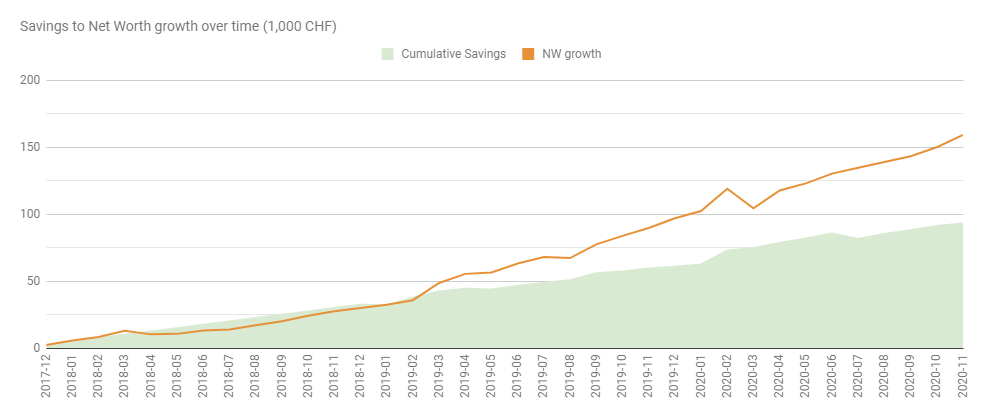

I wanted to explore more directly the impact of being invested vs. just cash savings. (a bit inspired too by @Cortana’s saved vs. actual NW)

So I came up with another view - cumulative savings vs. NW delta - which paints a stark contrast in 2018 vs. after.

P.S. IMO comparing our own NW growth rates to others’ is a bit pointless, as we all have various incomes, life conditions, savings rates and ultimately asset allocations.

(I was a bit amazed by some people’s progressions )

But it serves as a great inspiration to see those numbers rising!

P.P.S. Perhaps savings-to-NW-growth ratio would be a good indicator of how effective one’s portfolio is (at bringing one closer to goals). But then there’s also the risk story and others aspects…

