@TeaGhost @xmj FYI I moved that entire discussion to a separate thread, as it was off-topic. And as part of damage control, I closed it. The forum rules say discussion on policy is allowed, but on politics not. To me that distinction isn’t all that clear. In any case, I think it’s best to avoid igniting topics, eg. how we need more vs less regulation.

2 Likes

In my model, I assumed 4.5% general inflation and 7.6% inflation on health insurance costs in my current model. Not sure if that might be too conservative?

I assume 5% nominal return (so 0.5% real) with 100% income for the next year and phasing down to 40% income 60% CG over 3 years as my bond portfolio gets absorbed.

Where is the disciplinary action on the Personal attack? Please at least delete his posts… al least.

1 Like

The posts have been moved to a separate thread and unlisted. Nobody will see them unless they explicitly look for them. I hope that’s ok for you.

2 Likes

Thats great, the unlisting does the trick. You may just delete m request above and response now. All good, thanks.

Your approach seems prudent, but consider diversifying your assumptions for a more robust model. Exploring various inflation scenarios and investment strategies could enhance accuracy and resilience check how famous people manage their fortune.

Can we cleanup dumb discussions from this overview thread? I just scrolled for 20 seconds to find a „net worth progression“

4 Likes

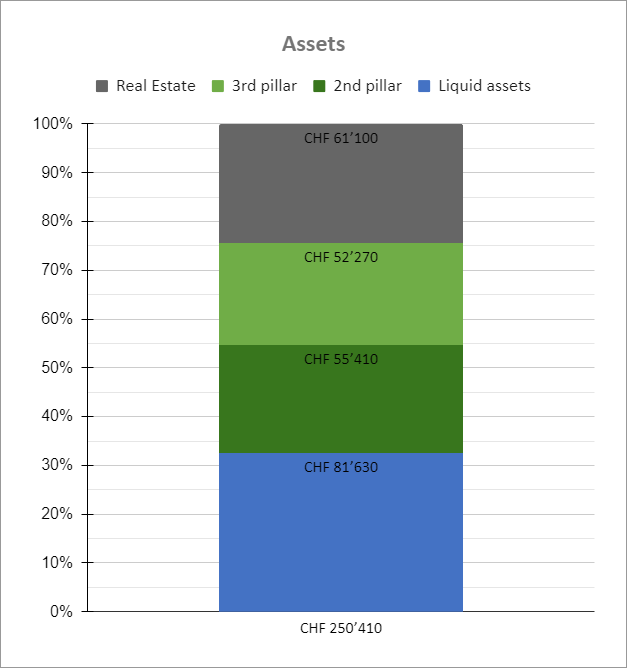

I finished 2023 with a networth of 215k. Reached the 250k milestone way sooner than expected (crossed it today the first time).

8 Likes

Bravo! ![]()

Assuming 5% on everything except the second pillar, you locked in 10k of investment net worth gain per year.

How long did it take you? What time frame are you projecting for the second one?

![]()

