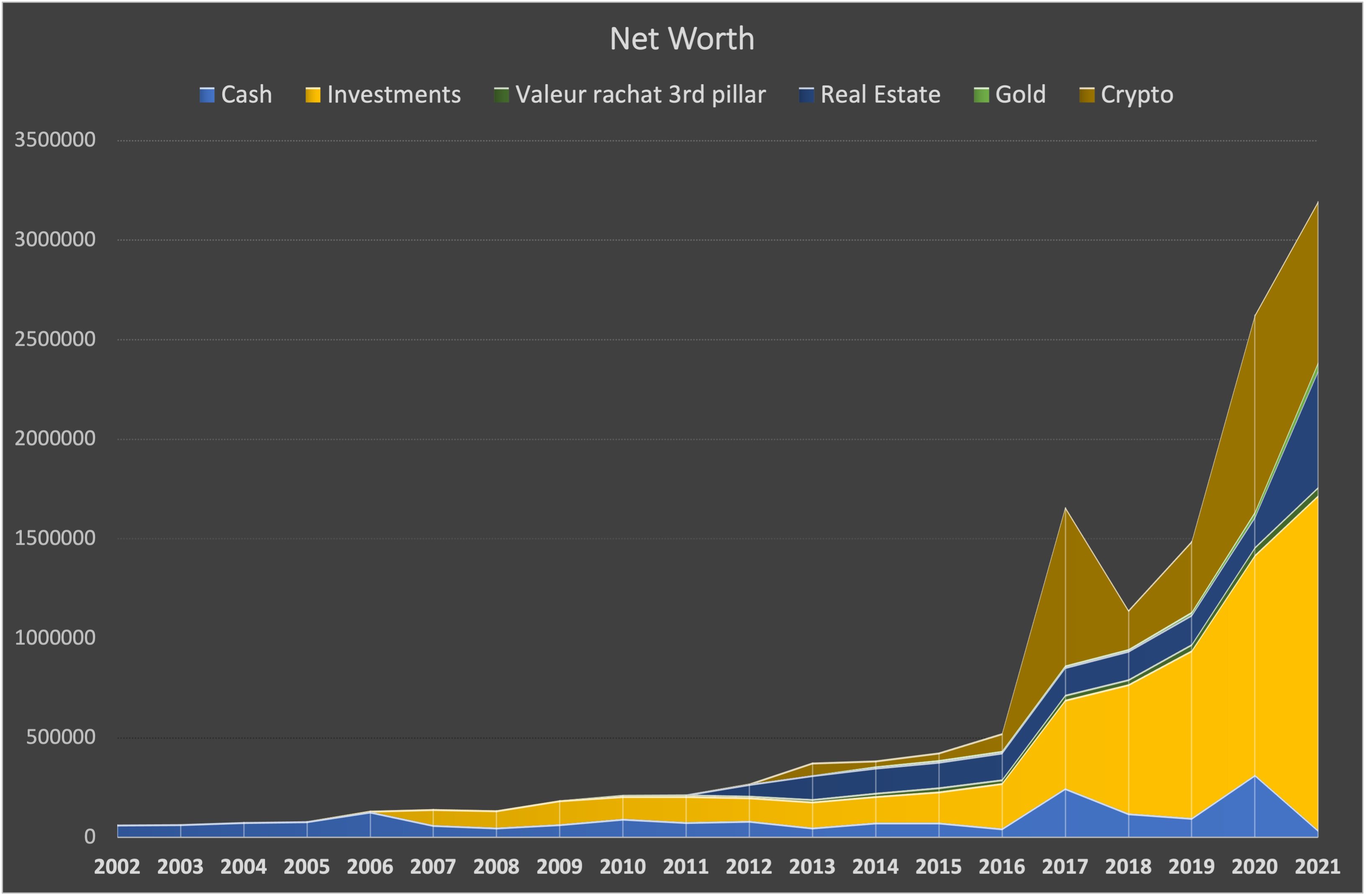

I continued selling my cryptos according to the plan + I capped it to 1 million max. I bought a house and started renting out the other apartment. The increase is mostly due to crypto gains and market gains. What a year !

I have a private pension fund, no 2nd pillar, which only gives a pension no lump sum. It is therefore not represented here.

My FI number is between 2.5 and 3 millions but I have always excluded crypto from this number.

Even then, it’s still a value greater than 0 and an income stream one can, with relative certainty, rely on at retirement age, in practice allowing to use a higher withdrawal rate in early retirement years.

Personnaly I don’t count it in because I do not have control over it.

So for me it will come as a bonus once going to become independent or leave Switzerland, but until then no point of tracking it since I do can’t make any decisions about it.

It is guaranteed that you can get it paid out as a lump sum today. Just quit your job and transfer it away from your employer’s pension fund…

The conversion rate only becomes relevant if you stay long enough with your employer.

Pension capital should be considered part of a person’s net worth, regardless if it’s in a pension fund, a vested benefits account or third pillar money. Transfers to those are not “lost money” in that sense.

Circuit breakers (for US stocks) and after hours/pre-market trading may make it overly difficult, if not impossible, to sell your assets during a market flash crash. Also, brokers could pull a reverse-Robinhood and prohibit selling while potentially still allowing buying…

But of course, another likely outcome is that the leftist government who steals by taxing decides that property is theft and assets belong to the People, seizing financial assets overnight without warning and without giving you any say in it. Who knows? They could even do it to save AHV and 2nd pillar pensions instead of reducing the conversion rate!

Stocks have risks, and stock markets can, and have, go(ne) to zero.

Even if you leave the country, you will still get paid AHV according to your contributions. I agree it’s hard to account for and I don’t. I occasionally check my AHV estimate and it’s actually not insignificant, considering that my wife is at home and me paying my AHV dues also buys her some AHV in the future.

Exactly. A rule of thumb is, currently you would recieve about 54 CHF Monthly, per year of contribution. So if you are here 10 years, you would get about 540 CHF per month.

Well, if we want to be nitpicky one should account for the present value of the annuity taking into account life expectancy. Or, as a very rough shortcut, use the 2nd pillar conversion rate as a proxy but this is polluted by your 2nd pillar particular case.

I count 92% of my 2P transfer value - after 8% cantonal withdrawal tax. There is low probability that CH authorities will decide to expropriate it and such a change needs to be voted and would happen slowly. We are not like Argentina or Hungary, yet.

You misunderstood me. I’m talking about transferring your money away from the employers pension fund. Not transferring money into it.

When you leave a company then you can transfer all of your money to a vested benefits account (or two). That is guaranteed.

What happens afterwards is a different topic. Early retirement for example. And the conversion rate has become irrelevant because your money is not in a pension fund.

OK but if you retire early (which is the goal for most of the people here I guess) then the money would in any case go to a vested benefit account where you can invest it according to your preferences, no ? Obviously the time this money remains invested in the VB account and has the possibility to (hopefully) grow according to your preferred strategy makes the difference

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.