Impressive numbers/ growth.

Can i ask you how old you are?

Also it seems like the growth come from RE, is that right?

If you plan to have some they sure as hell cause a loss of earning and some additional spending…

Impressive numbers/ growth.

Can i ask you how old you are?

Also it seems like the growth come from RE, is that right?

If you plan to have some they sure as hell cause a loss of earning and some additional spending…

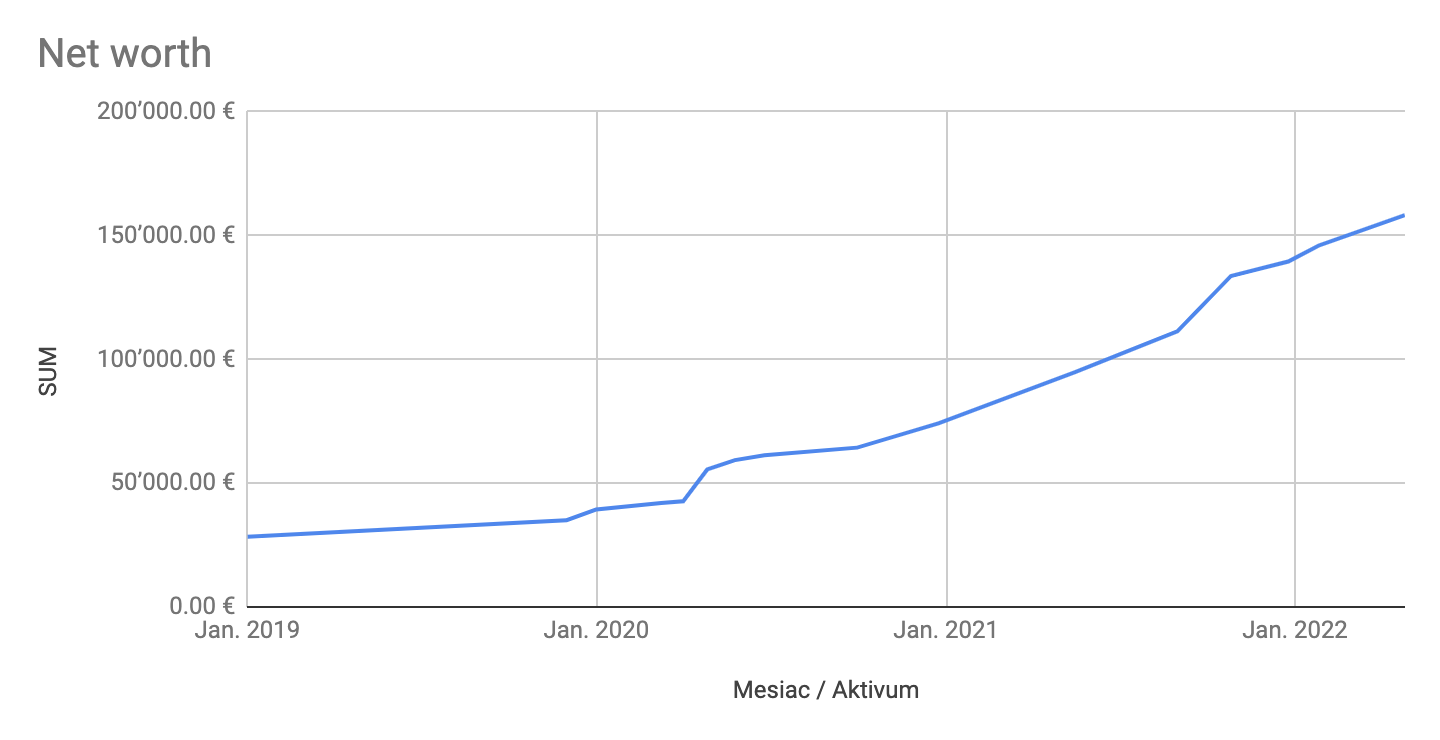

I’m 31 and she is 26. Well before May 2022 everything came from savings, investments and pension fund contributions. Then she got this gift and we bought an apartment. So the sudden increase in May is due to that.

