I don’t think it is related to the Tesla products. You see the same pattern with AMZN, META and others.

The drop is related to the Fed’s tightening - here its effect on short duration bonds:

It has an adverse influence on speculation.

Also interesting:

Fed executives have sold their stocks in autumn 2021 for “ethical reasons” …

Insiders of TSLA, AMZN, META, and others (do you own research!) only trades since then were: SELL !

About insiders: good point, since insiders often get free shares or stock options and sometimes want to buy a house or a fancy car. However, you can look on OpenInsider, they sometimes buy shares too. I also see from time to time insider buy/sell ratios published on financial portals.

About rates: probably various durations have their importance. Short durations rates influence what people decide to do with their cash: savings account, or gambling on the stock market ? — exactly as Papa Elon says in the tweet above the tweet you cite.

Short durations are also influencing the margin loans, IIRC (I don’t do investing on margin, but there are certainly answers on this forum about which duration serves as a reference).

Typically the 10-year yield is compared to the stocks dividend yield, but in this case it is irrelevant (no dividend).

Anyway, it doesn’t matter too much: all durations’ yields (from 4 weeks to 30 years) are significantly higher now than one year ago.

Tesla is more than an acute case of insider selling:

From inception to today, the company raised $32 billion in equity capital and earned a cumulative profit of $9 billion. Book value, firm equity, sums to $41 billion. The CEO has sold $40 billion of shares (all given as options), and counting. Almost all the cash and resources that ever went into the company ended up in Musk’s pocket. We will see how it goes at the end, but I have rarely seen such a transfer of resources.

It might be that the company will grow so much that this won’t matter in the end, but usually shareholders pay for performance after said business performance is achieved.

Add to that his margin loan with Morgan Stanley related to the Twitter purchase. I don’t know at which price level MS will do a margin call, but with the recent price action there is an additional risk about Musk selling a lot more shares to comply to his margin loan (what might mitigate the situation is if the collateral is not only TSLA shares, but also some of SpaceX).

Rates might have caused the price decreases in H1 2022, but I am more convinced that what happened in the last four months is more related to the Twitter circus. It damaged a lot Musk’s reputation of being a genius:

From a business point of view, paying $44 billion for a company having $5 billion of annual sales and roughly $1 billion of earnings is really questionable. Even more when this $1billion does not include share based compensation, and, Twitter being now private, engineers will want to get real cash instead of stock options. No wonder he had to cut the workforce to such an extent.

Even worse is the damage to his brand: when he was talking about rockets, most people don’t know about rockets so he was considered a genius. When he was talking about EVs, most people don’t know about EVs so he was considered a genius. But now that he is talking about software, most of his fan base are tech enthusiasts, very often software developers, and they can detect bullshit when what he says about software does not make sense. I think his interventions on various twitter spaces about wanting to re-write twitter from scratch because the tech stack is so crazy opened the eyes of many of his supporters.

It is a bit sad because it took Elon twenty years to build his reputation, and only three months to destroy it. For many, there is a growing possibility that SpaceX and Tesla succeeded in spite of Musk instead to thanks to him. For SpaceX, it looks like Gwynne Shotwell is really competent at running the company, i have no idea who would be her equivalent at Tesla.

(Actually, let me tone this down a bit. Tesla needed Musk’s promotion skills a lot, especially in 2018 when it escaped bankruptcy).

But enough about Musk, and more about Tesla the company. I have no clue how big the damage to Elon’s reputation will have on the company in the long term. It looks like there is currently less demand for their cars, but maybe this is a short term bump.

In the long term however, Tesla will have to renew its vehicle models, and I am curious about how they will do that, given that they have by far the smallest R&D budget of all auto manufacturers. That would be very impressive.

I am aware they have been recently focusing on the semi truck and the cyber truck, but:

the semi delivered to Pepsico does have indeed a great autonomy when transporting potato chips bags (more than 500 miles). But when it has to transport heavier cargo, like Pepsi bottles, the autonomy is only around 100 miles, which is a bit underwhelming.

Tsla recently announced that they manufactured the first 30 cybertrucks manually which is also underwhelming given that they announced it almost three years ago.

For FSD, I don’t agree with the complaints about regulation, and it being similar to the trolley problem. Waymo managed to reach level 4 autonomy while complying to regulations. They started recently having their first self-driving cars on a commercial basis. If they can do it, I don’t see why Tesla (which is still level 2) could not do it.

