“We have been providing loans for financing our automotive deliveries during [accounting period]. We have recorded net financing receivables on the consolidated balance sheets, of which [amount] is recorded within Accounts receivable, net, for the current portion and [amount] is recorded within Other non-current assets for the long-term portion”

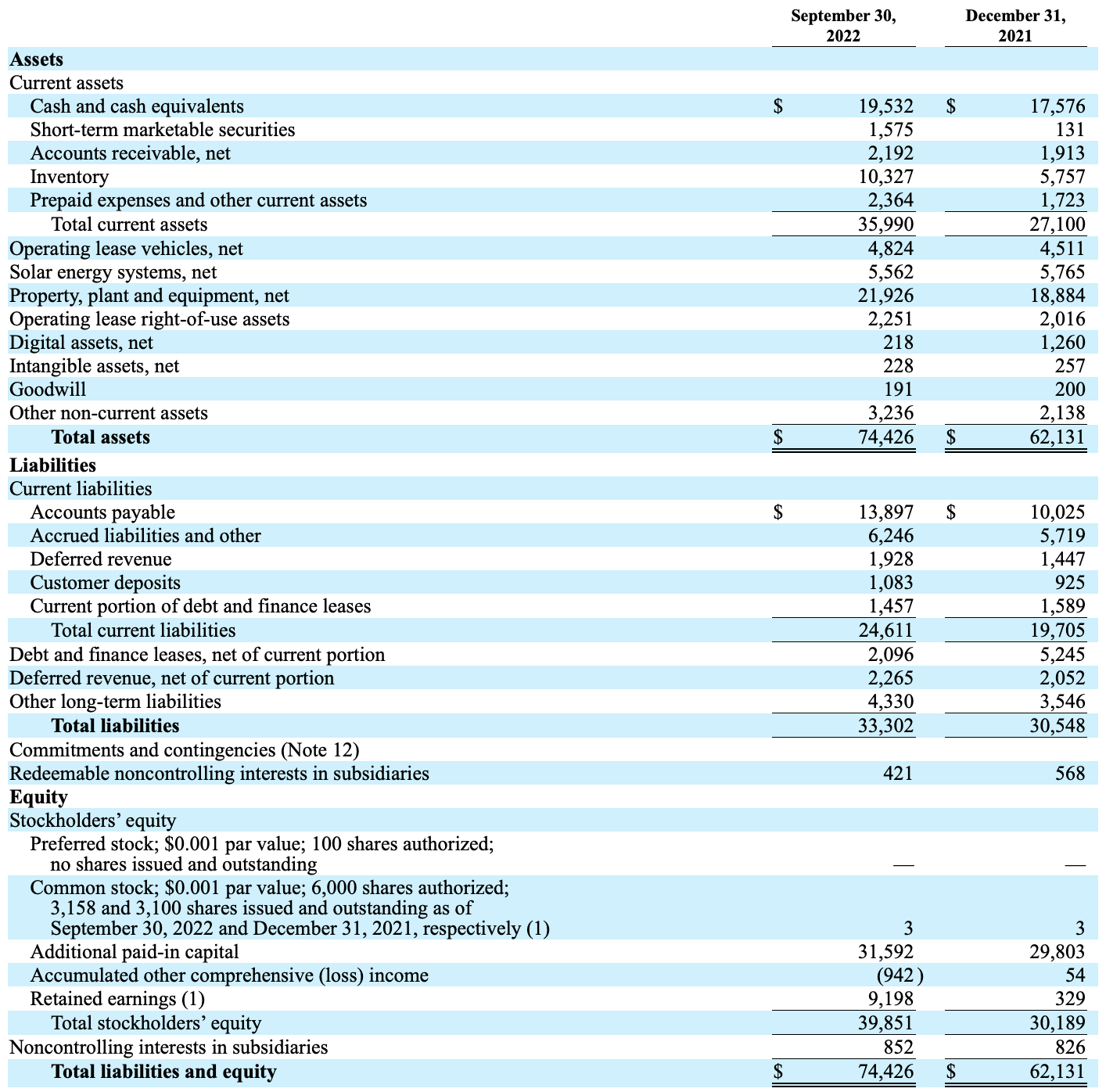

