Can you please elaborate in which crypto did you invest into and you‘ve had a crazy year because generally speaking crypto market didn’t have a so crazy year… or ofcourse you should have picked only the right coins…

Yes, that is true. But I am not counting on it: 2nd pillar I should be able to withdraw in the next <10 years when I move out (if I do, otherwise I’ll pay down the mortgage with it), while the AHV is some >25 years away… a bit far to even think about.

Quarterly update. Despite too much exposure on the market, debts clearing and a big downpayment from a project for later this year, the pace is still OK I guess. New income will start to kick in for the second semester will help.

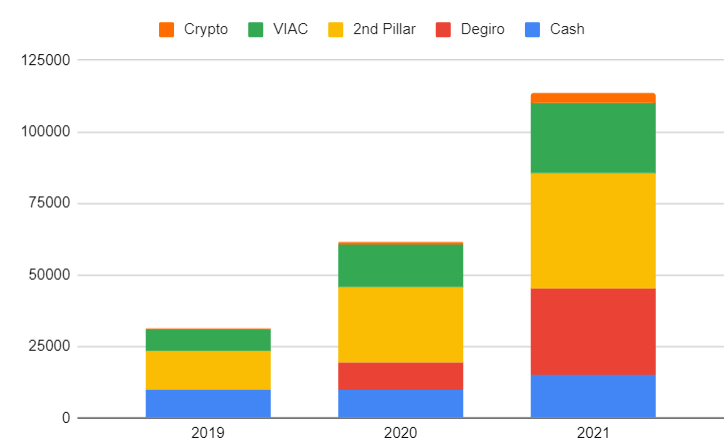

Vested benefit account only, VIAC+Finpension, yes. I made stupid choices some years ago and basically blew my 2nd pillar at that time. So now (because different job changes) I have all I recovered since in a vested benefit account. I will track next year the addition to what I’m adding with my current employer.

