I would like to ask your advice on my current challenges.

Background:

40 year old, with wife and one child(5yo), moved 3 years ago to CH.

Living in Aargau Kanton in an apartment.

Annually our income gross 150K, yearly savings net 20K.

Emergency fund 30K CHF.

No Saule 2 and 3a/b payment.

Debt 18k in foreign currency, 0% interest, handling fee around 1%.

Retirement planned in CH, close to zero pension expected from earlier employment at home country.

Abroad we have one property what we are ready to sell, at the current price calculating with worst case scenario 250K CHF. Currently it is abandoned, yearly maintenance costs are 2K CHF.

We are paying 2020CHF for the rent per month.

Both of us extremely happy with the local community and apartment.

The market price of the flat is around 800K CHF.

Goal:

Allocate the old house value to CH

Make the right steps to own a property at my current village without risking the retirement

Question:

Which solution would you choose if you were me?

Buying the flat with the down payment from the property abroad

Wait couple years to generate more wealth to be able to max out the Pillar 2 and 3 then buy the flat

Stay in rent mode and start to make an investment portfolio in order to make sure that enough money collected for the retirement

If you have other solution what I did not considered, I would be grateful if you share with me.

Your main question is about the property in CH. If that is really your goal, it would make sense to buy as soon as you sell your current place and use 160k (20 pct) for the downpayment. Also pay moving costs, etc cash. This leaves you some money left to beef up your emergency fund (aim for 6 months living expenses, so 65k) and some to invest as well

But do know that financially it may not be your best option. Your mortgage of 640k will cost you same as the rent, give or take.

You are way behind on retirement, sorry for being blunt. In your shoes, I‘d keep renting and save aggressively - 20k savings on 150k gross is not really that impressive. On this forum, you find people (not me though😀) that with your family size spend 40-50k, saving and investing the rest. Aim to save 50k. For really good advoce, post your budget, people here will help to identify how you can cut costs

How much taxes do you pay? Do you both work? If you share more details it is easier to help you. If you both work and pay more than 15k in taxes, it could make sense to open pillar 3a for both of you. You can invest it in ETFs but already get a good return via tax savings out the gate. Your income is not high enough for extra pillar 2a payments to make sense, so once you have maxed 3a, open a broker account and invest every month/ 3 months in ETFs for the balance

Hello and welcome to the forum! It’s great that you have decided to take your financial destiny in your own hands! This community can give you lots of great advices!

I will be also blunt frank. First, with your first name there is not much to hide what your “home country” is. I know for sure couple of forum members from the same country, maybe they can give you some more specific hints and share their own experience.

Second, if you compare things, it is straightforward that people from outside of “MSCI World” countries tend to overestimate the importance of real estate as an investment asset. Or as a wealth component, let’s say. Based on own experience and that of previous generations, they think it is the only type of assets safe from inflation and confiscation.

Well, that’s not the case. The most important growth asset is stocks. There are ways to invest in stocks simply, safe and cheap.

Now, ask yourself, how much of your desire to buy a property in Switzerland is a psychological bias based on previous experience and lack of knowledge about other types of investment?

My solution to your dilemma would be simple:

continue renting, maybe another place.

Sell your old property.

Invest in a diversified stocks portfolio, maybe in an all-world fund.

Start investing in 3a. I think you just missed a deadline for 2024.

Given how protected renters are in CH, why not plan to stay there for the next 10-15y?

You can always revisit your plan if eg your family situation changes (second kid, first kid moving out, etc)

As others have said if your plan is to retire in CH, figuring out your pension strategy is critical given you missed already one third/half of your contributions already.

Would be a good idea to sit down and estimate what your retirement might look like if you don’t take actions (working until retirement age, getting pillar1 and pillar2 with missing years of contributions). Based on that figure out if you need to drastically increase your savings.

thanks for being blunt, I need to feel the wake up call to rearrange my financials.

I hear you that you are also share my opinon about feeling the risk about the possibility for retirement.

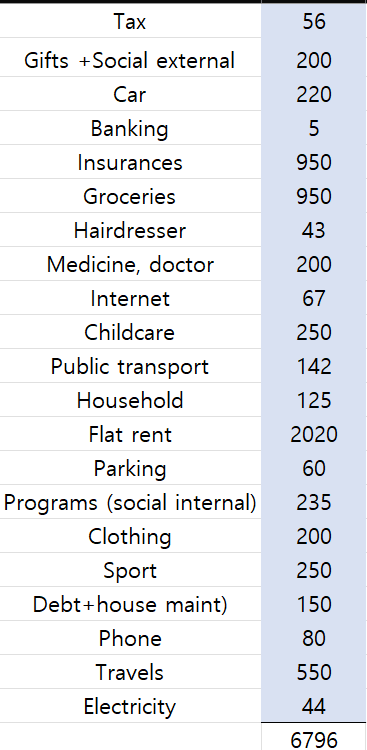

Here are more details on the budget:

My income ( 100% penzum) 140-145K per year

My wife income( entreprenuer) 5-10K per year

Regarding taxing I have to check, from last year we did not have the declaration as my wife business generated negative profit(just started in November 2023).

thanks for being straight-forward, I prefer this style. Best results to trigger me.

Honestly I am not planed to hide my roots, I believe in this equation better to keep it out.

However you touched a very important point, generational behaviour. For sure my unconscious drive what I had seen, learn from my close environment, which is : physical “stuff” is always higher rated then any other wealth.

By moving and changing my environement helps a lot to release this type of “financial traumas”.

