I want to restructure my portfolio (goal: long-term investment and asset growth) and consider my as well as our (my partner and I, getting married in summer 2025) overall financial situation (all figures in CHF). I would appreciate your opinions and advice. Please also correct me on anything that is incorrect or not well thought out.

Invest the capital independently through Saxo Bank.

Set aside a reserve in bank accounts and invest any excess cash every 3 months.

Review Pillar 3a with VIAC, possibly consider Finpension.

VT + Swiss ETF. Home bias somewhere between 20% and 40%.

Broker/ETF selection

Broker choice: Saxo Bank. I can trade VT there, and the fees are better than with Swissquote. I sleep better with it (I know the fees of IBKR are unbeatable).

ETF selection: VT + either CHSPI or SLICHA → Currently, I’m thinking of an 80/20 split. I’m unsure if one of CHSPI or SLICHA is “better” for my case.

Bank accounts, reserve:

CHF 40,000. This reserve might seem high to some, but for several reasons, we believe we need it. I’ve listed this point mainly for completeness. The excess money will be invested every 3 months.

Pillar 3a

We have a significant portion with VIAC and only a small part with Raiffeisen. We plan to liquidate the Raiffeisen account and transfer it to VIAC. I’ve read that Finpension allows for better portfolio customization than VIAC, potentially creating a more balanced global portfolio. However, VIAC is interesting because it offers the possibility of taking out a mortgage. While this isn’t a current concern, it might be relevant in the future. I would balance the strong Swiss orientation of VIAC Global 100 with my Saxo Bank portfolio and not overweight Switzerland too much (20% CHSPI or SLICHA).

Planned approach

Invest currently invested capital, i.e., CHF 150,000, with Saxo Bank.

Invest cash from private and savings accounts (CHF 45,000).

Invest an additional CHF 15,000 at Saxo Bank by the end of the year.

I would be very happy if you could give me feedback on my thoughts (choice of ETFs, portfolio allocation, general approach, etc.). I also have two further questions:

Allocation between Swiss and foreign markets: Pillar 3a with VIAC Global 100 is very Swiss-oriented. Additionally, Pillar 2 is also Swiss-oriented. We plan to invest more in our free retirement savings (Saxo Bank) than in Pillar 3a. This means the Swiss component will decrease. Does it make sense to consider a Finpension account and modify it to be less Swiss-oriented?

I’ve read about CHSPI and SLICHA in several forums. As usual, it probably depends on the specific situation which is better. Still, my question: Is there one that is “better” in my case? Or maybe something entirely different?

Your portfolio (excluding cash and 2a) boils down to following

X% World Equities + Y% Swiss equities

Y is upto you to decide. X+Y = 100%

But I would suggest to do a calculation if you would be better off keeping Swiss portion within the 3a as much as possible. Reason is that Swiss equities tend to have higher dividend portion vs the world equities.

You would need to account for

expected dividend yields for X and Y

Expected total return for X and Y

marginal tax rate to be applied on dividends in Saxo

Lumpsum withdrawal rate when cashing out 3a

Wealth tax

Sometime back there was similar sofuasion on where to place Bonds , inside or outside 3a. Read here

Overall looks like a solid plan to me.

I use Finpension for 3A, but didnt readjust the strategy. I balance the overall home bias with a lower bias in my 3B portfolio.

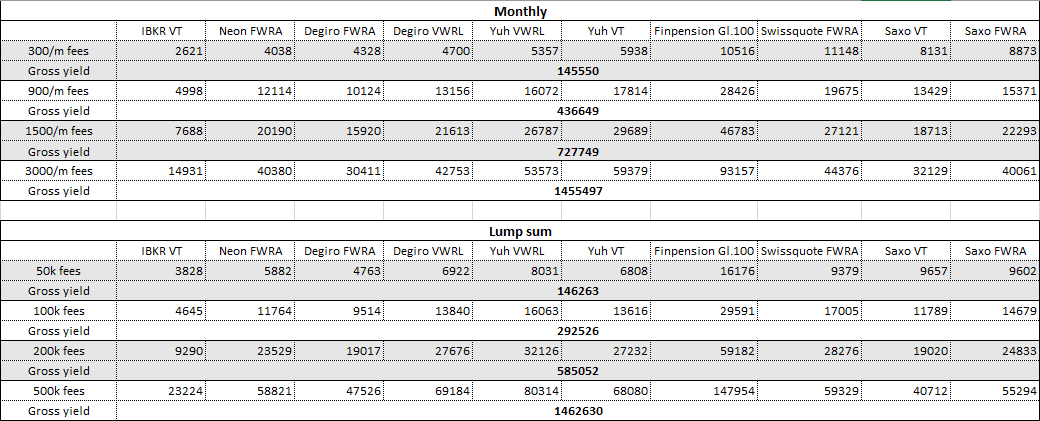

That is surely a point you have to consider. But the fees of Swiss brokers are indeed much higher. If you calculate it here, and expect that you invest 4000.- monthly (wild guess based on the large savings amount at your age), you see that you’ll ‘donate’ >500 CHF per year to Saxo Bank. *Update: might be a glitch in the calculator, total amount of fees is likely lower; see discussion below

I don’t say thats a clear dealbreaker, it’s just something to keep in mind while deciding.

I use CHSPI. I have no desire to rebalance the distribution of companies in the index (reason to go for SLICHA) and double the TER for SLICHA (0.2% vs 0.1% of CHSPI) is a big argument to me as well.

So the biggest impact is due to currency exchange. I still didn’t get to 500CHF delta. I think Poorswiss calculator is assuming you can’t buy VT and hence lose out on dividends

Actually you might be right. I think the problem is that the custody fee is not capped in the calculator. If you double the portfolio value you double the yearly costs by more than 120.- even if you do not pay in.

Let’s see whether he reads this forum as well @anon95353169

You are correct, the calculator assumes saxo has no US ETFs. If you click on any of the item, you can see the details and you will see that custody fees are capped but there is no cap on US dividends loss.

I am waiting for an official confirmation from Saxo about US ETFs before I update the calculator and the articles. Keep in mind that until a few days ago, we could not trade US ETFs .

Great, thanks for the answer! I missed that the triangles mean that the details can be expanded, interpreted it first as just another style of bullet points.

Just be careful with dividend substitute payments on lent-out securities. This generally is a clusterfuck of wantonly and wrongly applied, incompatible regulations. You can’t get a straight word out of IBKR, maybe Saxo is more on point.

Since you are already with Truewealth, I assume you have reasons to not use their 3a? I use that one and I am pretty happy with it. Earlier this summer, they heavily improved their offering by switching relevant investment classes to pension fund classes. In my understanding, Truewealth 3a is overall quite a bit less expensive than Finpension.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.