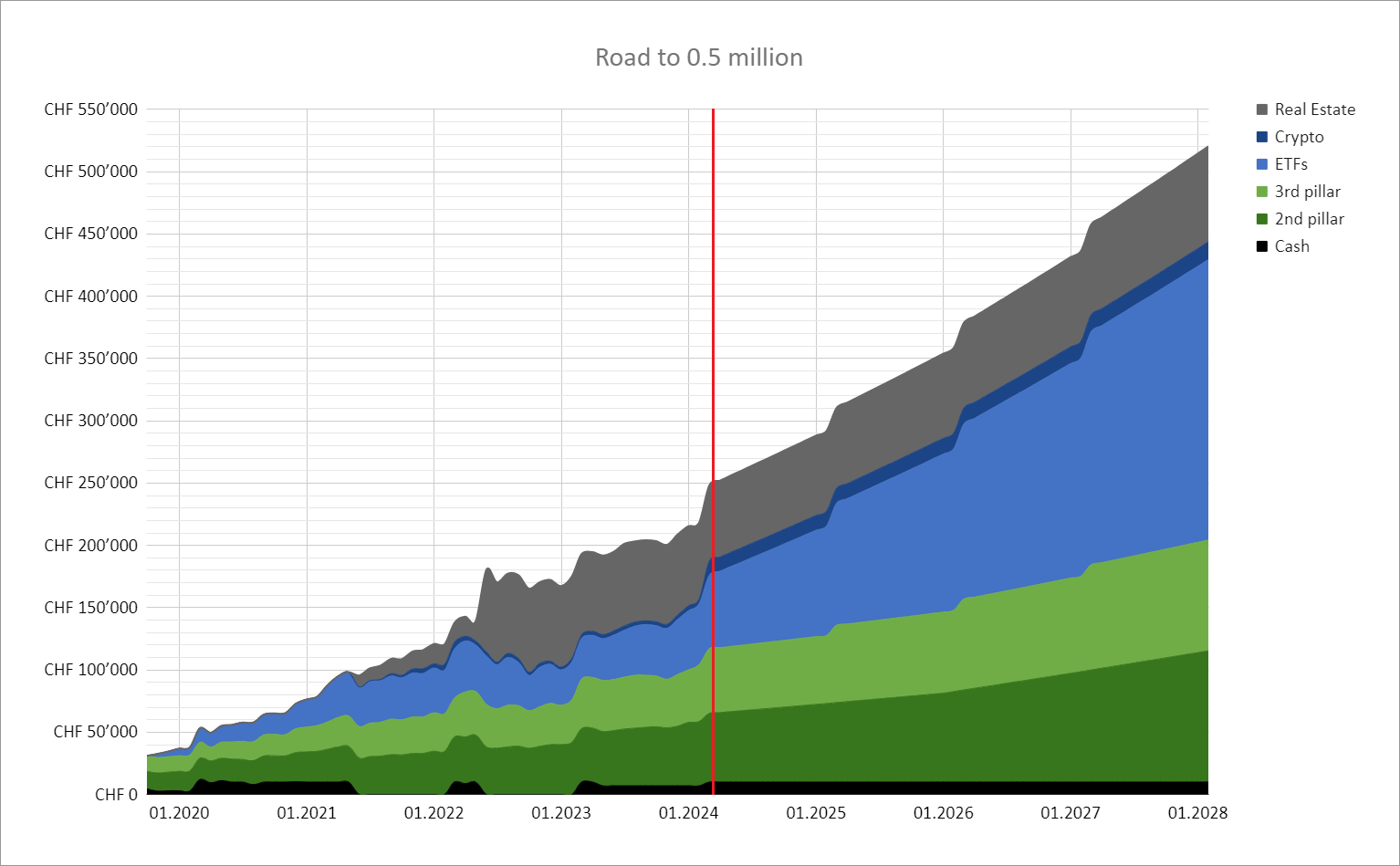

![]()

![]()

1 Like

I started investing 4.5 years ago when I was 28 years old (I wish I started sooner). Had 4k cash, 12k 3nd pillar and 14k 2rd pillar.

I’ll probably hit 500k in autumn 2027, so in around 3.5 years.

5 Likes

Where Bitcoin? ![]()

(here’s 20)

Which program you use to do this prediction ? ![]()

It’s Google Sheets ![]()

Estimating salary growth of 2k/year, 6% return on investments, an increasing savingsrate (basically the higher salary minus taxes) and other factors like interest on 2nd pillar, increase of employer contributions with age (next increase at 35 in 2 years) and some minor growth on real estate.

2 Likes

From personal experience I can’t recommend highly enough that everyone should have such a spreadsheet!

If you key in your your asset allocation, salary and approximate spending you can forecast your Net Worth and Financial Independence date with a high degree of probability.

Over the long term the expected return from asset classes is predictable.

Once you have the model you can understand the impact of changing the variables and decide your strategy:

- big purchase decisions (car or house)

- asset allocation (cash vs 2 Pillar vs stocks)

- where to focus your energy (getting salary increase, decreasing spending, stock picking, etc)

9 Likes

600k-ish ![]() (and some chars)

(and some chars)

4 Likes

And it‘s very motivating to see the numbers and graphs. 500k seemed so far away when I started my FIRE journey, now it‘s probably only 3-3.5 years away (if there is no massive crash). Then I‘ll be probably already be looking at when I‘ll reach 1M.