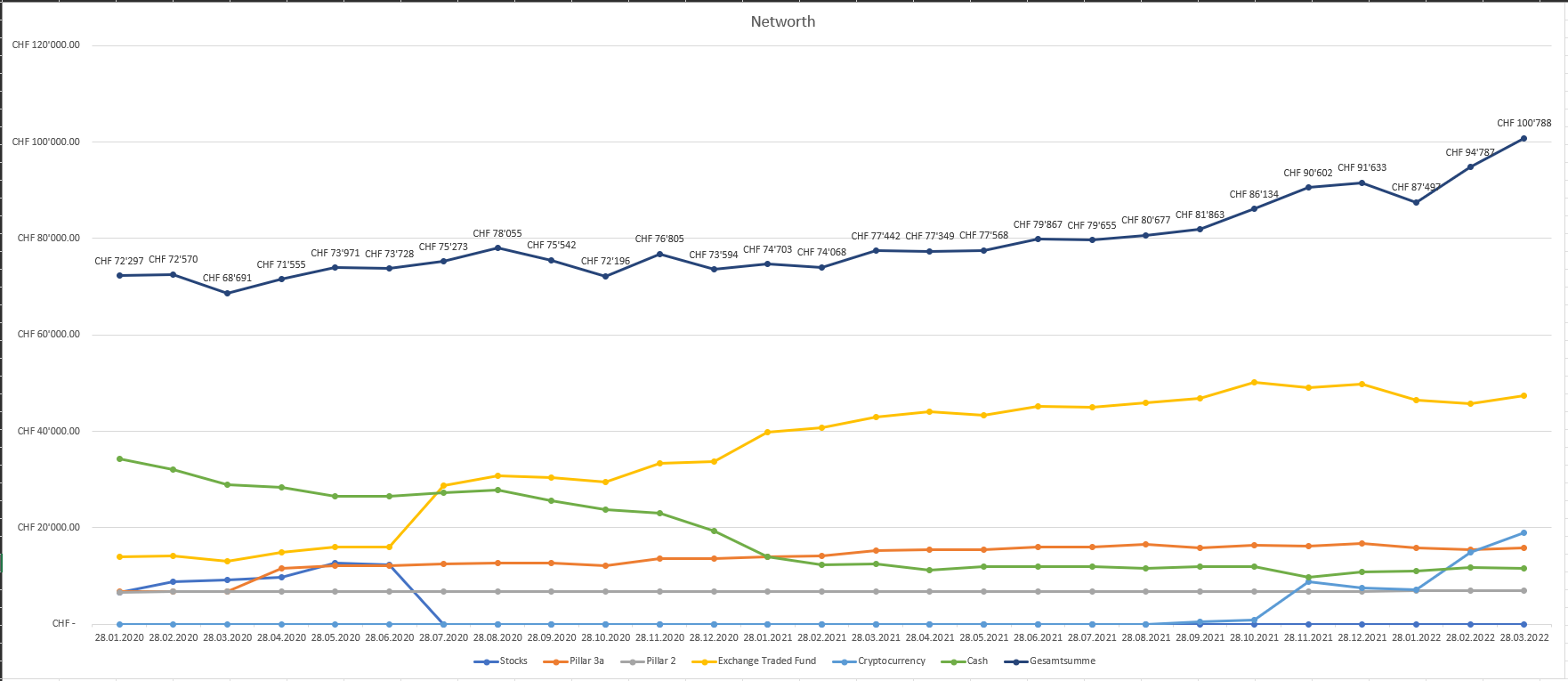

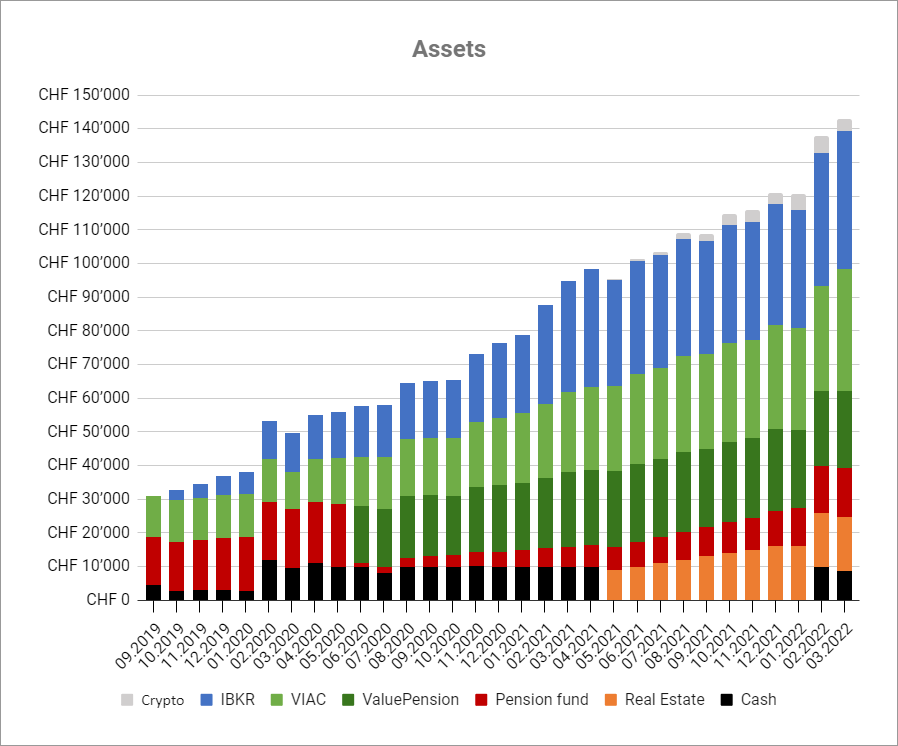

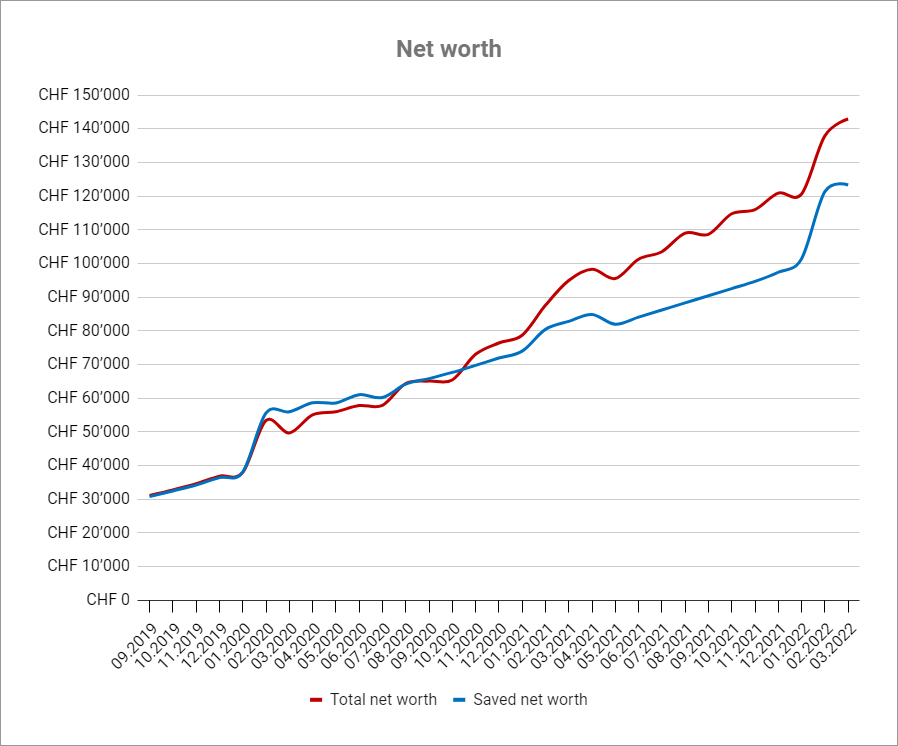

Updating it every quarter, now with March figures. Very interesting to see other charts kicking off once you reach the 100k.

Footnotes:

