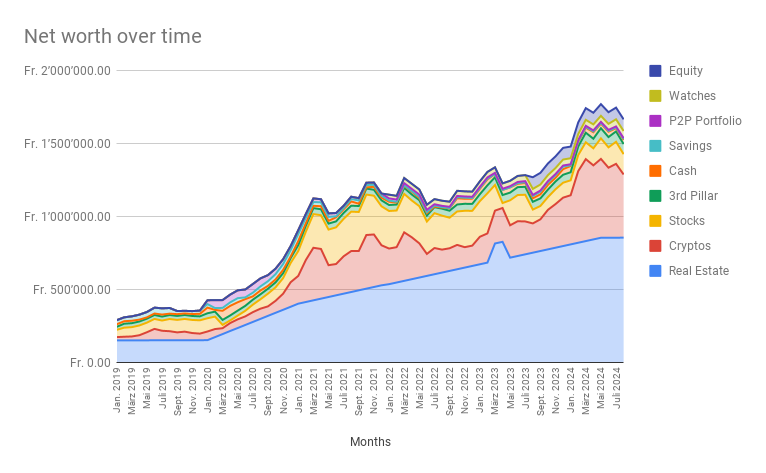

Thanks for sharing Butch - really interesting read!

I wanted to ask you about something not-so-related with investment, but have you and your wife discussed how your lives would be when you retire, but she still has 10 years on her career?

How would things look like, if you don’t work any more and/or travel, while she has a 9-5 job?

Many pension funds require you to transfer in all vested benefits account before you can do voluntary buy in ( and make signed declaration before proceeding).

An in case you do go ahead with buy in without disclosing a vested benefits to the pension fund;

While your contribution gap (or potential total buy in ) may be bigger than the sum of all vested benefit accounts at the time of buy in, what happens if vested benefits account increases in value over the next years and you end up with more buy in than you are allowed. Once this happens you can not put the vested benefits account in pension fund anymore.

"I wanted to ask you about something not-so-related with investment, but have you and your wife discussed how your lives would be when you retire, but she still has 10 years on her career?

How would things look like, if you don’t work any more and/or travel, while she has a 9-5 job?"

Surprising question so I spent a day thinking about it. I’ll assume for the sake of the discussion that children won’t happen. I don’t think much will change. My wife has the ability to work from home 90%. She has previously already indicated (early on in our relationship) that she would rather have me at home, unstressed, doing things I enjoy and with her working than me being so career absorbed… even if that means me making less money. Yes, I am lucky here. I’d spend a bit more time doing the day to day stuff (groceries, cooking, cleaning) and also more time living healthy (riding bicycle, hiking) but no material changes. Keep in mind I’d be spending a half a day a week managing our finances and probably a day a week either with Board or other compensated advisory work.

In case of children, the picture would change but in that case (and assuming I’ll work again) I suspect she’ll choose to become a stay at home mother given we can afford that and it reduces stress.

People working at G, Meta etc are earning 1M+ TC yearly while the normies among us are stuck at 150-250k (if at all).

I know comparing oneself is not healthy, but I’m working for 10+yrs to have as much savings as a Senior staff engineer makes at Meta yearly in stocks alone.

It’s such a leapfrogging rocket if you get into one of these companies with a generous LTI package on top of your regular salary.

AFAIK, less than 5% of people at those companies (in CH) might earn that kind of TC when looking at value at grant comp (if you count the stock appreciation, but that’s just luck, you can play the single stock game for that, some are lucky and some aren’t).

I wouldn’t be surprised if the top 5% at financial companies and other large swiss companies (pharma, etc.) is similar.

We only have the tiniest of tiny influence on this but:

as investors, if we want to become activists, we can shun the stocks and bonds of the companies offering such compensations.

as customers, we can consume less of the software and items they produce.

as employees, employers or freelancers, we can lobby for better prices for the products of our own labor and for better salaries accross our industry, and specifically ours.

as citizens, we can engage in politics and support initiatives that help our views (as well as vote for them, the later being for citizens only, the former being available to non-citizens also).

Getting such jobs require hard work, skill and also a bit of luck, certainly.

especially in the USA you need to come from a good college. Only wealthy families can afford to send their kids there. So its a closed circle.

I agree inequality is a huge problem. Not necessarily because because i want all people to jave the same, but more in terms of equal chances in life.

If your parents are wealthy, its much easier to buy assets, have passive income, accumulate more assets, have more passive income, and so on…

Leading to concentration of wealth in the hands of few, while average Joes cannot afford a house.

Solutions?

Change monetary policy from highly inflationary to stable, maybe even slightly deflationary.

Taxation on high wealth, especially on real estate could be easily achieved without need for international coordination

This article (in French) gives some numbers from 2022 showing what’s required to earn to belong to the top 5% earners in CH. Qui appartient au Top 5% des revenus? | Allnews . In ZH for instance the threshold is around 200k. You will always find someone earning more than you and that for different reasons, some of which you might deem unfair. However putting things into perspective will most certainly help you understand that we are already part of the lucky ones, being Swiss citizens / residents and that regardless of our salaries ^^.

For reference, the source of that article is IWP where there is an interactive map with some more information. The income figures are based on taxable income.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.