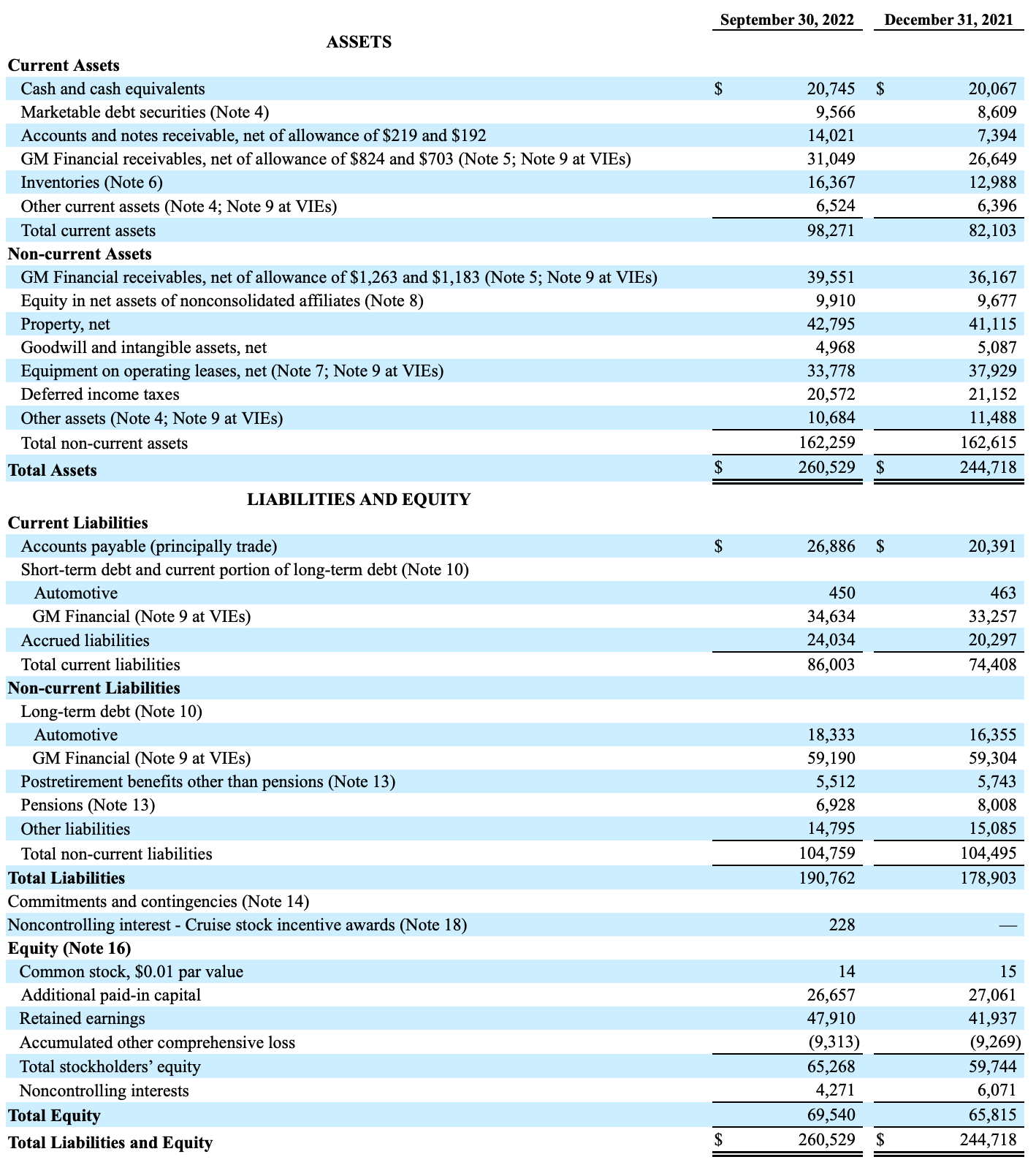

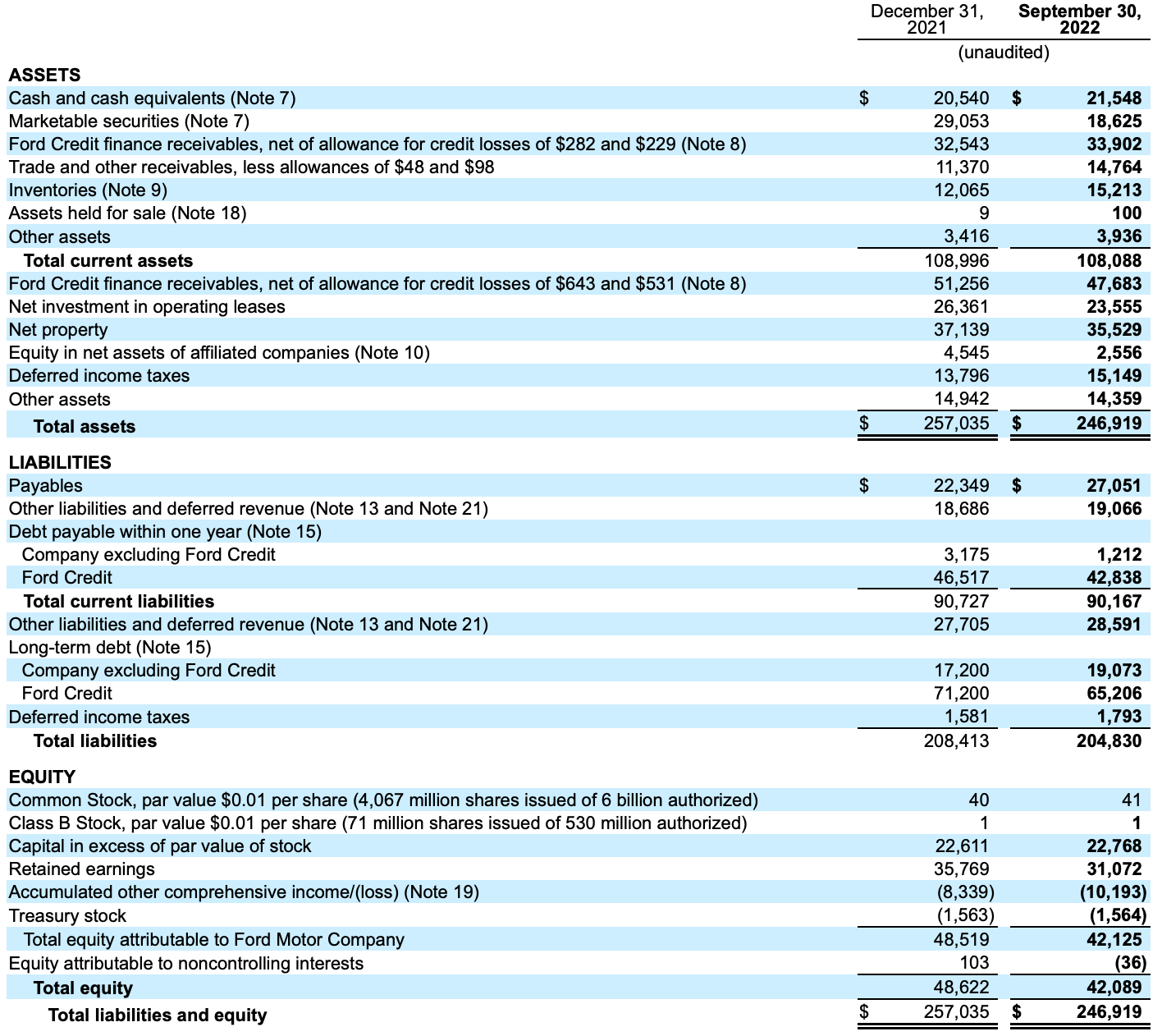

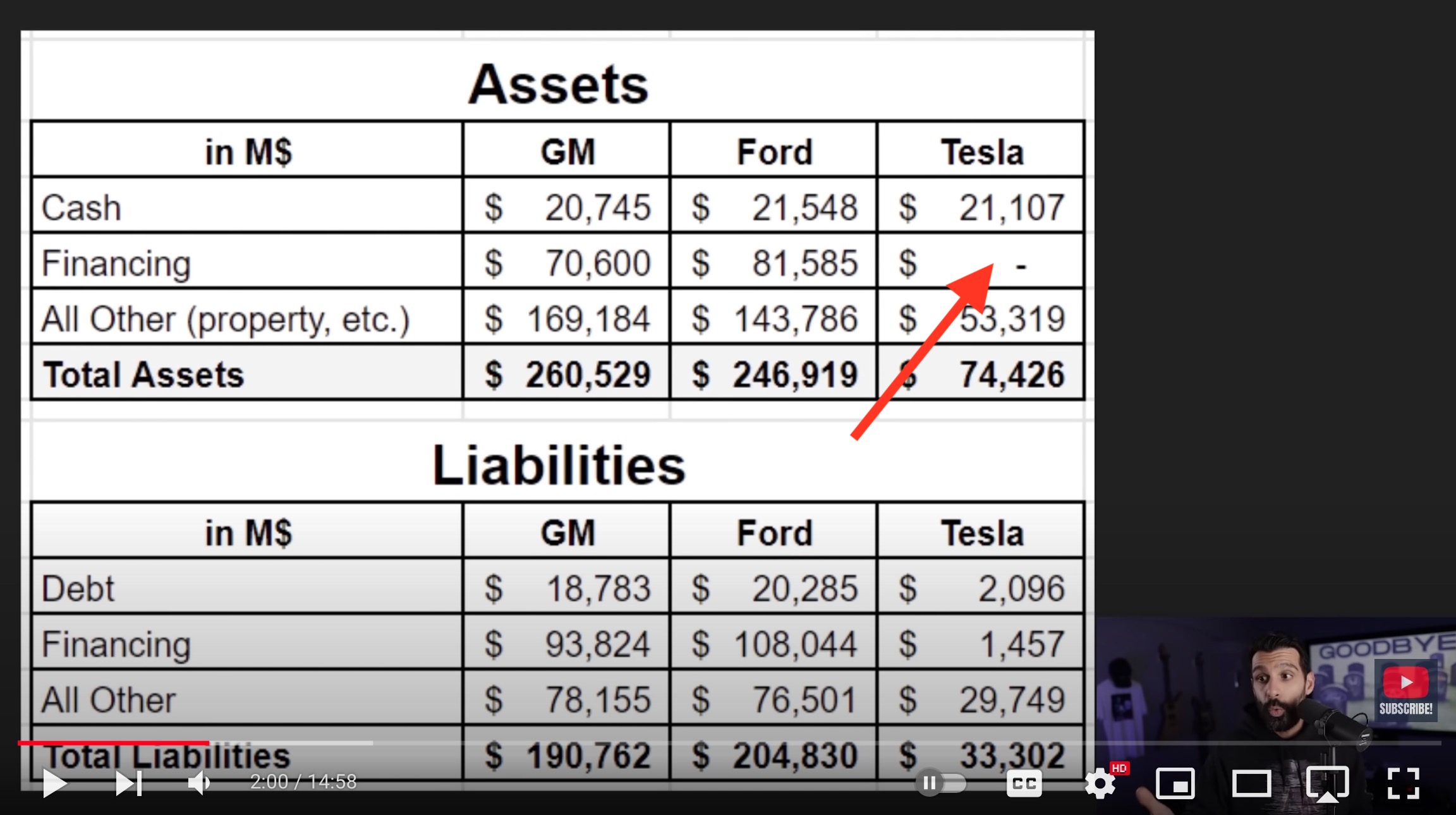

Assets / Ford Credit finance receivables: 33,902 + 47,683

Assets / Investment in operating leases: 23,555

Liabilities / Ford Credit: 42,838 + 65,206

So we can see that F & GM have massively higher Credit/Financial operations than TSLA.