Finally, it looks like they currently have a hard time in China. I am not expert at all, so maybe it is only Covid related (although it looks like their biggest competitor, BYD, is executing much better on their territory - for the anecdote, one of the biggest shareholders of BYD over the last fifteen years is… Berkshire Hathaway, but almost nobody is aware of it).

So there is a possibility that all those issues are transitory, that Tsla will continue to grow profits 50% per year. In that case the company would be worth a lot.

But there is also a parallel universe in which competition catch up and demand for Tesla cars decrease in the long term, having an impact both on volume and margins (if the company has to decrease prices, the operational leverage will be big on earnings). In that parallel universe, Tesla would not be worth a lot more than its book value, like other car manufacturers (i.e around $40 billions, so roughly $15 per share. Make it $30 to have a margin of error).

Currently Tesla is trading between those two scenarios. I don’t know which one will prevail in the end, that’s in the too hard pile for me. But both the upside AND the downside are massive, even after this price action.

I am not happy to see Musk or Tesla fail, i just want to see reality for what it is. If Tesla is the best company in the world, I want it to be the best in the world. If Tesla is only another car manufacturer, well then it should be so. What I am against is making retail shareholders believe it is the former when it could very be the latter.

I am sad for the losses, I had hoped you’d had sold a bit of your stake on the way down to protect your wealth. If you are still in it, I have only two (very small) advices:

as said I don’t know which scenario will prevail, but if you are still long, please do a lot of due diligence, there is still a lot of potential downside or upside.

If you stick to it, know that you don’t have to make it back the way you lost it. Above all, please don’t make being a Tesla shareholder part of your identity. This has to be a rational decision, not a psychological one.

Well I for once bought some TSLA at the end of last year. I believe it’s undervalued at the current price. Missing car sales by ~5% shouldn’t make a stock drop 10+%. Well cheaper stocks for me.

Isn’t that’s just your memory of recent prices influencing you?

Can it bounce and go back up? Sure.

But it could also go lower. E.g. if you check the 5 year chart I don’t see much support at current price levels (not that I think TA is really that useful, just saying).

And there was a lot of share dilution too.

Well, this is the same stock that went up substantially on stock split announcements …

I believe their fundamentals are solid and a lot of things would need to go wrong for them to burn thru 19B cash w/o any significant profit within the next 2-5 years.

Well, Tesla seems to have a P/E of almost 40. Compared to 10 for Toyota and 4 for Volkswagen.

Given their valuation - or if they were to justify it - one could argue that missing any sales target may be a red flag.

Investors better have a compelling narrative why Tesla should be worth (relatively) 5 or 10 times a much as other car manufacturers- that have sold way more cars than Tesla.

First-mover advantage doesn’t guarantee long-term success. Considerable doubt has been cast over how much, if anything, their FSD is ahead of competitors (it’s been lagging years behind Musk’s pompous announcements for sure). And the coolness of their cars to recent first-time buyers may wear off like last year’s summer fashion collection from Zara.

Using P/E is just lazy. It makes no sense to compare a P/E of a company whose earnings are growing to the one of a company whose earnings are shrinking.