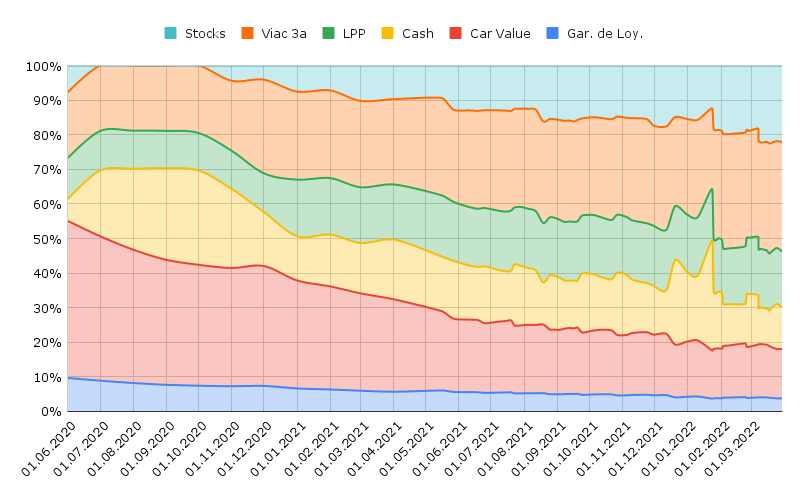

Light orange is amortized debt for rental properties in Germany as well equity down payments if any. Taking market value (vs. initial debt volume of €2.5m) into consideration numbers are likely higher but prefer to be conservative