What I don’t understand is why assets and liabilities for GM Financial & Ford Credit aren’t equal. Maybe some balance sheet guru could answer. @Julianek

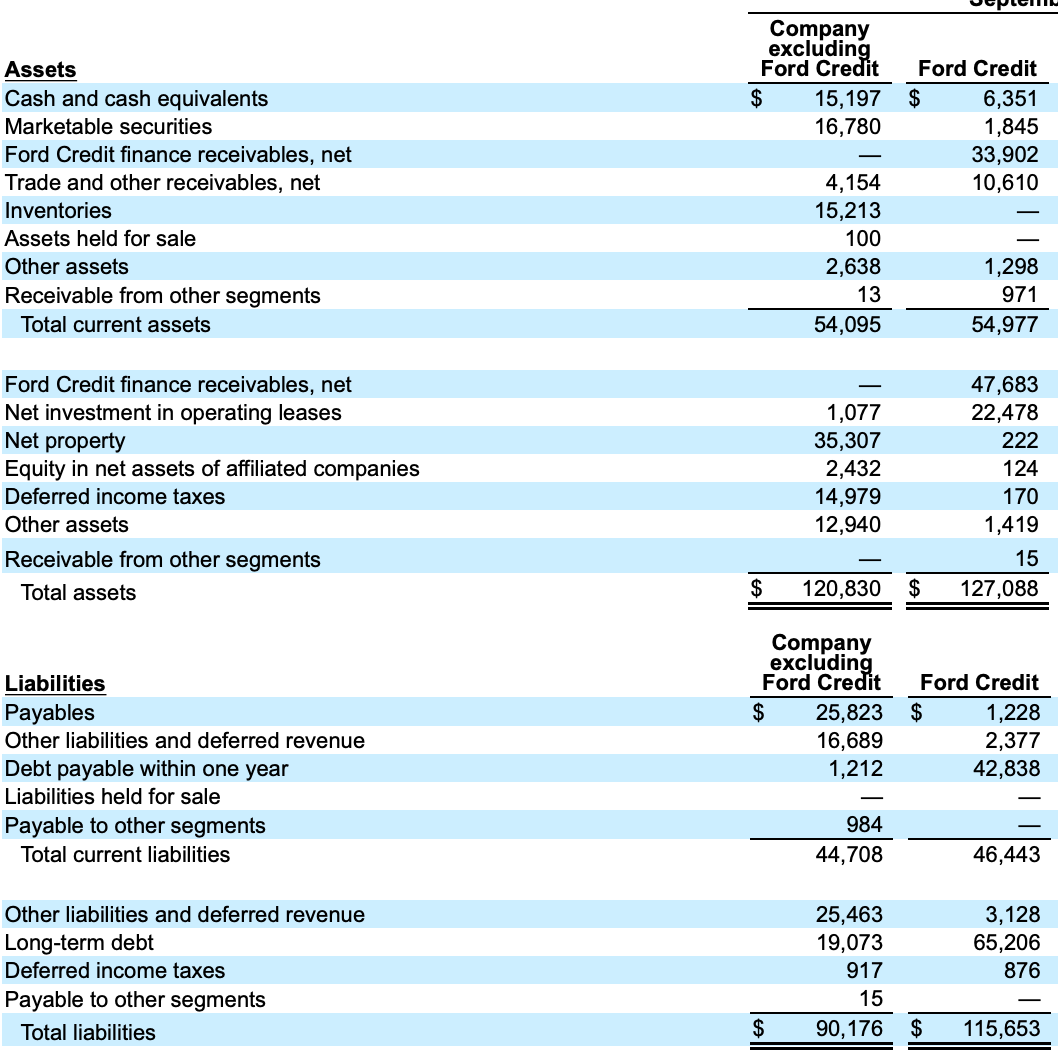

Oh, and here’s Ford Credit isolated from the balance sheet of the entire company. @San_Francisco this goes to show how big Ford Credit is for the entire company. It’s like half of the balance sheet.

