As we reach the end of the year I have been looking at supplementary insurance packages to try and determine whether any are worth my while.

I’ve found some of the options from SWICA to look almost ‘too good to be true’.

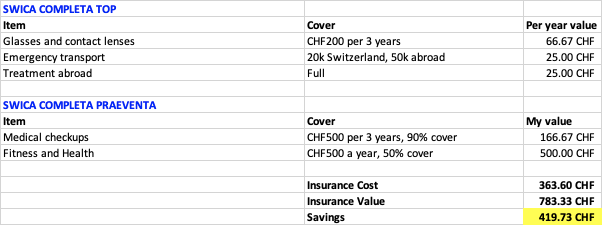

If you take the SWICA COMPLETA TOP package you can add on the SWICA COMPLETE PRAEVENTA package. This comes to a total cost of CHF30.30 per month or CHF363.60 a year.

This assumes you wear glasses/contact lenses, travel to the US/Canada/Australia every now and then so benefit from insurance abroad, have a medical checkup every few years, and go to a gym or do sporting actives that cost over CHF1k.

By my personal calculation this package would save me over CHF400 a year.

And thats ignoring the other benefits such as alternative treatments, alternative medicines, maternity, home help, spa treatments, orthodontics (if you are under 25), medically prescribed aid contributions (e.g. wheelchair), and vaccines (which work for travel).

Am I missing something? How do they make money with this insurance when the gym benefit alone (CHF500) is more than the annual cost (CHF363.60).

Insurance mathematics is a complex calculation. They don’t need to make money on the single patient, but on the whole group of insured people.

Also, they don’t have to accept you as a customer. They can deny your application without any reasons and there is nothing you can do against it.

In my opinion, Swica offers the best supplementary health insurance in terms of value for money. They make money because the vast majority of policyholders do not make full use of the benefits. The business model here is that they require you to take out their compulsory health insurance in order to be eligible. Swica’s compulsory health insurance is not among the cheapest (in most regions). What they charge in compulsory health insurance premiums makes up for the supplementary insurance benefits.

It’s worth noting though that insurers are not allowed to terminate a supplementary health insurance policy when a policyholder terminates their compulsory policy. That means you can move to a cheaper compulsory health insurance policy after 1 year and keep the supplementary health insurance. Over the long term that would certainly pay off - if you actually use the benefits.

Do they require you to take out their compulsory? I selected just the supplementary package on their site and it seemed as though they would let me apply (although I haven’t done it just yet.)

This would make a difference for sure (current basic is CHF171 vs CHF250 quoted here). Smart idea to cancel after 1 year.

I’ve decided to send in the application for Completa Top + Completa Praeventa (CHF363.60/year).

