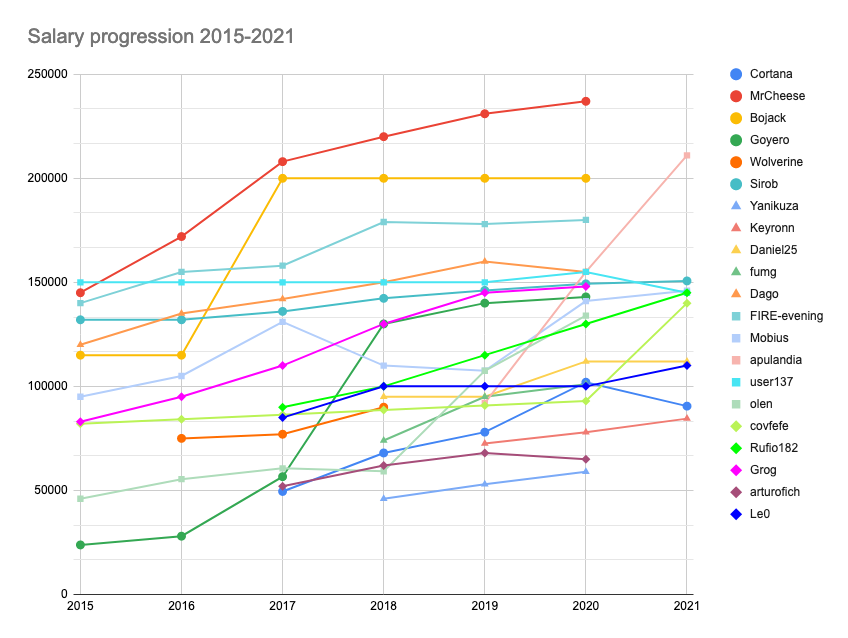

Similar to the post I published about the NW progession, I put all your numbers in a chart ![]()

Here you go:

Unfortunately, it’s a bit messy and unreadable. But hopefully you can extract value out of it.

Similar to the post I published about the NW progession, I put all your numbers in a chart ![]()

Here you go:

Unfortunately, it’s a bit messy and unreadable. But hopefully you can extract value out of it.