1 Like

I guess a few factors are at work:

- As your salary increases, you get a kind of operating leverage as most of your new salary should go to investments so long as you keep lifestyle inflation under control; combined with

- The exponential nature of compounding means it seems flat until it suddenly hockey-sticks

1 Like

Not there yet. Here is a half time (~2.5 years) update:

Equity: ~ 750k

Pillar 2: ~ 200k

Total wealth ~ 1m

18 Likes

What helps me with that is a simple Spent/Income/Saved overview, and at the end of every year I have a target for Saved for next year. I even include the amount of tax I will be spending, which I then update in March once I have filled out tax for last year, I estimate the amount for current year, and it’s always been very accurate so far.

As the year progresses I keep checking if I am on Plan and I will adjust my behaviour to make sure I reach Plan. This year the target is 5k higher than last year and so far I am doing well against Plan.

Of course I could be happy with saving the same as last year and enjoying spending 5k more, but I take a perverse pleasure is saving and reaching my target. And there will always be years where I will want to spend, a new bike comes to mind, but more importantly, at some point the compounding really takes over and you want to get there faster. Keeping this in mind helps to keep spending low.

3 Likes

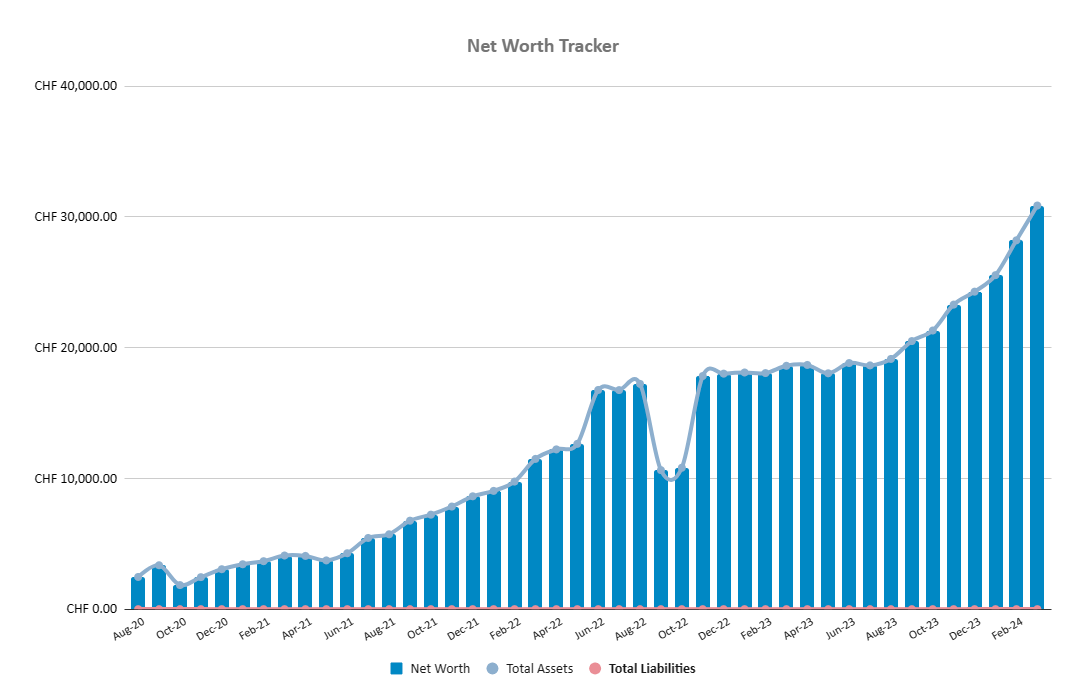

Just reached a further ten thousand !

I’m very happy with the progress. That may not sound like much to some of you, but at 19 years old, it already represents almost 75% of the total salary I’ve received since the start of my apprenticeship in 2020 (CHF 41’200.00).

Thanks to the market → 90% of my total net worth is invested in stock market and I got a return of ~20% since inception.

I spend a lot of money on my hobbies, which give me a lot of pleasure, and that figure is only going up! Sounds good for the future

24 Likes