Now what happens if we run into a recession, customers stop paying their installments and start defaulting on their loans. The customers might try to sell their used ICE Fords, but they will be surprised to learn that the resale value is much lower than they thought.

Leasing is not financing. See my previous post above.

I’m not buying the whole argument as much. As user137 said above, it’s the narrative of Cathie Wood and the fanboys.

The recession may arrive soon. But unemployment figures are low. And considering how car-centric their society is, one of the last things, I imagine, US lenders will risk is having their car repossessed.

And the impact of EV on used car sales is much longer away.

Take these numbers for 2021 (I briefly referenced the plausibility with other estimates):

I don’t get it. Ford classifies leasing as part of Ford Credit. In leasing, the cars belong to Ford right? So after the leasing, the cars come back to Ford. Which could potentially be even riskier.

But find me in this balance sheet, how many loans Tesla has given, as you claim that they offer loans.

It’s north of $100B for Ford in outstanding loans. This is a lot, especially if you compare it relative to the size of the actual car business. You can think these are some fanboy theories, only time will tell.

I haven’t looked at the figures in detail.

All I pointed out was how you are confusing things.

You said customers don’t owe money to Tesla, since they don’t provide loans themselves.

Apparently Tesla does provide financing themselves and has that on their balance sheet (my quote from 10-Q).

In response to that, you quoted their “Operating lease vehicles” figure of “4,824”.

That is leasing. Not financing, which they’ve recorded under accounts receivable and other non-current assets (again, see my quote above).

What I don’t know, since I didn’t dig into these numbers in detail, is whether there’s substantial other positions included in accounts receivable and other non-current assets).

Accounts receivable, net, for the current portion and [amount] is recorded within Other non-current assets for the long-term portion

We have been providing loans for financing our automotive deliveries during the nine months ended September 30, 2022. We have recorded net financing receivables on the consolidated balance sheets, of which $76 million is recorded within Accounts receivable, net, for the current portion and $398 million is recorded within Other non-current assets for the long-term portion, as of September 30, 2022.

Don’t know why you removed the dates and amounts from your quote. So it’s under $500M, compared to $71B for GM and $82B for F. I don’t think you mean to say that the scale of the car business of F & GM is 150x bigger than TSLA?

“We offer financing arrangements for our vehicles in North America, Europe and Asia primarily ourselves and through various financial institutions. We also currently offer vehicle financing arrangements directly through our local subsidiaries in certain markets.” (Tesla 10-Q filing for the period ended 30 sep 2022 (note: same as where the YouTuber got the financial statement figures from))

“We have been providing loans for financing our automotive deliveries during the nine months ended September 30, 2022. We have recorded net financing receivables on the consolidated balance sheets, of which $76 million is recorded within Accounts receivable, net, for the current portion and $398 million is recorded within Other non-current assets for the long-term portion, as of September 30, 2022.” (Tesla 10-Q filing for the period ended 30 sep 2022)

“In 2017 [Farzad Mesbashi] joined Tesla based out of Bethlehem PA, helping the ramp of the company’s parts distribution network in the US and overseas. He left Tesla in 2021 after a successful build out of the network as a Program Manager.” (https://www.farzadmesbahi.com)

An ex-Tesla manager operating a YouTube channel full of videos about Tesla.

Making an assertion about facts that any ape with a can easily verify as wrong in mere minutes.

…and charging his followers on Patreon for the privilege of that.

Though I can’t say I’d be surprised if the guy is still loaded with employee stock options.

I’d rather watch funny cat videos than base my investment advice/decisions on such YouTube videos.

This was not the question, but if these 71 and 82 billion dollars come home to roost - if only partially, like 10% will default, that’s still a massive number of loans failing.

Although the reposession and selling these cars might not be that damaging financially to the car manufacturers, as their leasing contracts are usually very one-sided.

