Well, yes and know. I didn’t want to silence that user, but I also didn’t necessarily believe in the story. It’s not a bad idea to reassess the situation and learn about alternatives, whatever the occasion is.

If you are taking risks, it’s better to do it consciously.

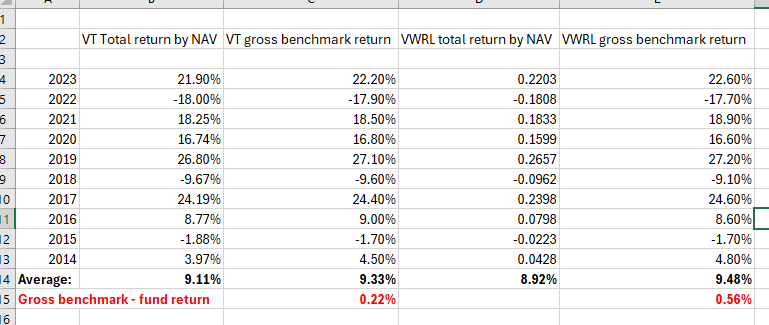

Just made a comparison between VWRL and VT in terms of tracking difference between the fund returns and gross benchmark (before dividend withholding taxes). Over the past 10 years VT did 0,32% per year better than VWRL. Note actual performance of VWRL is slightly better due to different benchmark, it does not invest in small stocks, which lagged large cap in that period.

We pay the “wealth” tax, which is roughly equal to 2% of capital per year. No capital gains tax (may change after 2027)

I think you took mathematical average. Isn’t it? Or was it CAGR? In case you would like to see overall cumulative return , then following are the numbers from the ETF webpages.

Where did you get gross benchmark returns? Because normally returns are measured as Total Return Index.

I believe the post tax calculations done by the experts on the forum are quite good and we should count with realised difference of ~0.2% in final post tax performance between US domicile MSCI ACWI index vs IE domicile MSCI ACWI Index (with TER difference of 0.12% inclusive) . Of course higher dividend yield will have slightly higher differences

It is not insignificant difference but I think for someone who is interested to diversify (partially) away from their US domicile positions then VWRL is best option for now. In couple of years perhaps FWRA or WEBG will also be good once they are established.

I posted arithmetic return (not geometric), so it is not CAGR. But the metric I used is pretty good to compare leakages of withholding taxes. This topic is very well studied in the Dutch investor circles.

The fund providers always compare performance with net return benchmarks. Net return benchmarks give you returns after DWT. The gross benchmarks do not take into account losses of DWT: this is important in the Netherlands, as Dutch domiciled funds can claim it back from the tax authorities. The elephant in the room is that there is no Dutch domiciled fund that does not apply an ESG screen. I avoid ESG funds.

The gross benchmark data for can be obtained here:

Here is IBKR guide on withdrawing in general:

“Because of anti-money laundering regulations, all withdrawals will be sent in the name of the account holder.”

I would not rely on name at all

Here is IBKR guide how to withdraw funds… to a 3rd party!

There are some controls though:

"…submit the third-party payee information to us for approval. You will be notified when we approve the information."

However consider the potential confusion of joint accounts , married vs. maiden names, double barreled names. In UK you can change your name by deed-poll in 3-8 weeks! And if your name is John Smith, Juan Garcia or Wang

I have a question for you, since you seem to be well informed about the topic of Total returns.

I was looking at VWRL reporting in Switzerland. And the documentation say “comparison is based on gross income reinvested” … does this mean that assumption would be that full dividends are assumed to be reinvested (without considering L1TW or L2TW) ?

Thanks for the compliment, but I cannot answer your question with certainty. It is likely that they mean that dividend is reinvested before taxes on dividend in Switzerland if you pay such taxes. Their performance data clearly indicates that they benchmark VWRL to the net index, i.e. after dividend taxes at the source (15% in America, 15% in Japan, 0% in UK, etc), the so-called level-1 tax. Probably they neglect level-1 tax and mean level-2, i.e. the tax that investor pays on distributed dividend by the fund.

As you can see, VWRL follows its benchmark very nicely, within a few bps, since inception there has been 0 difference. How can it be for a fund with a TER of 0,22%? It’s not security lending income, as it just 1-3 bps. The answer is that net index uses maximum tax rates, like 30% in America, while US-Ireland tax treaty lowers it to 15%.

To further illustrate the point, compare net and gross returns of a major index, MSCI World:

The difference in annualized 10 year returns is 0,60%. Awesome!

That’s why for me VT is much more attractive than VWRL, at least I don’t pay taxes on US dividend (US is 60% of the fund), and it looks like US has better tax treates with some countries than Ireland (e.g. Japan-Ireland 15%, while Japan-US 10%).

Thanks.

I also have majority of portfolio in VT.

However I also have some VWRL and I just wanted to be sure that I understand the net impact of this choice.

It seems like tracking error is not a good metric for IE domiciled funds because of this benchmark discrepancy. It’s also misleading for investors if benchmark assumes full tax and ETF assumes treaty rates.

I think the calculations made by Dr Pi in past is the best estimate (adjusted for dividend yields) and can be used as good approximation for impact of VT vs VWRL for Swiss investors

I would not judge that harshly, but yes, you need to understand the benchmark. It complicates things indeed that bencmarks use maximum tariffs, while the fund may use tax treates.

I always compare performance to the gross index and nerdishly read annual reports to see the percentage of withholding tax paid, it’s always in the annual reports.

On May 16, 2024, Interactive Brokers LLC (“IB”) filed a notice of data breach with the Attorney General of Massachusetts after discovering that an unauthorized party was able to gain access to an employee’s email account. In this notice, IB explains that the incident resulted in an unauthorized party being able to access consumers’ sensitive information, which includes their names, Social Security numbers, financial account information and driver’s license numbers.

But it raises more questions. Why was such sensitive information stored in email? How was it possible that email was compromised? They kept the breach unreported for more than 4 months…

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.