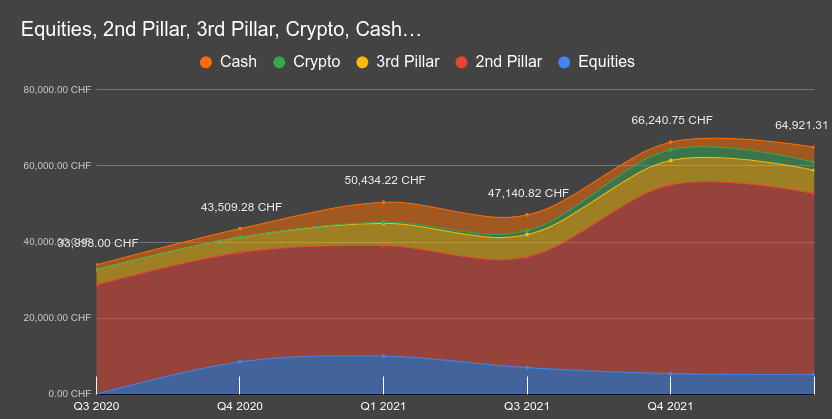

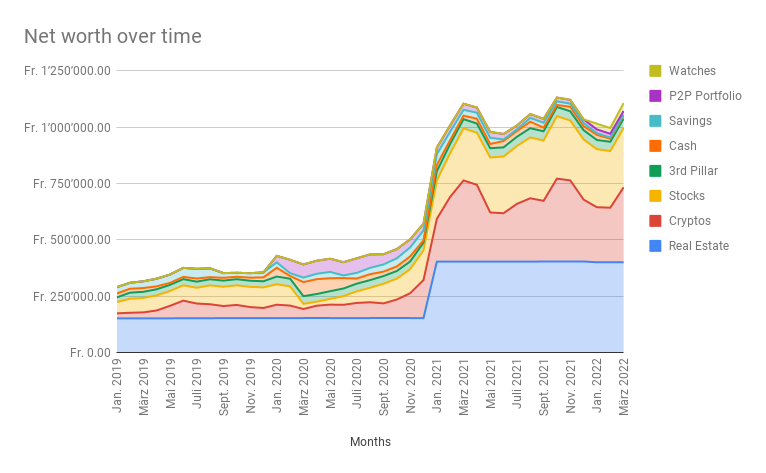

Sharp increase in 2021 is due to two facts: i) crypto increase from 30k to 200k in Q2 ii) in Q3 I put any money I could grab (500k) into my employers company to participate in a Series C funding round which paid off end of year with +50% performance so far

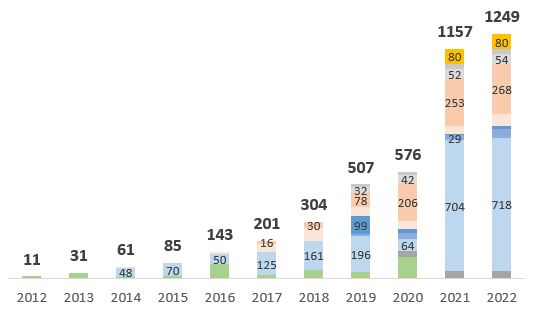

Progess of the last 30 months. Will probably hit 200k in summer 2023 and 300k in summer 2025. Maybe also way sooner because I’ll be able to save more once we bought the apartment.

As I have access to evaluation tools with the biggest database in Switzerland (Wüest & Partner) I could potentially make new evaluation every month. Then subtract the current mortgage of it and get the new value.

The issue is: We paid 110k less than the current market value (880k). I see 2 options:

Track it as it is and increase my net worth directly by the current gain.

Set the buying price as the base (770k) and change it relative (%) to the further increase. So if it goes from 880k to 920k (+4.55%), then increase the value from 770k to 805k.

Personally, I only consider liquid assets (cash, investments, 3a, crypto, etc), and leave out anything that has a “negotiations” value (car, watches, real estate, etc).

If I were to take into account the value of my real estate, I would calculate:

Value at appraisal (at the conclusion of the mortgage) - Mortgage = current value.

However, I would re-evaluate the value of the property every year according to the appreciation/depreciation. I don’t see the need to keep the value of a property up to date, I can live with an annual revaluation (my opinion).

In your case, I will take into account the market value.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.