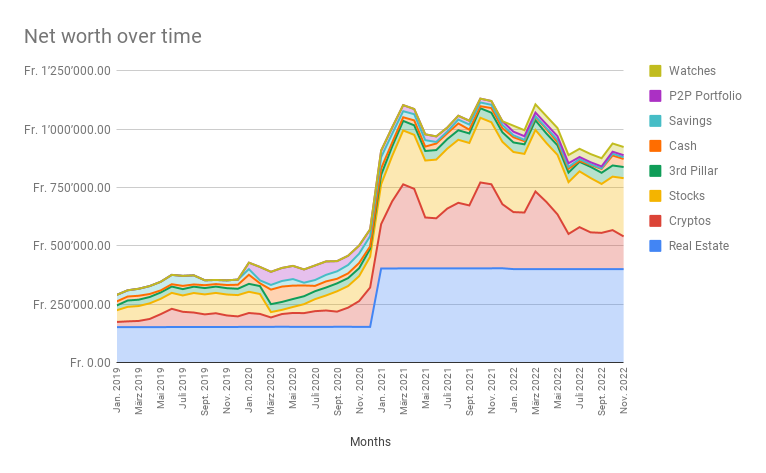

Still hovering around the 1M CHF mark, I hope these bear markets end soon, at least the income got a nice boost since September.

Read all about it here:

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.