Does anyone know if “Bruttoertrag” here refers to total taxable income from your assets or only the income from the foreign dividends?

Say I have some ucits funds and some swiss funds, that have no withholding tax, but contribute to my total income.

This woudl pretty drastically change the reclaimable amount (in case of high debt deductions) of withholding tax and justifies optimizing domicile of your funds (i.e. use ucits funds for ex-US holdings).

Damn this is what I feared… I thought I could optimize, but knwoing this, there is almost no advantage going with partially ucits funds in my calculations. (purely for DA-1, for other tax reasons still can make sense)

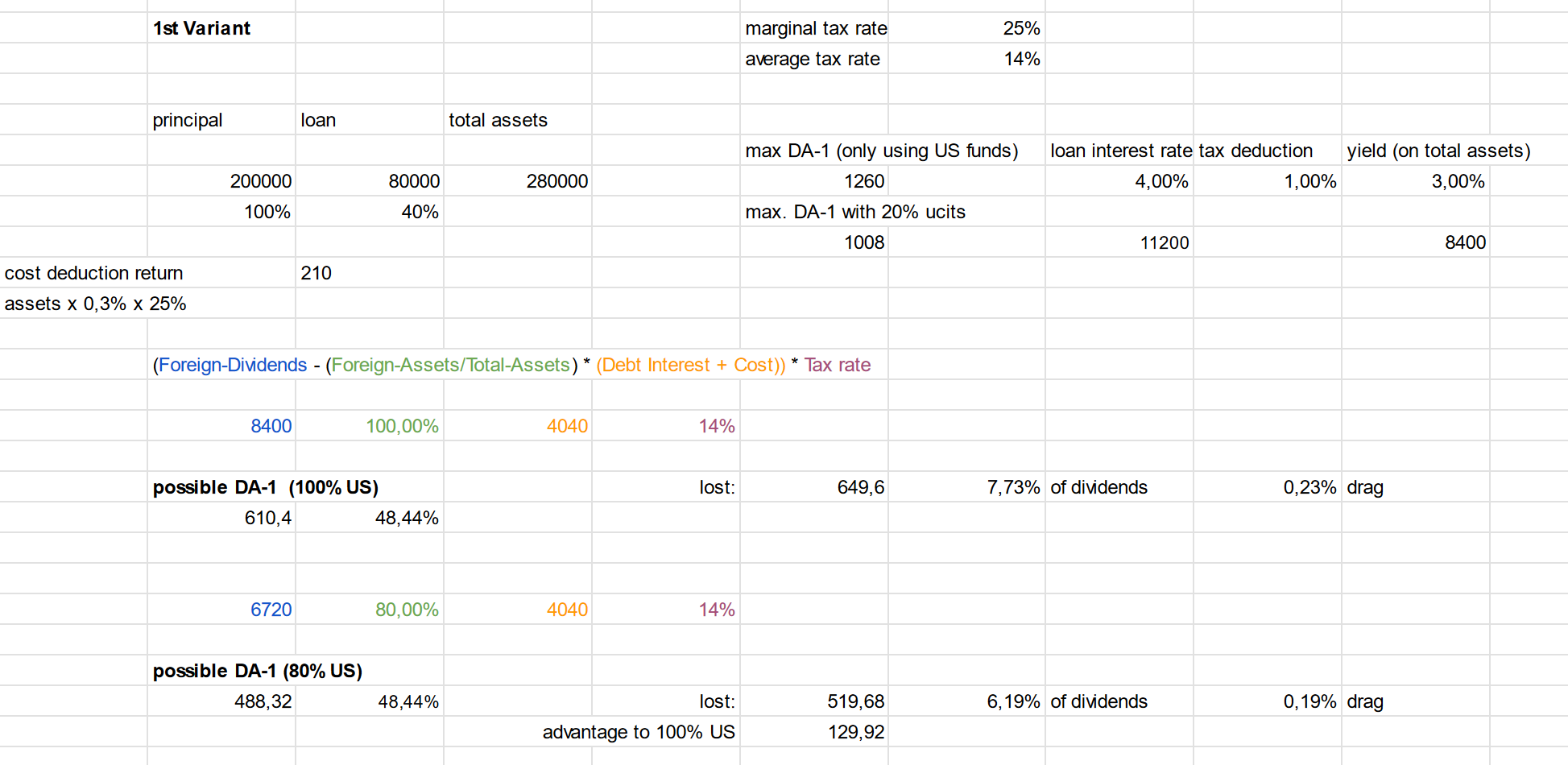

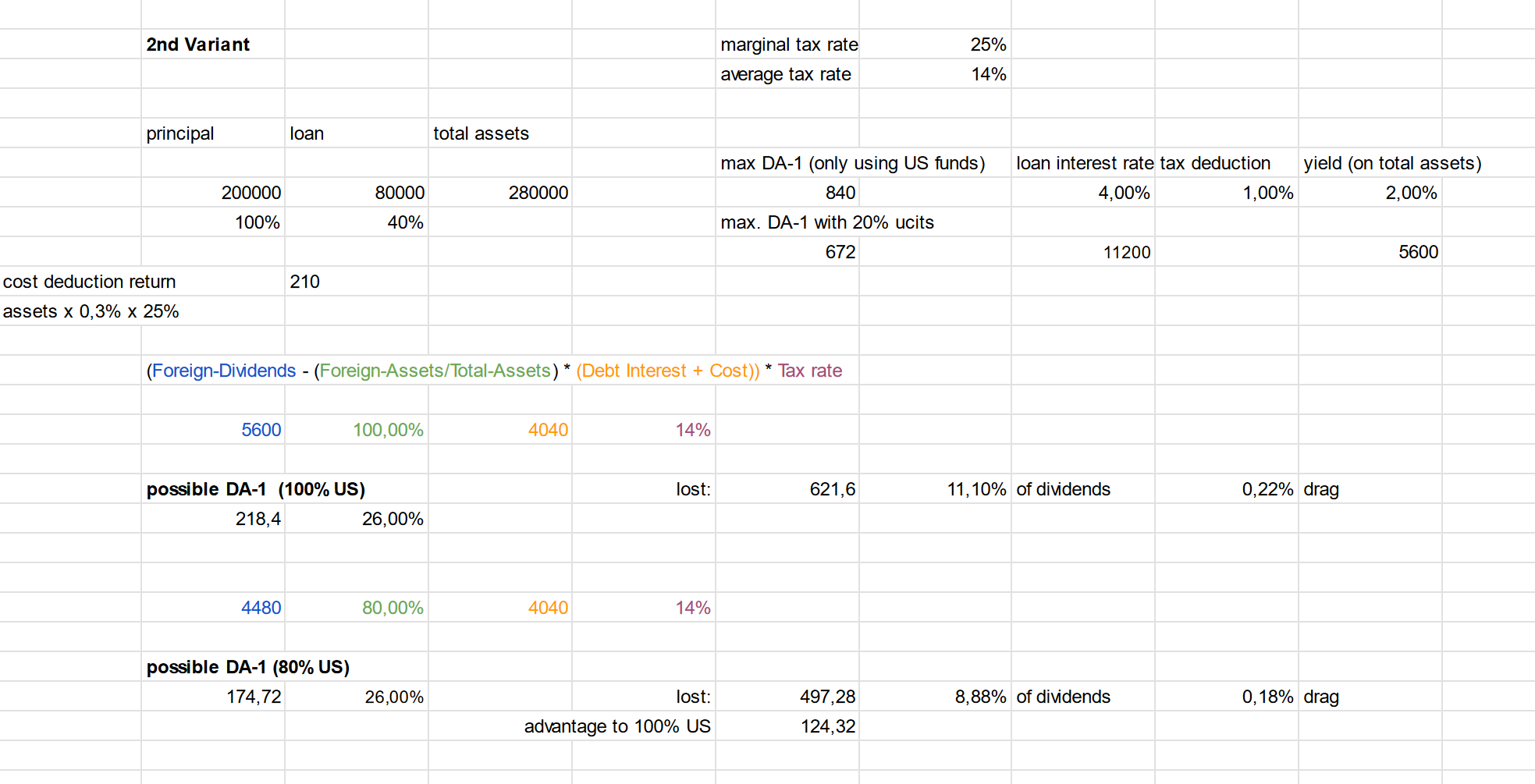

Keep in mind there’s two parts in the deduction calculation: Wealth management cost, based on the income and cost of debt, based on assets.

