We’re not talking about lung cancer …

1 Like

Correct. Would you mind sharing why would you keep relying on US providers?

Frankly speaking, I completely fail to see any reason to buy US funds at a US broker, now that cost-effective and tax-efficient European alternatives are widely available. It adds completely avoidable risks, without bringing any significant upside.

I am genuinely curious to hear why would you keep relying on US providers.

Personally while I started diversifying (a tiny bit), it’s still a lot more convenient (low cost, high liquidity, good coverage with single fund approach, and due to personal situation I don’t worry too much about estate filings).

If there’s a big risk, it should impact all US investments, whether they’re in a UCITS wrapper, or non US broker, or not.

(and if US makes drastic moves esp. something like section 899 as unlikely as it is, it’s going to impact everyone, US treasuries are still underpinning most of the global financial system)

4 Likes

dividend tax wise, VT still seems to have the advantage to me? Otherwise you’re still dealing with swaps (with corresponding fees) and likely having to split into multiple funds (i.e. more effort and temptation to change) to have a USA swap fund. You have the scalable capital mixed global fund, but it’s low TER is (for now) temporary.

(And if you split the ex-US stuff is still somewhat expensive TER wise, even if the L1 tax is same-ish and doesn’t include emerging markets, requiring 3 funds total)

3 Likes

Fees and taxes on dividends (DA-1). My own risk analysis assesses that the savings in fees and dividend taxes far outweigh the risk of choosing IB and US-based ETFs, stocks and options.

Can you share how much you think you save in fees and taxes compared to using a European broker like Degiro and European funds like XALL or ALLC in the long run?

I will re-do that analysis again following the above discussion as I share some of the concerns regarding ‘all eggs in IB’.

Last time I did it the biggest hit was the FX fees, which with IB are so competitive compared to e.g. 0.25% at degiro.

1 Like

XALL and ALLC (or the physical WEBG) are traded in Swiss francs in Zürich, therefore there are no FX fees.

Spoiler alert: there are no savings. Just more risks, without more rewards.