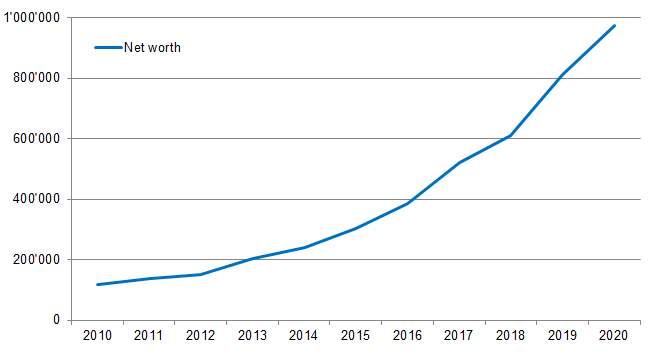

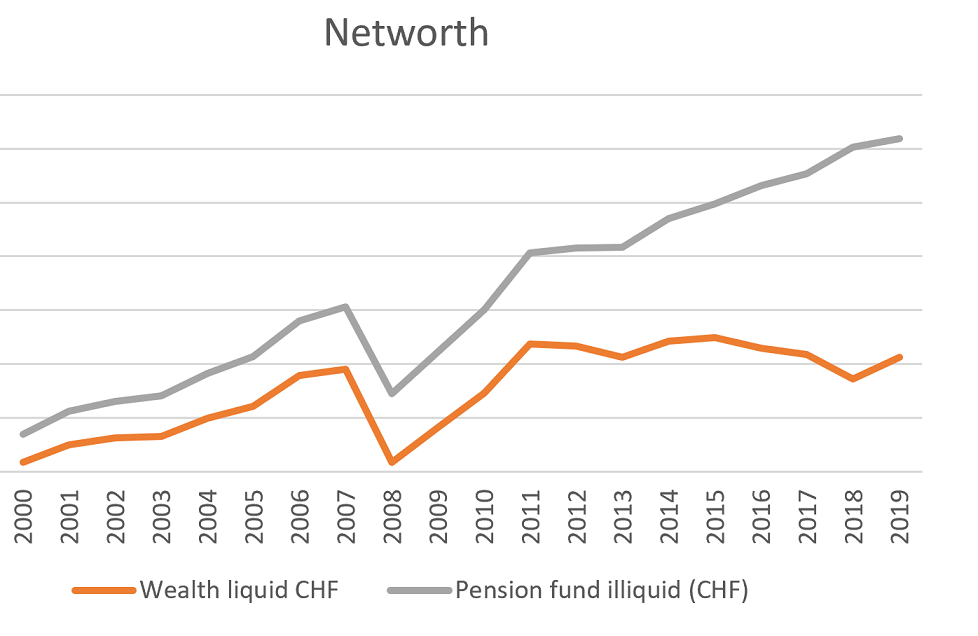

I’ve been at it for a while - at least the tracking part. I only started to become aware of the FIRE world after 2007, when a divorce “happened”. With a very small remaining part of my salary I tried to get by, as my wife was unemployed and we both had decided that she would not go to the RAV and instead focus on her next career step while sustaining her with our savings.

Soon thereafter we settled our (amicable) divorce with a one-time payment for my son that would cover his expenses living under her roof until 2018. I was paid out from the 2 houses we owned at that point and also received a sizeable gift from my parents that helped me get back on track. So V-shaped recovery does exist in real life

In 2016 I started to buy into my pension plan which reduced my liquidity and helped me save taxes. My savings rate was >50% while living in Switzerland. In 2018 I quit well-paid work while having to pay for my son again (who turned 18), then after 4 months found new work in a new country (Luxembourg) which is paying less but still allows me to save a bit (~25%)

To be fair, that development also reflects the significant increase in my savings rate as my career progressed. In general, I believe focusing on your income is much more important than optimizing your investment returns.

As far as my current portfolio goes (roughly, I don’t have a fixed investment strategy and adopt comparatively frequently):

65% equities

20% in VWRL

20% in other ETFs (focus on high cash generation, which makes me pick dividend ETFs)

25% in share picks (tends towards value investing with only some growth titles)

15% liquidity

10% other asset classes (HY bonds, RE and PE via ETFs; no commodities, no crypto)

10% locked assets (mostly second pillar; not included in return calculation)