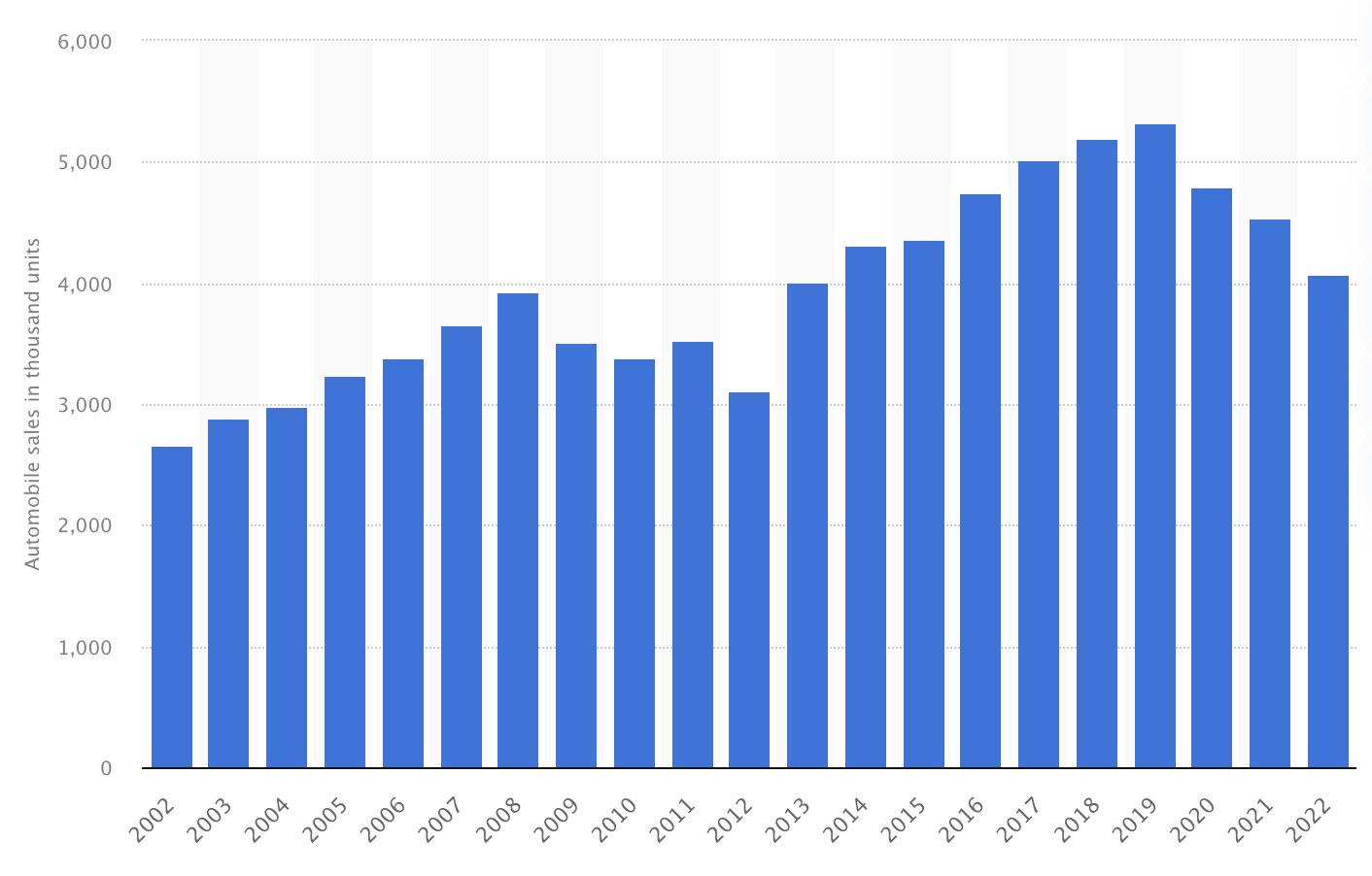

Like Honda, who has sold 4 million cars in 2022, which is like 3x Tesla, right? But notice the trend:

Toyota, Volkswagen, Ford, GM, if I am not mistaken, are actively participating in providing credit to their clients, who purchase their cars. The cars are then used as collateral, and the money is provided by banks. If customer preferences should shift to EVs, the value of these used ICE cars will plummet, and just think how the balance sheet of these carmakers is going to look.

Yes, it is (admittedly) lazy - but so is your retort that it would make „no sense“. I believe it does make some sense - but we shouldn’t just stop at superficially comparing the two figures and call it.

The sensible question is: does Tesla justify its higher valuation - and if and how can or should we make adjustments to better compare the. I think we can probably agree on that.

Seems cyclical.

Like waves.

They sold less cars after the 2007/2008 financial crisis and downturn, only to then propel their sales to new heights.

Looking at that graph, one could just as well predict a third „wave“ of growing sales that starting in 2024 or 2025 and reach new sales records in five years or so. That would totally fit the picture.

Current earnings don’t really matter, they’re in the past. Only future earnings matter. So we should try to estimate future earnings, free cashflow, discount the cashflows which are far in the future, sum them up and that gives us the value of the company.

True, I admit nothing it for sure. But IF the future sales of most current carmakers should collapse in the future, so would their earnings, so it would explain a P/E of 10 or even 4.