I didn’t delve into the specifics of Tesla’s financing and leasing operations. Whatever their volume, I’m sure it’s only a fraction of GM’s or Ford’s.

Last year alone, Ford sold more than 1.8 million cars in the U.S… That’s more than Tesla sold cumulatively in its existence. I also googled the duration of U.S. car loans and that seems to be 72 months commonly nowadays. Even leaving aside their much bigger international footprint, I am not surprised in their financing activity being much bigger than Tesla’s.

And I don’t see what’s wrong with that - after all, they’re probably charging interest on the financing.

If Tesla had huge financing/leasing on their books, wouldn’t the fanboys laud them for contributing additional income to Tesla’s bottom line “per-car”? “And they’re doing it in-house, foregoing expensive banks and their fees!”

I also have no doubt that Ford and GM have account for possible impairment on their loans.

And the transition to electric cars will be a gradual shift. ICE cars aren’t going to lose their value overnight - especially not in a recession. If anything, people will keep using older cars longer.

PS: All that said… I don’t disagree that Ford and GM may be in big troubles as legacy car manufacturers. Their sales have been declining for years and they may be ill-prepared to survive the EV revolution. But it won’t from sudden overnight depreciation on loaned/leased vehicles.

Also, considering the trajectory of Japan/Korean car manufacturers, I believe it’s premature to lump together all “legacy” car manufacturers in predicting their imminent death.

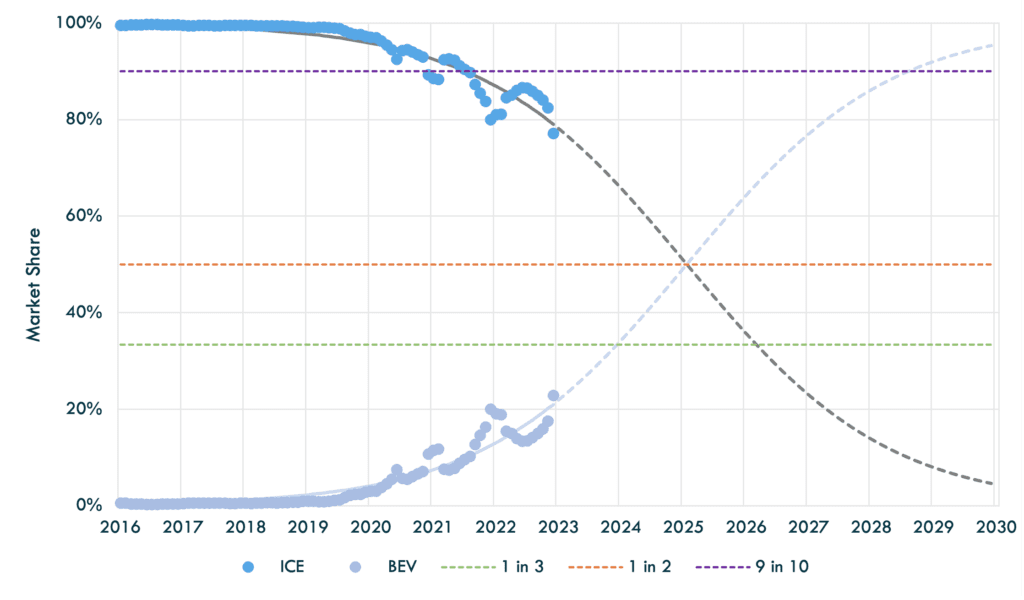

If it is true, we should reach 50:50 parity early 2025, just 2 years from now, and 90:10 by early 2029, 6 years from now. Of course, for the entire World the transformation will be slower, but at least in the developed countries, there isn’t much time left.

The market share of electric vehicles in the U.S. was about 6% last year.

I don‘t know about the regional size of GM‘s and Ford‘s financing and leasing operations - but I‘d be surprised if they weren‘t skewed towards the U.S.

One can make many criticisms to regular auto manufacturers, but not being “agile” is certainly not one of them.