I hope that my salary progression will compensate for the additional spending with kids. With 1 kid we would probably keep working full time and use Kita. With 2 kids she’ll likely reduce working drastically or stop alltogether.

How is Grundstückgewinnsteuer calculated?

(Selling price - your buying price) * tax-rate

In AG it’s 40% in the first year, 38% in the 2nd year…20% after 10 years and then -1%/year down to a minimum of 5% after 25 years. Other cantons are similiar.

If you buy something else within 2 years after you sold, the tax office will waive the Grundstückgewinnsteuer and the years of holding RE will keep going. So buying A and selling it after 10 years, then buying B and selling it after 15 years without buying something else will lead to the minimum tax-rate of 5% in AG.

It also depends if the new property is below, at or above the selling price of your old property. Let’s assume you bought a house for 600k and sell it for 800k after 10 years.

In reality RE prices increase over time and you’ll probably going to buy something new for a higher price. If you never return to renting an apartment, you’ll probably never pay the Grundstückgewinnsteuer.

So my net value calculation is assuming that we are selling the apartment for the current market value without buying something new (which won’t be the case). So I’m more defensive here.

I love how much into detail some people go in tracking their net growth. A huge inspiration for me.

I am currently 26yo and most of my income comes from my full-time job. I have been frugal my entire life. I’d love to hear your advice or any resource on what to do next. I wanted to buy a property but with the current market being so unstable I am honestly very confused. Anyone who’s gone through this journey - please get in touch.

I think you are doing just fine. Your target now is consistency, to continue what you began for years to come. I would not recommend a real estate deal in these uncertain markets and this early in your accumulation phase.

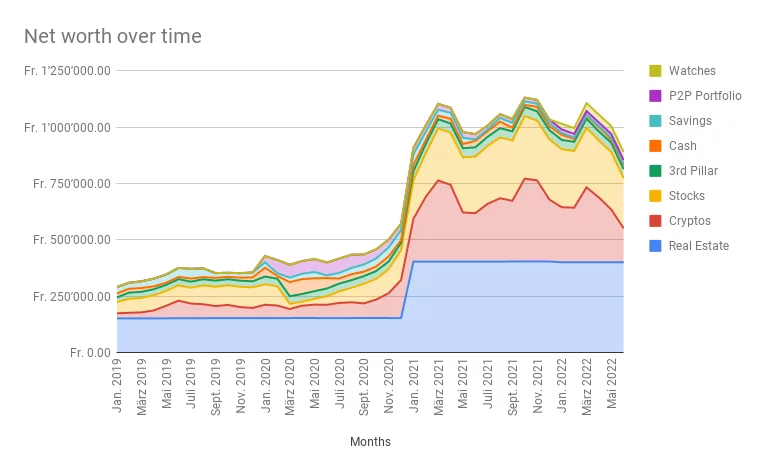

How does it look if you leave out the crypto piece? ![]()