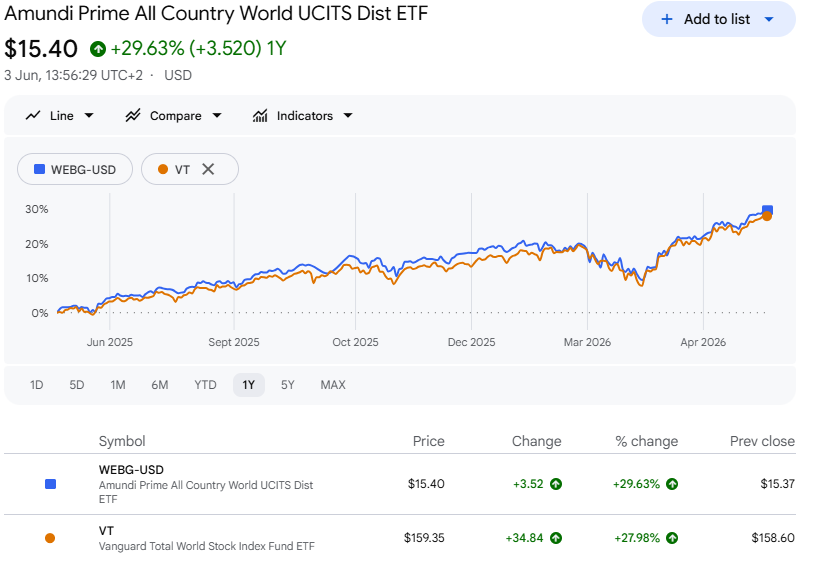

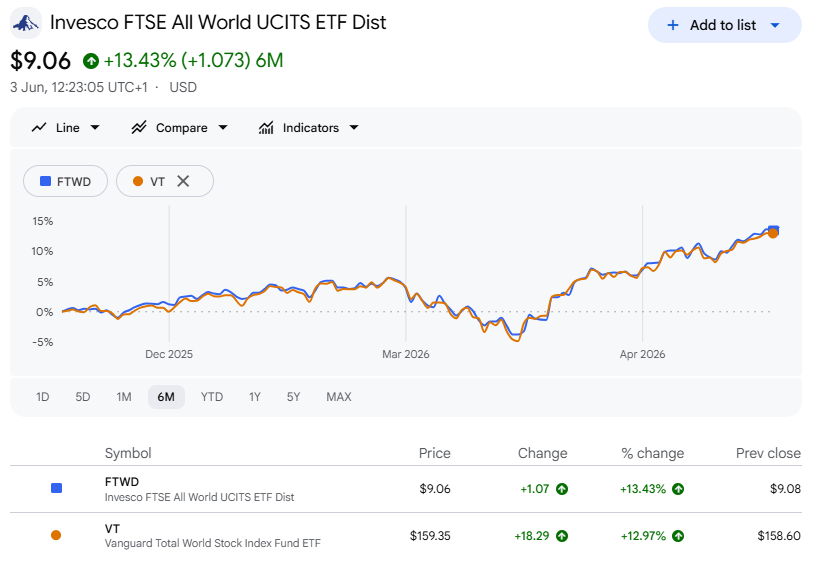

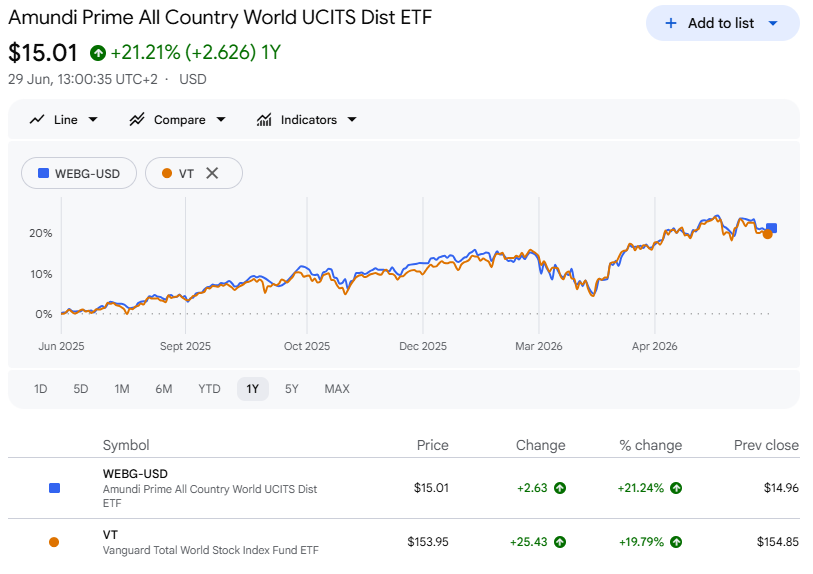

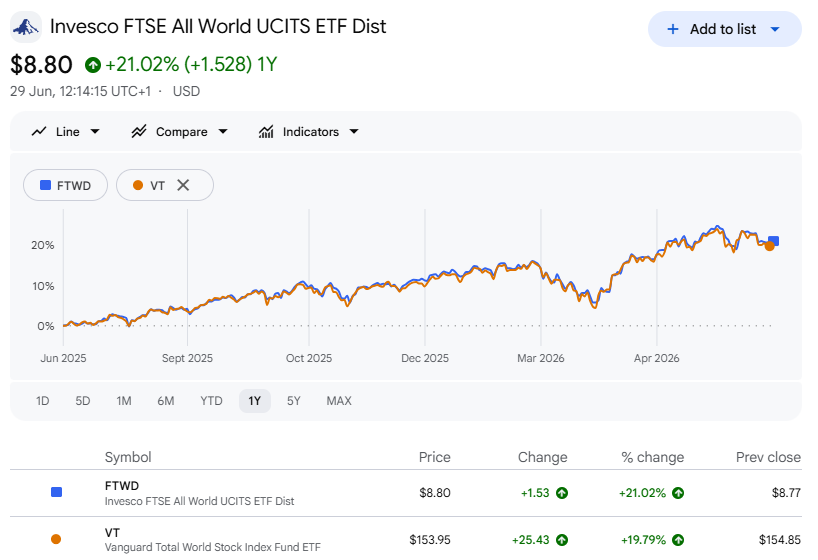

These funds come in different flavours but bring comparable performance.

WHT drag and higher TER are some of them at least.

I did not quantify, but am observing the outcome of this discussion to see if I make any significant changes myself.

For ex-US I already started slowly boosting with EXU1 (the rest is in 3a), but for US still with VTI.

1 Like

I did quantify. TER is as low as VT and synthetic funds have no WHT drag.

We had the discussion around messages 40-45 regarding different flavours and different indexes.

We didn’t end up with a good reason to accept additional, avoidable US risk concentration.

What was clear is that VT brings performance that is comparable (at best) to UCITS funds.

I would not have phrased it like this, but what the actually extremely interesting and valuable discussion points me towards … if you are somewhat concerned about US concentration including broker and ETF jurisdiction, there is no ‘perfect fit’ and everyone needs to find the right compromise for oneself.