A P/E will tell you: if earnings stay constant, how many years will it take for the business to pay for itself. An inverse of P/E will give you the implied annual return. But all that goes out of the window if the earnings should change heavily in the future.

What let you think that Tesla sales will skyrocket in the future (explaining its higher P/E) ? Will it be able to maintain its competitive advantage (if there is any) ?

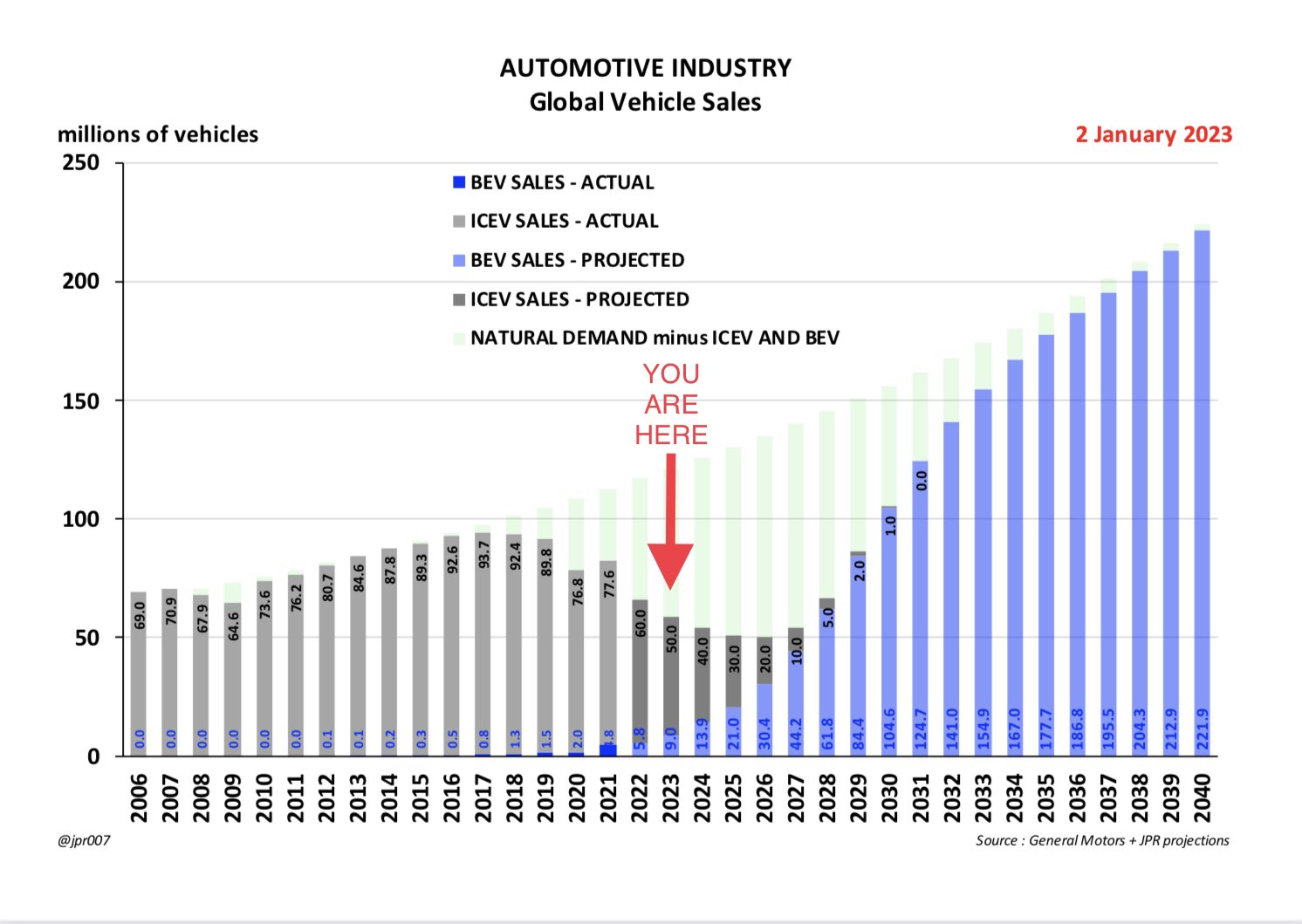

The entire world won’t turn to EV in a night. The shift will take time. Carmakers will increase the %-tage of EV’s leasing.