“Agile”, “Scrum”, “Kanban” and similar methodologies are all derived from the Lean Manufacturing approach invented by … Toyota. Since the 1980s, all auto manufacturers have converted to this methodology because the Japaneses were eating their lunch…

Contrary to a popular belief, manufacturers are much more advanced in this type of methodology than many software companies because the underlying business is so more difficult (high capital intensity and low margins). Because the margin of error is so low, they had to adapt and be excellent at manufacturing or die.

For those interested, there are many good books on this topic, including The Machine that Changed the World and The Toyota Way.

On a related note, I am surprised that Tesla does not take advantage of its technological advance to keep innovating and release new models (The semi and the Cybertruck don’t count: the fully loaded semi has 20% the autonomy of a regular ICE semi, and the Cybertruck is currently manufactured manually…)

If I were Tesla, I would have tried to keep releasing new advanced models to keep competition at bay, especially in critical markets like China (which provided 75% of Tesla’s EBIT in 2021). Instead, they seem to be resting on their ageing models and allow fast moving competitors like BYD to stay in the course.

And those Chinese competitors are very good at evolving and appropriating new technology. I mean, in 20 years, BYD went from this in 2003:

to this:

and in December, they have actually sold more EVs than Tesla in China. I am wondering why Tesla let its competitive advantage getting thinner and thinner…

In case people wonder, the source has the following rational: “The alternative model of slower, more linear growth would now be a very risky investment approach to take, hence our emphasis on the non-linear S-Curve as a model for future market direction.”

Am I missing something or is it simply the circular reasoning it appears to be?

One problem these companies could be facing, is that because of low margins, they have put high emphasis on outsourcing parts, if it means saving on cost. Thus, the vertical integration is lacking, and the supply chain is complicated. It’s hard to redesign a whole component, if its pieces are made by different subcontractors, who aren’t sitting in the same building. And I think EVs present an opportunity to redesign the car from the ground up.

I think battery supply is one limitation, and the other limitation is the growth tempo. OK, we have seen a “miss” in 2022 delivery growth, but 40% is still a big number. But I agree that we should see a cheaper model soon if Tesla doesn’t want to keep losing market share.

One thing they might find surprising is how PepsiCo is using them. According to a recent Reuters interview, the food giant will have different use-case scenarios for the trucks carrying soda bottles and cans for Pepsi as opposed to those hauling chips for Frito-Lay. It somehow makes sense because the chips are less heavy than soda. Nevertheless, the difference is staggering, with the soda-carrying truck only taking 100-mile (161-km) drives for now. On the other hand, the Frito-Lay trucks go on longer 425-mile (684 km) assignments.

This is my 2015 Volvo 730. It has two 150 gallon fuel tanks and averages around 6.5 mpg fully loaded at highway speeds of 65 to 75 mph. I routinely go 1,000 to 1,400 miles between fill ups, and it generally takes 15 minutes or less to top off the tanks. That means on a hard week of running, I might spend a total of 45 minutes putting sufficient fuel in the rig to go 4,000+ miles. Tesla claims their semi will go 500 miles on a full charge. Then it will need an absolute minimum of 30 minutes on the most powerful Supercharger around to recharge to 80% … at which point it’ll only be good for another 400 miles, right? And there’s the rub. In many states a trucker can legally and easily drive 700 miles per day. Most OTR truckers won’t even contemplate an EV rig until the range is a guaranteed 800+ miles under full load, at average highway speeds of 65 to 75 mph, across any terrain and at any temperature, from 125 to -40 Fahrenheit. That way we could drive our 700 miles per day and charge the rig while we take our 10 hour break. So in order to go 4,000 miles per week, you’re looking at spending well over 300 minutes sitting at a charging station - that’s AT LEAST 5 hours the driver won’t get paid for, vs. the 45 minutes for a diesel rig. You see, the vast majority of OTR drivers are paid by the mile. We don’t actually get paid for fueling - or charging the batteries. Raise your hand if you’re willing to work at least five extra hours per week without compensation… And of course, that’s assuming you can find a semi charging station - I haven’t seen a single one yet.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.