Hello, I’m new to this forum and would appreciate your insights on some investments I made in 2024.

Background:

- I’m not well-versed in investments and am behind on my retirement planning, which led me to seek solutions.

- I hired a tax advisor for my tax declaration in German language. After completing it, the advisor suggested retirement plans since I had significant cash available and I was willing to put an effort.

Investments Made, following work with the Advisor:

- Opened a Pillar 3b with classical and “fund-unit-linked life insurance” for both my wife and me.

- Transferred my existing Pillar 3a to the same plan.

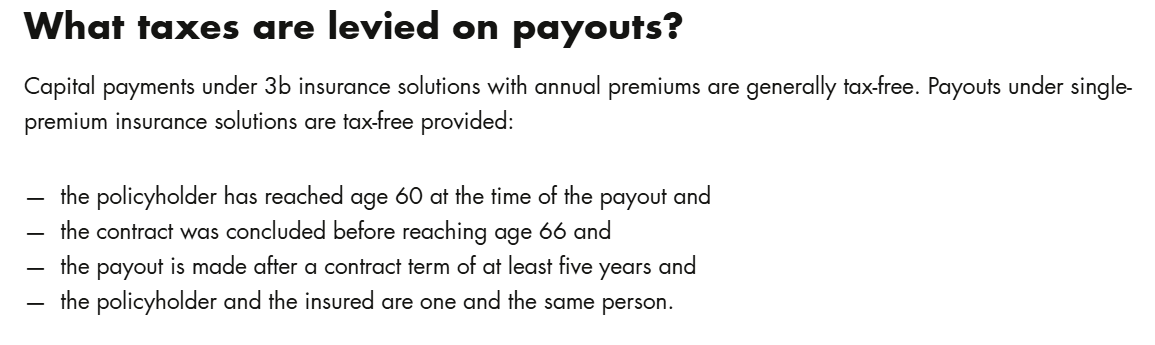

- The advisor mentioned that after 10 years, the money in Pillar 3b would not be taxable, which seems advantageous.

- During the process, the advisor requested that I provide medical checkups because the insurance company needed to assess their risk. At that stage, I was so uninformed that I found myself asking, ‘Why is that? What risks are they referring to?’ I’m not suggesting that the advisor hid the nature of the contract; rather, I was so unaware that I did not understand it well.

Both Pillar 3a and 3b contracts started in early 2024 for 15 years:

- Pillar 3a contributions: CHF 7K each per year (for both my wife and me).

- Pillar 3b contribution: approximately ~CHF X0000 per year for both my wife and myself.

Current Situation:

After one year, my Pillar 3b balance shows a total 15% lower than what I invested.

=> The “savings Total balance on 08.01.2025 before deductions upon surrender"

Concerns:

- I feel both plans lack diversity, we are “putting all our eggs in one basket”

- As I have no dependents, I’m questioning if life insurance products are the best fit for me.

- A “loss” of 15% invested seems significant for 2024 only (is the remaing used as Premium fees?)

Questions:

- What are your thoughts on my situation?

- What could be my next steps be?

- Trust the system and continue, hoping the loss will be compensated over time?

- Close both plans, accept the losses, and start fresh?

- Keep the plans but reduce my monthly contributions to regain investment capabilities, and to start investing somewhere else to diversify?

Thank you, I would really appreciate your help!

PS: As a side note, the same tax advisory company did not respond to my request for assistance with my 2024 tax declaration, forcing me to extend the deadline with the Canton and hire a new tax advisor in an emergency. This experience gave me the impression that their business model works as follows:

- The Tax Declaration activity allows Tax advisors to assess clients’ investment capabilities (but they don’t make much money from this)

- Acting as brokers to sell life insurance plans is where they generate their real profit.

But I may be wrong.