Most carmakers use a dedicated company (external or internal to the Group) to manage the leasings. Everything is done to reduce the financial risks.

About Tesla and Musk, what are your thoughts about Musk and his shares pledged as collateral for loans ? Do you see it as a danger for the company ? A Closer Look at Elon Musk's Buyout of Twitter

Well, those 3.5 million delivered cars to date beg to differ. At around 60k USD each, that’s 210 billion dollars(!) that didn’t go to other manufacturers. That still doesn’t guarantee long term success, but it’s a heck of a lot of money to build something for the long-term that others can’t.

Not so fast. This is the Cathie Wood narrative and while it has merit, she’s largely discarding what the consumers think about EV affordability (Autoblogist Teil der Yahoo Markenfamilie), the financial nonsense of buying an EV vs keeping your current ICE car until it falls apart, or the longevity of ICE cars vs the lifecycle of an EV past its 10-yr mark.

The way I see it, I would not buy anything else but an EV if I were to buy a new car. However, I’m not crazy and buying cars new is a gentlemen’s pastime. Buying an ICE car 2yr old or new but with huge discounts (albeit, I think this trend will only speed up around 2028-2030) could still be much more profitable than owning an EV for the next 10 yrs (and suffering the huge depreciation of inflated new EV car prices).

The billion dollar question is where do manufacturers get batteries from for all that EV shift? China has the majority of current production, second is Tesla (with Panasonic), third are Korean companies (LGChem, Samsung), the rest are negligible. So until the European manufacturer market doesn’t secure the long-term lithium sources and batteries, they won’t be able to change production, they won’t be able to provide a cost-effective alternative EV as they are not going to have the batteries. Not to mention how crazy complex and fragmented the charging network is outside of Tesla’s Superchargers.

Interesting times we live in. Next 5 years are going to be interesting.

Your question is to explain the entire investment thesis. There are many reasons. To name a few:

Tesla is focused on EVs, does not have the ICE baggage

It has new factories, which are tailor-made to build EVs

It is the largest EV maker, and thus, it has the opportunity to secure the largest, most attractive deals with battery and raw materials providers

the EV market is growing, the ICE market is shrinking

it is vertically integrated, which is advantageous if you’re developing something new. It’s time to rethink the process, remove parts, streamline, before you go and outsource to save a few pennies on some part.

it is using the agile methodology and a flat structure, which means it can implement changes much faster than a traditional company

Tesla is not using the dealer model, saving on cost

it is working on the full self driving technology, which is making visible progress. It is very hard to predict how long it will take, and will it at all be successful, but I like the approach they’re taking. Putting as many cars on the road, collecting data, training the neural networks. Even if there is low probability that they achieve the goal, IF they achieve it, it will be massively profitable, dwarfing the car selling business

beyond car business, Tesla can apply its tech in energy, installing battery packs and even providing arbitrage in energy trading

Don’t try to argue with any of the points I mentioned. I don’t want to do that. I just listed some reasons, and of course everyone is free to believe if each point is good or bad. In the end this is what decides if you invest in the company, or not. It’s not an exact science, but of course you try to build some models and predict future cashflows.

It will take time, but it will be faster than most think. Could even look something like this:

Admittedly, I don’t know how exactly the other carmakers do it, but on the balance sheet they seem to have have financing assets, compared to Tesla. That means they have given loans to customers themselves.

I’m not a fan of the Twitter takeover and I see Elon’s tweets as potentially damaging for the Tesla brand. But I don’t think Elon’s financial situation poses any danger to Tesla. If he’s forced to sell more shares, because he bit more than he can chew, it’s his loss. Things that he and other talented people at Tesla have put in place are there to stay, even if Musk should leave. Of course, I would prefer if he stayed and made sure that no erosion of company culture takes place.

Customer can switch models and car brands when buying their next car.

It remains to be seen how successful Tesla will be in keeping their customers loyal over the long term.

(and fanboys on internet forums won’t likely be the best indicator for that).

As far as I know, Tesla has deals with banks and it’s the banks who give the loans/leasing. Like Cembra in Switzerland. So customers don’t owe the money to Tesla and Tesla is not making money on interest. But I admit I don’t have this one figured out. So could be that I don’t understand something.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.