As a thought experiment, what if … … one were to shift some DA-1 assets to non-DA-1 end of year? This could tilt the result significantly, even from 0% reclaimable back to 100% depending on your parameters.

It’d result in the same level of income and assets reported. Could the tax office still find any offense in doing that?

If one were to shift assets to non-DA1 at end of year and move them back to DA-1 at beginning of year , for the sole purpose of saving taxes, then it is similar to following

Changing your address to Zug in dec and moving back to Zurich in Jan.

Gaming the system is never good. We are lucky to be in country with friendly tax office. Let’s focus on not tricking them. Once they get upset, they would go after you

You would not game the CH tax office here, you‘d game the US IRS from collecting withholding tax from you. CH would get roughly the same tax amount from you still.

CH does not care about the IRS.

The wealth management cost deduction is included in the formula.

I‘ll try to make the sheet public maybe, without doxxing myself.

Shifting assets out of the US at the end of the year doesn’t reduce US withholding taxes, except for dividends that you would have received after that point. And if the US deducts the same WHT but Switzerland’s DA-1 tax credit is higher, CH would obviously not get the same amount of taxes from you anymore.

It’s a serious question, not a “gaming the system” type. Deducting mortgage cost is not meant to be a cheap loan to invest, but to partially offset the imputed rent which is taxed as income, yet not considered in the DA-1 amount calculation.

Might be a different angle if you actively borrow money to invest, where there are court rulings that your debt doesn’t need to be directly used for DA-1 assets to still be included.

Switzerland does have those tax treaties to avoid double taxation. The idea here is not to pay less taxes than you owe, or “trick” anyone, but to avoid paying twice.

In spirit, to me this is different to, for example sell and re-buy around dividend dates. Switching residence back and forth to avoid taxes seems an unfair analogy, as well.

Question is, whether the tax office, or a court would see it like that, as well, if it came to discussion.

I think as per tax office , their objective is that you don’t get taxed twice on your net wealth.

So when they reduce mortgage payments from DA-1 income, this kind of shows that as per them you don’t get credit because you didn’t get taxed twice in first place (Mortgage payments reduced income and hence no tax)

If they wanted to compensate for imputed rent then they should have added that number to this reduction calc for example

DA1 dividends - mortgage Payments + imputed rent

But they didn’t. So this makes me think they don’t consider imputed rent as unfair and hence their thinking might defer from yours.

Oh yea, I wrote that already being in bed and misinterpreted it a little

In the back of my head I had my portfolio, where most distributions will be end of the year.

But that would be avoiding some dividends, depending to what funds you switch.

Either way, I think there is lots of potential to optimize legally.

One thing I thought about is using a big part in swiss home bias funds for your developed international exposure to avoid WTH alltogether + a small tax free distribution.

The ucits managed futured funds I use are wth free already that‘s set.

Then for emerging markets exposure use a ucits fund as well.

For a generally partial/no Da-1 optimized market cap weighted portfolio (no factors, no alternatives etc.) something like this could be good:

60% US: US domiciled (always better then physical ucits) or a swap based ucits fund (has no wth, but a bit higher cost and only large cap available afaik and only really interesting if 0% DA-1)

30% ex-US developed: 20% swiss market funds, 10% ucits EXUS (for some more diversifcation)

10% ucits emerging markets fund

This setup saves you a lot of withholding tax compared to VT.

I’m having trouble understanding why my DA-1 refund request for US dividends was fully denied for 2022 and 2023, while in 2021 it was partially accepted.

I have been waiting for years for a decision on my DA-1 refund request, and I have only now received the response.

