “contains” that loss. It’s as if you’re subtracting it twice.

Blockquote 2. Also, the “Situation complète Pax” columns do not include your 2024 contribution (CHF 6’768) but only the transfered amount (CHF 26’084) from Pax on 01.04.2021, whereas the “Réduction Pax” ones do (CHF 5’568 contributed in 2021).

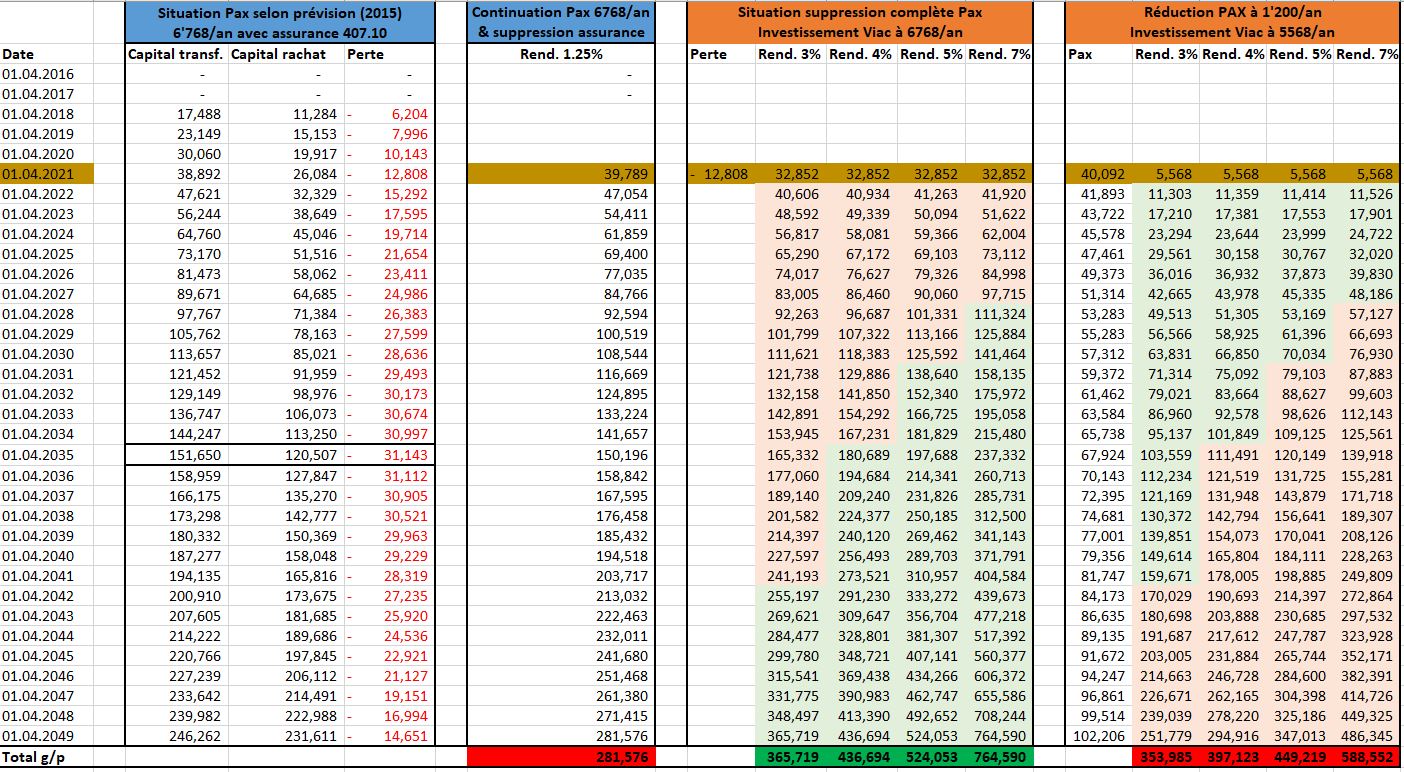

True, again. Both my columns (“Situation complète Pax” and “Réduction Pax”) do not include my 2021 contribution to PAX, respectively CHF 6’768 and CHF 1’200. In “Réduction Pax” my contribution of CHF 5’568 to VIAC is correctly included, as you mentioned it.

The clear financial advantage of going out from Pax ASAP is even more striking. In the light of those corrected numbers, which hopefully do not contain any flaws anymore, I understand better the clear opinion expressed in this topic. Thank you all.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.