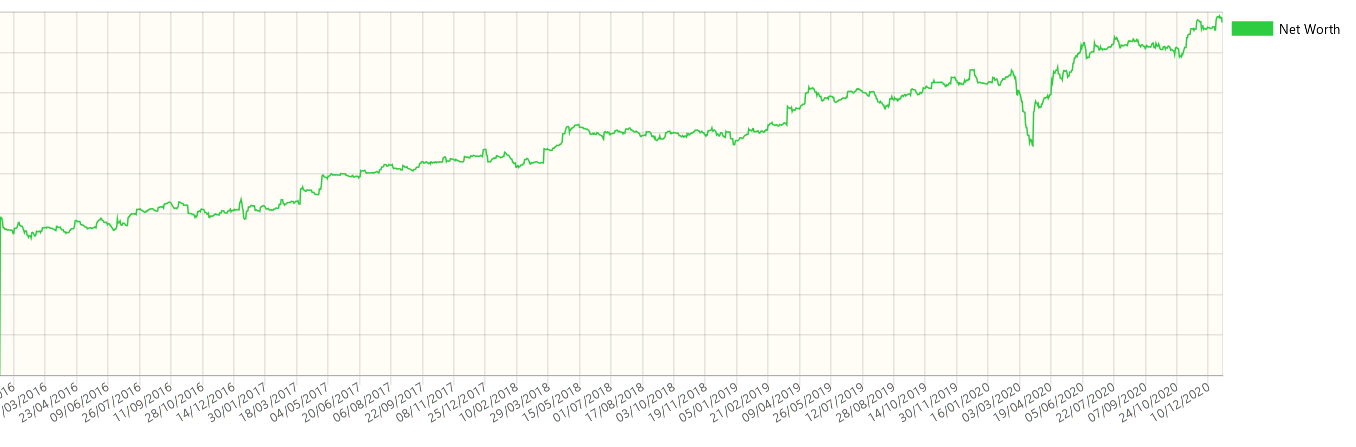

The liquidity and share picks is where I generate my over performance to the market. Share picks obviously requires a bit of work to analyse, but so far has worked out fine. These are the shares I invest in long-term. Short-term, I use the liquidity to capture market opportunities (I often buy on news, especially bad news). I sell naked (cash covered) puts and to lesser extend covered calls to optimize returns. Also, I sometimes buy calls on hyped shares to ride the momentum and sometimes use a lombard loan to buy on bad news (mostly when in HY bonds due to their institutional sizing). This year, the long awaited crisis came (though unexpected in cause), and I temporarily used a lombard loan to buy the dip (I invest on-top of my usual monthly rate per each 6% drop of the market, no matter the cause or stage of the crisis).

In summary: I had a lot of luck. Given that I made quite a bit of money from timing the market over the years, and considering that my portfolio effectively has a dividend and value focus, I would not suggest to replicate it.

In summary in figures: ca. 11%/p.a. return in that shown 11 year period (including 2020 estimate, not yet calculated), compared to I believe roughly 7%/p.a. of VT in that same timeframe. EDIT: VT including dividends is closer to 10% for that timeframe too. So summary of summary: Buy VWRL / VT and focus on your income

Thank you for sharing, quite an interesting (and happy to hear a successful one for you) approach.

I am too lazy and too unknowledgable for such a strategy (at the moment at least).

10-year p.a. of VT is 9.62% (not sure if that includes dividends - if so, it might arrive closer to your 7% p.a. number; or if that 11th year made such a difference)

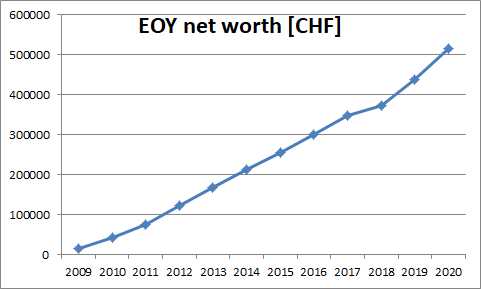

It’s Dec 31st, so that time of the year again. I’ll update my yearly spending thread in the following days, but here I just wanted to share with you guys that I’m far away from exponential growth:

You are lucky between 2010 to 2020 really nice years with some drops but I gain after too. I’m happy for you but be careful about next years for keep this value.

Unfortunately I really meant years! 1 or 2 depending on how you measure it. But it recovered pretty quickly and even if it hadn’t, that would’ve been “just” 2 years but still better off than not having saved at all. So despite what it may seem, these are positive and optimistic posts

Ah you meant the drop (bottoming out) itself set you back to the point 2 years ago?

I was looking at it from an angle of how the whole event “slowed down” your progression, i.e. how long it took you to catch back up again (from one to the other side of that V).

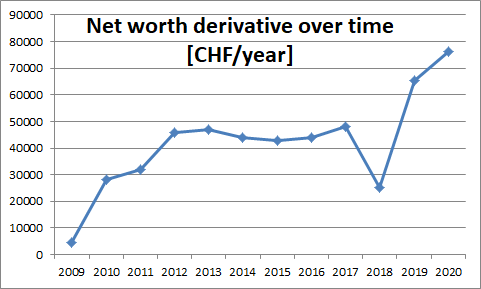

As you can see the derivative was growing fast in the first years as I went from internships to real jobs and got a substantial salary increase for few years in a row.

Then it flattens out between 2012 and 2017 (same job, basically no investment).

I started investing very gradually in 2018, that year’s result is affected by the market performance but also by a lump sum payment/gift to my parents.

I’m not even close to some exponential growths I’ve seen posted above, but still pretty happy with the direction it took in the last 2 years…thanks to these crazy markets

Nice gains and an even nicer watch! Your savings rate is through the roof and I think you’ve earned a bit of luxury. Coming from someone who ust spent 600+ to service one of my watches and I still should send one for repair.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

glad you’re on the right path!

glad you’re on the right path!