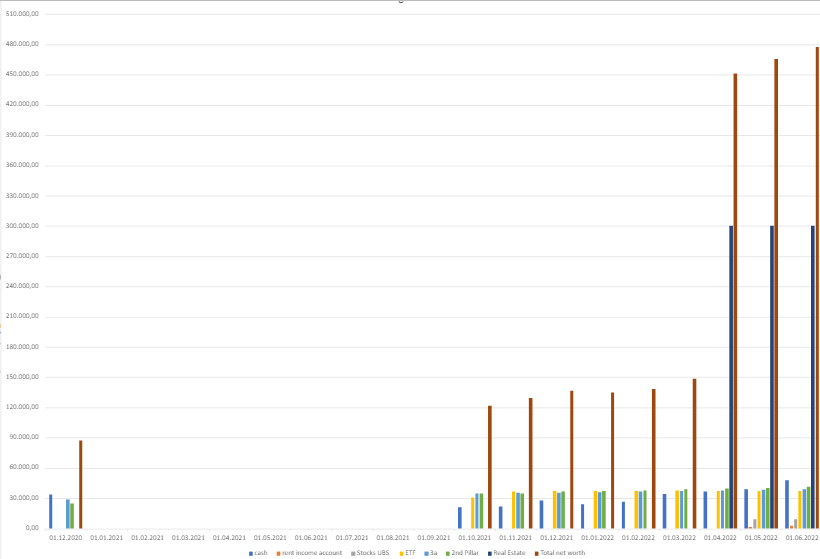

How did you produce these awesome charts?