It will always be a compromise between fees, risk and returns:

- IB + VT .. is clearly simple cheap and give good returns but you have the US inheritance tax and US risk to manage

- Saxo + CHF-traded ETF … Swiss-based, no FX fees, but likely lower spread and stamp duties

- degiro + ETF … comparably low trading fees and no stamp duties, but balancing between FX fee and low spreads (EUR and e.g. Xetra) or no FX fee and higher spreads (CHF and SIX)

5 Likes

Here are some number for 2025:

- no Swiss stamp duty

- 25 trades of VT = USD 20

- spread for buying/selling VT = supposedly equal or better than European broker

- 22 FX transactions (USD > CHF and CHF > USD) = USD 24

- Access to US treasury bills for short term USD investment (3-6 months) → don’t know if this is possible with European brokers.

- return of 15% withholding tax with DA-1: CHF 330

- no account or portfolio fee

IB tells me that cumulative effect of costs and charges reduced my total performance by -0.46%.

Another aspect for me was the clear and understandable write ups of the Poor Swiss and MP about how to invest. If it hadn’t been for these articles I would not have started my own investments.

If there was a similarly clear and understandable write up of an alternative investment strategy I would be more than happy to have a look at it.

1 Like

Thanks. Getting 330 francs via DA-1 means an implied dividend of 2.2k and a portfolio size of roughly 115 to 120k.

Let’s take Degiro and a CHF-Listed All-World UCITS fund:

- Stamp duty: zero

- FX fees: zero for CHF-listed funds

- Trades: zero if your ETF is on the main list, 2€ each if it’s another ETF.

- Spread: large UCITS funds trade at a negligible spread. The one-off spread you paid for your 1’000 shares of VT is probably around 1’000 cents. That’s 10 francs for your entire portfolio.

- Not being able to buy BOXX : saves you from a negative yield in CHF.

- Withholding tax: zero with swap-based funds.

- Account or portfolio fee: zero

- Excess return from picking a better fund: depends on you, but there are options as you can see below.

The Poor Swiss and Marc Pittet certainly are nice and helpful guys, probably just like you and me. They never pretended to be finance experts, and neither do we.

What I do recommend though, is to run some calculations for your personal case because the assumption “savings in fees and dividend taxes far outweigh the risk” was maybe correct in the past, but maybe not anymore.

From my calculations, the price difference is:

- absolutely tiny for a 120k portfolio

- not necessarily in favour of VT, and in fact quite the opposite.

It is indeed up to you to assess if it’s worth the risk. As many said, it is a very personal matter and this conversation is certainly helping many of us to better understand what is changing and what is not ![]()

4 Likes

There is too much handwaveium in the list for my taste. Pick a concrete example and go with it. May I just say:

- You seem to combine the trading fees of Degiro with the no fixed costs of Saxo.

- Spreads for CHF denominated funds are probably around 0.2%

- FX for dividends dipends on the fund currency (not trading currency)

- Vanguard passes on revenue from Wertpapierleihe after cost, while other providers keep half if it.

- Swappers may not have WHT, but the cost of the swaps is not part of ter

- Most indices track the worst possible wht reimbursement, while Vanguard US may not do this (not sure)

- You have to calculate the cost (and lost revenue) over 20 or so years, assuming reinvestment

No.

No. Large UBS or iShares funds at SIX have a total spread of 3-4 bps on a typical rebalancing day.

Not at all. Forward on the fund itself is close to nothing. The 0.25% mentioned earlier is absolutely dependent on the trading currency.

I beg your pardon? Can we just check the performance delta on a full year rather than marketing claims?

Short answer: No, it really depends.

Correct, so what matters is the tracking error and at the end, the performance delta on a full year for comparable indexes.

I beg your pardon? Can you back this up?

I did. Others did it in this conversation as well.

1 Like

Just to clarify: A CHF investor holding BOXX unhedged would keep the 4% USD return but take on FX risk. The 4% hedging cost would roughly cancel out the 4% yield, leaving negative net return in CHF terms, after trading costs and 0.19% TER.

I am really happy you guys have the nerves to discuss miniscule differences in ETF choice, domicile choice, etc.

In practice, my performance using VWRD at LSE looks the same as it does with VT - despite the low volume of VWRD (market makers will immediatly fill orders - so the spread you see is not the “real” spread).

(Switched to VWRD, because I wasn’t able to get value out of the DA-1 anymore after buying property). When the Vanguard all cap is here, I’ll buy it instead - but performance wise? probably not even 1-2% over 30y.

5 Likes

I’m not talking about BOXX, but about United States Treasury Bills. I had USD, no fx risk.

While tracking error is meaningless, tracking difference between US and European funds is not easy to compare.

Again, we should really compare a specific ucits package at a specific broker against vt @ ibkr. Chose your champion!

Also, please state and reason your risk assumption (a percentage number) for vt with regard to a comparable ucits package.