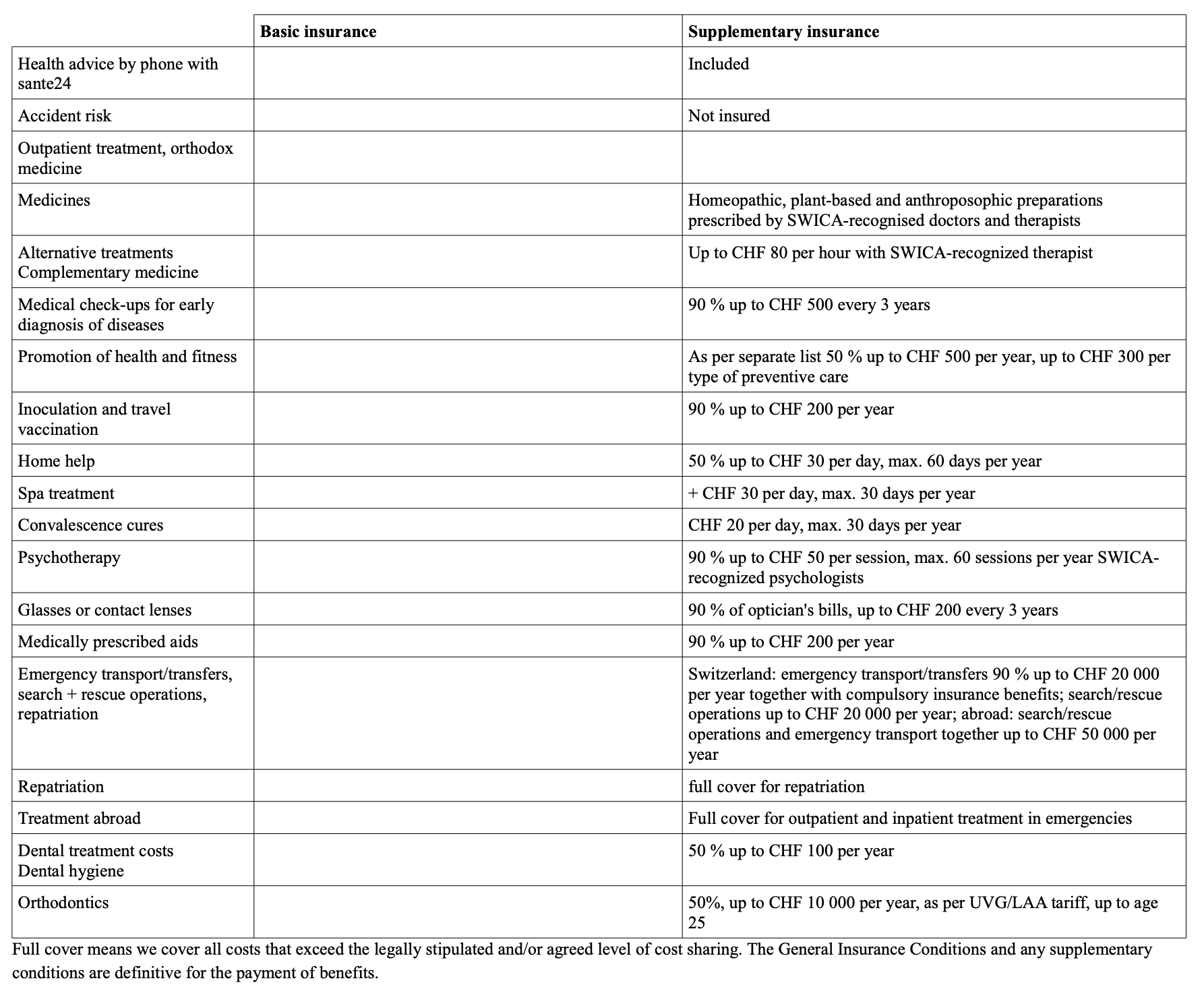

The benefits on the application form are shown below. It seems there is even a dental hygiene contribution of 50% up to CHF100 a year they don’t put on their website. (this sold me over)

If of any interest my line item assessment of the value add per year is:

Medicines CHF0: Will probably never use any alternative medicines not covered by basic insurance.

Alternative treatments CHF5: I believe there is a CHF600 deductible for this and then CHF80 a session. Apparently this works for massages so if I ever wanted weekly massages later in life this may save me some CHF.

Medical check-up CHF75: Assumes I get a medical check-up every 3 years which costs CHF250.

Promotion of fitness CHF370-CHF500: Note that even though it says up to CHF300 per type of preventative care if your gym has a sauna (which all gyms in CH seem to have) that counts as a second type. I currently use ActivFitness (has a sauna) at CHF740 a year so this would only save me CHF370. But if I found some other promotion of fitness or joined a more expensive gym could get to CHF500.

Travel vaccines CHF10: Every decade I may need a yellow fever vaccine or something.

Home help CHF1: I was wondering if you could get a subsidised cleaner here . Sadly not so no value for me for now at least.

Spa treatment CHF1: It seems this is only with a prescription if you get pneumonia or something.

Convalescence CHF0: No idea what this really is.

Psychotherapy CHF0: Probably never use this.

Glasses or contact lenses CHF66.67: As I wear glasses and use contact lenses I should be able to claim CHF200 per 3 years here.

Medically prescribed aids CHF1: If I needed a wheelchair someday I may find some value.

Emergency transport/transfers + Rescue operations CHF50: Swiss ambulances seem to cost about CHF1000 with basic insurance covering half (so CHF500 out of pocket.) This covers 90% of it so saves you an extra CHF400. Assume 1 ambulance a decade and the abroad insurance value.

Repatriation CHF5: Can be very expensive; good to have insurance for.

Treatment abroad CHF25: Full cover is great for US and Australia where basic insurance at 2x Swiss costs may not be enough. CHF25 assumes about 1 week a year in the US for me.

Dental hygiene costs CHF100: I do a yearly teeth check-up and cleaning which comes to about CHF200.

Orthodontics CHF0: I am almost 25 and doubt I would use this.

So my value calculation for this package comes to CHF710 to CHF840.

Yep, as a rule Swica only sells the supplementary insurance in a package deal with compulsory insurance. I don’t know how hard and fast that rule is, but that was their response to my inquiry. If you use standard compulsory insurance with a 300-franc deductible you can also change to another insurer mid-year. But obviously the standard model with the minimum deductible is the most expensive so I don’t image many mustachians use it.

If you have children, the orthodontics coverage is a huge plus. It only applies up to age 18 so no good if you don’t have kids. It’s worth noting that the prevention benefits go a lot further than just gyms. For example, they also cover dance classes, visual training, public swimming pool abos and rock climbing center memberships. Of course, only up to the annual allowance for all preventative measures combined.

Follow up question to this: does anyone know if you can take out a CHF300 deductible basic health insurance policy, cancel it mid year and swap back to a CHF2500 one?

Also if a health insurance provider wants to raise supplementary insurance premiums do they have to raise them for everyone with the insurance? Or could they just single out me?

No. Annual check ups are covered by supplementary and it’s not even 100% clear what they mean. I mean, you could do so many things in an annual check-up.

Because if you have say a problem with your ankle and you plan an operation on February, you get the 300 franchise, do the operation and then change it back to 2500.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.