Thanks for the advice, I see now that the safest bet for the relaxing life including retirement is to focus on investing.

Liquidate the old house and start being disciplined in investment.

The need for life stability: how dependent are you on your current appartment? Could you find a similar place at an affordable price in your current village or another place where you’d be willing to live if you had to (say the appartment is sold for own use by the new owner, against which you’d be somewhat protected but my guess is nobody needs the hassle of a landlord who doesn’t want them on their property). That need could lead to a “buy” decision. It can also be negative if you expect you might have to move in the future.

The need for financial stability: in general, in Switzerland, renting is more profitable than owning provided one does save the difference and doesn’t just spend whatever is available as is the default philosophy (both of our social insurances/pension schemes and of most people I know). That need would lead toward a “keep renting and invest what you can” decision.

On a general basis, I really don’t like buying appartments as co-ownership can lead to all sorts of frictions between the owners and if someone systematically blocks the improvements you’d want to have done, or pushes for improvements you don’t deem necessary, or have terrible use of the common places, getting insulated from them to protect our peace of mind becomes pretty difficult (while a renter could just find another place to live in and move on).

As you seem to enjoy your neighborhood, buying an appartment might be an option, though. Be aware that people can move in and out and that you might enjoy your future neighbors less than your current ones.

A few questions:

Is your flat for sale currently? Is the current owner willing to sell it and would that be their primary choice or more of a favor they’d do to you? Is your landlord a commercial entity or a private owner?

Are one of you of Swiss nationality or on a C permit? Is there a scenario where you couldn’t stay in Switzerland despite wanting to because of administrative hassle, loss of work or any other reason?

How desirable is your location and how easy would it be to sell the property you plan on acquireing?

You don’t mention your current savings amount. Should we assume that your total savings are the emergency fund + property abroad (roughly 280k)?

How likely is it that your household income increases or decreases in the future?

The only debt shown on your initial post are 18k at 0%. Your budget shows 249 CHF/month of “Debt+house maint”. Are the 249.-/month comprised of 234.-/month of house maintenance and 15.-/month of the “1% handling fees” of your debt or are there other debt related items that we are not aware of? Is part of it amortization on the 18k debt?

While I admire your wifes entrepreneurship, what is the realistic income she can generate next year and the 2-3 years ahead? Is she employable and at what salary level? Could she moonlight and start up business while working a job until she makes 50-60k?

Given your lack of pension funds you may need some real tough conversations on that.

If you need 130k spending power in retirement, and pillar 1 will only give you about 20k/year combined IF you stay next 20 years, your required nest egg is 2.75M chf at retirement (todays chf)

If we assume a return of 5 pct over inflation (fairly aggressive) and you immediately invest the 250k, you need an additional 63k invested every year for next 20 years to get there. You will get some money from pillar 2 as well, which i here ignore for simplicity, but point is that you need to really have your challenge sink in. The appartment is a distraction from that imv. Most people get shocked at how little income a sizable portfolio realistically generates

How will you do this? Painful budget cuts or increase income?

@finalcountdown@Dr.PI have raised great points and given good suggestions. Indeed to have proper retirements the next 20 years would need higher savings rate and investments

My question for you @Laszlo_P is a bit different. The struggle you see here is driven by entering Switzerland at relatively later stage in your career. And since you come from other country , the wealth accumulated (in terms of property) might not be sizeable enough to compensate the missing 15 years of work life , AHV & BVG contributions

So the question could be - do you really need to retire in CH? Because if that’s not the case, you might be able to manage with less aggressive plan.

You touched the most sensitive part of the equation.

We hope and believe that within 2-3 year it will make around 40K per year.

If not we ,will downgrade as part time and my wife will look for a job.

The entire 2025 will be a trial period to see that our efforts and outcomes are match.

Thanks for the calculation, the gap is substantial, so I think we need to work on both end.

Increase the income and reduce the cost.

Yes indeed, planning is now very vital. The rest 25 year to be prepared for the retirement ages are not so promising without taking hard, painful turns.

The raised question is fully valid, it is hard to commit myself that what my 65yo brain and heart will decide. Currently with my wife mutually agreed that we plan ourselves to stay in CH for our retirement ages.

Our close family quite old, bigger family spreaded around the globe, friendships are under also a reboot, the sentimental values what we need from our own country can be satisfied via 2-3x visit per year.

So we need that “aggressive plan” to be able to stay here.

Calculating what for pillar 3a and ETFs? Returns? Accumulation rates? This depends on what you invest it in and as this would - should - be Capital at risk to get any good returns, just simulations of course. I‘d simply assume a 5 pct real return when invested in index funds, either via 3a or ETFs

I suggest you start educating yourself on (early) retirement, unless concepts like 4% rule, SORR, SWR, etc are all familiar to you.

I don’t know your age. But if young and sprightly, I’d redirect some of your 20k savings in a 3rd pillard. 100% tax-deductible and money towards your first real estate buy in Switzerland.

Another Hungarian here - FYI our wonderful goverment only pays pension if you worked 15 years there. I have an engineer friend who just went to pension, worked ~10 years in Hungary and lost it all. Just in case you did not know it, for my friend it was a big surprise.

With the house question I cannot help, we pay ~4.5K for housing in GE (rental), financially it is bit better than a loan. But the worse thing is that even if we had infinite money, it would be mission impossible to find a place as good as the one we live in, simply because they do not build houses like this anymore and whenever we hear that one is going to become available someone in the owner’s family moves in. Unsure how is the housing market in AR.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.