I think the 1042-S could be particularly helpful in this case, it clearly states that you are the recipient of the withholding tax (and not the etf provider).

I would also write to the federal tax administration to have their written confirmation that you can claim back the 15% wht for VT and support your claim, there’s a contact form on their website.

Hey there, I recently had the opposite experience than @FunnyDjo. My DA-1 was initially refused (in VD), so I called and they promised to look into it.

It turns out that the “stocks taxation specialist” who processed my demand refused it by mistake. It took them 3-4 days to clarify and they called me back to tell me it is being fixed. Maybe it helped that the person who checked wasn’t the same one that made the mistake (initially they wanted to address me to “my guy” but he wasn’t available).

Anyways, I would encourage you to push back. Not only you will hopefully get your CHF 116.- back but it’s important that our tax people do things right, they are dealing with our money after all! And who knows, it may help others down the line

A small update on WTH refund, I did exactly the same type of declaration for my VT shares and their dividends for 2022. nb: I declare them individually in the software for each purchase to calculate the withholding tax amount automatically.

For 2022, it was 325.- and was approved and applied.

For 2021, it was 150.- and was denied. I wire then and send the explanation of the federal tax office but never had an answer.

I had no explanation of what change outside of the tax officer but it’s reassuring for the future.

Apologies for digging out this old threat, topic is still relevant.

Anyone got the non-reclaimable WHT credited from the regular tax bill in the case where the DA-1 reclaim got denied or substanially reduced? How did you do it?

Or even better, successfully challenged the reduction due to mortgage interest? The tax office argues with a federal court ruling (2A.559/2006), which seems to conclude that interest paid doesn’t need to be related to the dividend income.

Yes, it’s about the calculation of maximum DA-1 reclaim. If mortgage interest (and deducted wealth management fees) are high enough compared to the dividends you reclaim WHT on, it gets significantly reduced, leading up to 0 reclaim and hence double taxation.

I read the regulation quoted above as that you could get at least the WHT credited via the regular tax declaration, at least if you don’t file the DA-1 reclaim in the first place.

The question is if the maximum DA-1 reclaim is smaller than the reduction in income tax you get if you deduct the requested DA-1 amount from your taxable income. Not in my case. And I tried it for different income values. So it is still worthwhile for me to execute the DA-1 process.

But it still makes sense to apply wealth management fee deductions to reduce taxable income, instead of increasing the maximum DA-1 reclaim. So I guess it depends on the amounts involved. Calculations required…

It will always make sense to use the wealth management deduction, as marginal tax rate is applied. Whereas for the DA-1 calculation, the average rate is used.

Question is whether at least the 2’250 of WHT paid could be deducted to reduce double taxation? Depending on your tax rate, it’d still be a few hundred more than 0.

Absolutely agree.

I have been looking at these calculations and thinking about mortgage scenario ( potentially in a few years)

With mortgage, it might be meaningful to move to the non US part of the ETF portfolio to UCITS or Swiss based ETFs so you have zero L2 WHT tax compared to 15% on the US domiciled ones. This will reduce your DA-1 relevant assets and DA-1 relevant dividends, so a considerable lower percentage of DA-1 refunds lost. All this while benefitting from the zero L2WHT on non US part and deducting same amount of asset management costs at marginal tax level. Does this make sense ?

if 2’250 * marginal tax rate < max amount for reclaim then execute DA-1 process

I don’t have that much DA-1 dividends yet, so it’s still worth it for me, even if the max amount of reclaim is much smaller than the WHT.

I don’t have a mortgage either.

It does, at least that’s what I’m doing. Will call the tax office next week to maybe find a solution. For the next declaration, might just skip DA-1 and reduce declared gross income by the WHT.

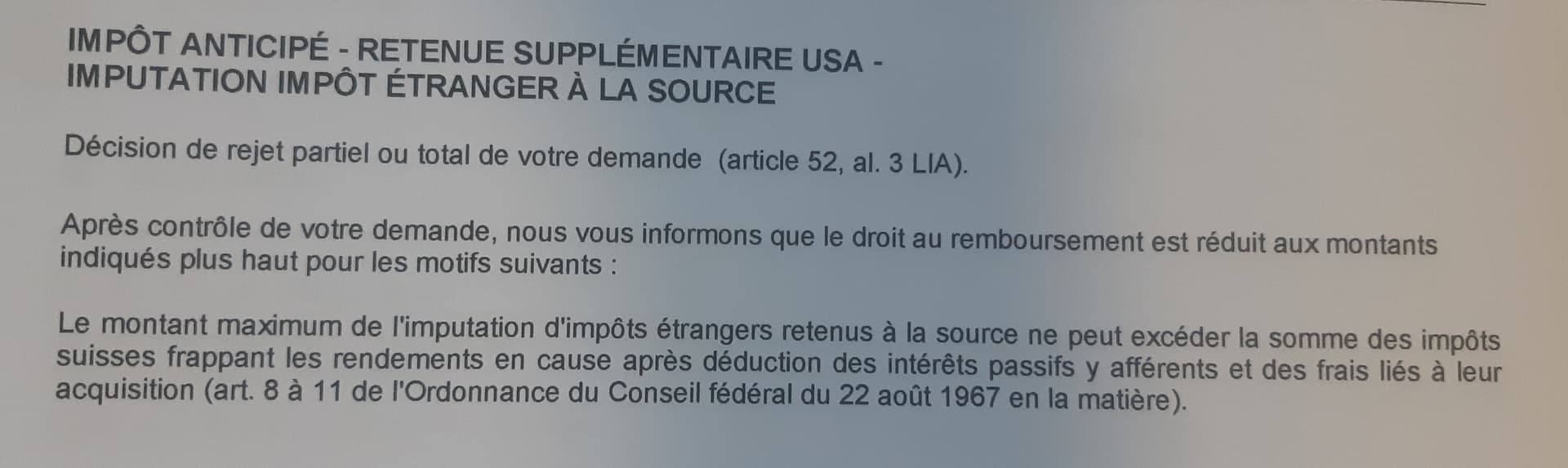

Hello! I may need some help to understand this. The Vaud Tax office send me back this letter, regarding my DA1 refund and I barely understand what they mean… I understand French very well but this wording is too complicated to me and to my native french speaking partner I guess. Do you have an idea?

Thanks for the answer. Ok, let’s see… No, they did not provide any detail other than that sentence.

I deducted portfolio fees that were quite low (less than 100chf), in my IBKR account I use a small amount of leverage (less than 10% of my total porfolio) that I declared as debt. For the rate rate no, it is not below 15%.

You say that because you think that my declared debt + fees are higher than the amount of WHT I asked to be refunded in the DA-1. I think this is the case but I don’t get why my debt is relevant to be refunded the WHT, are they not two separate things?

Deductions effectively reduce the Swiss tax rate you pay on dividends, so your effective Swiss tax rate on dividends may fall below 15% even if your overall income tax rate is above 15%.

If your wealth income deductions are higher than your wealth income, you effectively pay no Swiss taxes on dividends, which means there is no double taxation and thus, you can’t get a DA-1 tax credit.

How the calculation works is described in this thread and DA-1 Refund calculation. If they don’t provide the details and you need help calculating and/or understanding this, you need to provide numbers:

Total wealth income (interest, dividends and [imputed] rental income)

US dividends (part of the above)

Wealth income deductions (wealth management, debt interest, house renovation)

Overall income tax rate

I think that should be enough to at least approximate the correct DA-1 tax credit.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.