Background

• I hold US stocks that pay dividends, and I filed Form DA-1 to reclaim the 15% Swiss-US tax treaty deduction on the 30% withholding tax applied in the US.

• In 2021, my request was partially approved.

• In 2022 and 2023, my request was completely rejected.

Difference between 2021 and 2022/2023

• In 2021, I did not have a mortgage.

• In 2022 and 2023, I had a mortgage.

Reasons for Rejection (from the tax office)

The tax authorities stated that the refund is limited by interest expenses and other deductible costs related to income generation. Based on this, they seem to have concluded that my mortgage interest reduced my taxable income too much, leaving no room for the refund.

My Questions

1. Why does mortgage interest affect the DA-1 refund? If it’s a personal mortgage, why does it reduce my ability to reclaim the US tax?

2. Has anyone else faced this issue? Is there a way to optimize tax deductions to still qualify for the refund?

If anyone has experience with DA-1 rejections or strategies for dealing with this, I’d really appreciate your insights. Thanks!

Let’s say you have income of 1000 in the US and withholding tax of 15% giving 150 of WHT. Let’s also say you have 10k of mortgage interest. If your US assets are 50% of total assets, 50% of the mortgage interest is allocated to the US. Therefore you have 5k of interest allocated to the US.

Now they work out that you had tax of 1000 in the US, but if you allocate 5k of interest expense against it, your US income becomes zero and therefore withholding tax of 15% on that is also zero. So they say you can’t claim any WHT.

The basic principle is that DA 1 is not meant to refund US tax . It is meant to avoid double tax

If your estimated Swiss tax is lower due to mortgage then your refund would also be lower (or zero) and this means that tax paid in US will not be refunded.

Hi,

I live in Canton de Vaud and started investing in VT (through IBKR) in 2024.

I’ve just received my 2024 tax decision and noticed that the Vaud tax authorities did not refund the full 15% U.S. withholding tax on VT dividends (even though I filled out the appropriate form). They only reimbursed a small portion of the 15%, explaining their decision as follows :

"Withholding tax – additional U.S. withholding – foreign tax credit … we inform you that the right to reimbursement is limited to the amounts indicated above for the following reasons : The maximum amount of foreign taxes withheld at source that can be credited cannot exceed the total Swiss taxes levied on the related income, after deducting the corresponding passive interest and the expenses related to acquiring said income (Articles 8 to 11 of the Ordonnance du 22 août 1967 relative à l’imputation d’impôts étrangers prélevés à la source).”

Or, in French :

"Impôt anticipé - retenue supplémentaire USA - Imputation impôt étranger à la source … nous vous informons que le droit au remboursement est réduit aux montants indiqués plus haut pour les motifs suivants : Le montant maximum de l’imputation d’impôts étrangers retenus à la source ne peut excéder la sommes des impôts suisses frappant les rendements en cause après déduction des intérêts passifs y afférents et des frais liés à leur acquisition (articles 8 à 11 de l’Ordonnance du 22 août 1967 relative à l’imputation d’impôts étrangers prélevés à la source)."

I had never seen any mention of this reduction on the websites and forums that talked about VT and Swiss taxes. I must specify that my tax situation is not extraordinary in one direction or the other (I own my home with a mortgage debt, and have income and finances “in the average”.

To be more precise, in my case, I held some VT for the first time in 2024. The yield on VT was CHF 1,293.65, and the 15% withholding by the US was CHF 189.55. The Vaud tax authorities reimbursed me only CHF 25.85.

I suggest searching this forum, this has been asked and answered many times. You can also read the DA-M, which explains it.

In short: the tax office credits you only up to the amount of Swiss taxes you would have had to pay on the dividends (which is apparently CHF 25.85). If the US WHT is higher than that (which in your case, it is), you’re out of luck.

Thx, I should have paid closer attention . I’ve also asked the tax office to provide the details of the calculation. The employee told me he handles that manually (by filling out a calculation form), so it could be useful to check anyway. In 2025, I will have way more VT, so better to understand now than later.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.