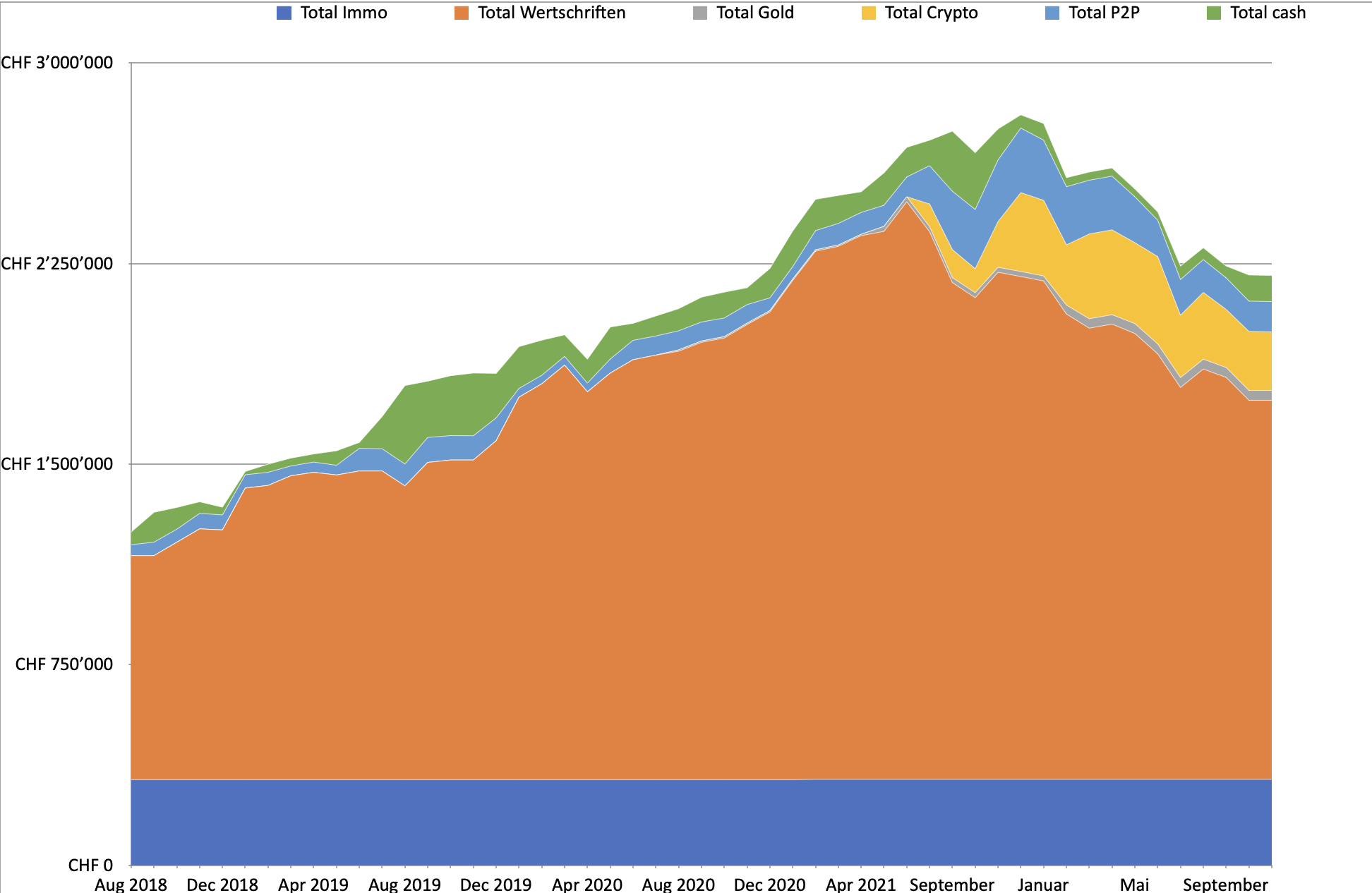

Update: On my side nothing has changed - I saved up 50k during that year and my portfolio melted by 50k. So I’m net zero.

So you are getting to buy cheaper ![]()

Just Google Sheets ![]()

Can share a template link later ![]()

Here it is, let me know if you have trouble accessing it:

Fields you add numbers to are with colored headers (i.e. your investment vehicles & savings), the rest is calculated.

Hi everybody

First of all, I am sorry for my english ![]()

I’m a 31yo Dipl. Treuhandexperte working Zug. Gross salary is 140k/year + bonuses.

I started to analyse my net worth by end of last year. I always had huge expenses for hobbies (golf, tennis and a big boat), cars and vacation. So I decided to start a more frugal lifestyle by 2022.

By end of 2020 I had a net worth around 90k. By 01.06.22 I had a net worth around 465k.

A huge increase was due to an inheritance in April 2022. My sister and I have now a old house with 3 flates which were rented (3’300/month). Currently we are planning to tear off the old house and build a new investment property with 10 flats. I am a bit scared cause the current interst situation but looking forward to start the new project. I am in general very intersted in real estate.

I planned go FIRE by 50 and enjoy life in Ticino with rental income and dividends.

Thank you

All depends how much your withdrawal rate with 2.4MCHF is.

Maybe just cut down some big ticket luxury stuff which would not hurt (travel less far, postpone a big ticket purchase…).

@moderators : if this gets into a bigger discussion, it might be worth an own thread.

I guess the FI number depends on your calculated withdrawn rate. However, of course there is never a guarantee that your money would cover all your expenses until end of your life.

Furthermore, the near term future will be very interesting as the hole FIRE became big and popular in a time with soring share prices, almost 0% inflation, etc. we all knew that these were exceptional times but as it was rather a long bull run it became the norm. Now it will be interesting to see how people react under these different circumstances.

If you opted out from your old job and felt happy about that I would not go back. However, it may help you to be more relaxed to have some income in these times just to sleep better.

Sequence of returns in the first few years after retiring is the killer element that can hit you, even if you adhere to all conventional assumption like a reasonable SWR.

So yes, you may want to consider saving and reducing withdrawals in these years (e.g. postpone expensive travels typically planned after RE) or picking up a side income to stay on track. On the other hand, it looks like you peaked at nearly 15% above your taget number, and aren’t too far below it yet (though that also wasn’t an actual crash so far), so certainly no need for too much concern.

I think this is a very important aspect. Many, myself included, have no idea what an actual crisis feels like, especially not a prolonged one with many dire years. If the reactions seen in such forums to comparatively minor events are an indication, many will eventually panic sell and loose their FIRE possibility in the process. If that sell-off were to begin, it would also be a self-fulfilling prophecy, and retail investors (esp. in the US) could create a crash not seen in a very long time.

Fully agree and I’m also in the same situation not having experienced a major bear market with considerable own money invested. I already though of getting out of the market and back in or buy some puts or short mini-futures. I let you know once I do that as this a usually a good indication that the market turns ![]() .

.

Honestly, now I still feel good but already my company share portfolio which is restricted has seen a considerable down which would impact my dream of a sabbatical leave with my entire family in 2024.