Renovation no (some deduction for e.g. energy efficient still might happen at the cantonal level). Mortage, yes but prorated on ratio of rental properties over overall wealth.

1 Like

There is no change on the wealth tax side. The value of the principal on Dec 31 will still be deductible.

I can only recommend to everyone to look at this page. There are all the information and materials we need to make our mind.

1 Like

Fyi GFS poll is out: 1. SRG-Umfrage: So steht es um die Abschaffung des Eigenmietwerts - News - SRF

1 Like

Still early, but still quite clear that it will likely pass.

Also again the very clear trend of old people (the property owning class), a lot more in favor.

Well gonna need to switch to box spreads for leverage then it seems…

2 Likes

I will vote no, although I think the tax is bullshit. But not being able to deduct my margin loan for stocks, but having to pay tax for the dividends is completely fucked and makes less sense than the original imputed rent value tax.

Although I may get back a bit more of my withholding tax that way, probably more than the CHF 2’500 I have to pay more in tax with the new regime because of the interest situation.

So it does not matter anyhow too much for me. I always have the possibility to pay back all my debt at the blink of an eye. But I don’t want to because all money is debt and I prefer to owe to somebody than that somebody owes me. Especially if that somebody is a central bank which needs inflation to make the economy work.

Our genius government not even was able to make tax declaration easier because we still need to declare the value of the real estate and that is a big source of dispute.

Yes, it will be more crucial to calculate, if a margin makes sense - the dividend/interest income has to be higher (more or less by the marginal tax rate, someone has).

The value of debt goes down with inflation, so you have to add inflation to your formula. But you do not know inflation in advance, that is the biggest risk you have as debt-free person with money, money is technically debt of the central to you. The central bank that can change the rules at any time.

I cannot calculate the tax difference the new rule makes for me. At the moment I get back only a little of my withholding tax because I can deduct debt interest. The difference would be CHF 2500 more tax if the withholding tax situation would not change. But it will change and at the end they probably give away money to people who don’t need it like always: me.

1 Like

You could also look into short box spreads for cheap leverage. Not tax deductible, but you pay risk free rate + 20-30 bps

—

Btw when would this go into effect?

1 Like

Gosh darn it this was the only thing that made my gigantic 7+% interest on my UK student loan repayments worthwhile…

2 Likes

Well, technically, the repayments are even more valuable if the interests aren’t tax deductible and presumably, the value of the debt itself comes from the education you’ve gotten and the prospects it gives you?

Sorry, I don’t understand.

Our education system (and the proposed change in tax law) says that debt is bad. But then our education system does not teach what money is (debt).

So, our education is a bit like the crowd in the stock market or the banker that tells you what to do: you are better off doing the reverse they tell you…

I am not a fan of our education system. It takes away the natural wish to learn that every kid has and at the end of a decade or so locking you up in a room having to listen to somebody you probably hate and is boring many kids can barely read or write.

John Lennon said it best: “As soon as your born they make you feel small by giving you no time instead of it all… When they’ve tortured and scared you for twenty odd years they expect you to pick a career when you can’t really function you’re so full of fear.”

1 Like

Seems the outcome of the vote is not that clear.

According to this article (German) the majority of asked persons could not reason to why they would vote yes and did guess the voting will fail.

Opposition comes from all sites, mainly because the coupling with the debt interest tax reduction. The rich and the poor, the renters and the owners, everybody has potential to lose with the new regime. If the majority loses and then has to pay additional taxes to support the minority that gains… how could that pass?

- Renters are against it because obviously they only lose; no more debt reduction and higher overall tax.

- Owners are against it if they have to pay more (me) and for it if they have to pay less (mainly rich retired folks).

- Landlords are against it if they own other good than rented out houses; they probably have to pay more then.

- Companies in the construction business are against it because they may lose work when it cannot be deducted from tax any longer.

That leaves only the rich retired folks. On an individual level this may be a very big tax reduction for very few people but the rest of the country has to pay for it.

I still don’t see a clear yes. Another missed chance to get rid of a stupid tax. Why they try to enforce the “debt is bad” thinking into that tax reform. And if debt is so bad, why we have money at all (which is debt)? They want to lower the overall debt, but as long as money is losing value (and it has to lose value for the economy to work) debt is actually a good thing! At least for me.

They did it again. It is not about the removal of imputed rental value anymore but about making debt more expensive. And it is not clear to me why landlords are better off than the rest of us. Are they really that much in need of more money from everybody else?

But you know that all derivatives take interest into account and have it included in price building, no? Indeed you could not deduct it from tax if using this kind of instruments. If derivatives would not take interest into account some arbitrage trading would soon do it anyhow…

I suppose the tax change will go into effect very soon, maybe for 2026 or 2027, because all the details are already laid out.

There are plenty of unsophisticated people who have little investments apart from their house. Even fewer people have debt other than a mortgage. Also, the mortgage rates are relatively low now, and Eigenmietwert appears to be high in some places, e.g. in Zürich. People just see that it benefits them right now and vote Yes.

It is a common misconception that debt is classified according to the collateral. It does not matter if it is a mortgage or your last invoice at the pub. Debt is debt for tax.

Exactly as I said, rich retired people with no debt and high imputed rental value will profit. No real estate owner in Zurich with no or low debt is poor, that is nonsense with the current real estate bubble. However, rich owners with no debt are the only people profiting from the change. At cost of everybody else…

1 Like

What consequences does the reform have for the stability of the financial system?

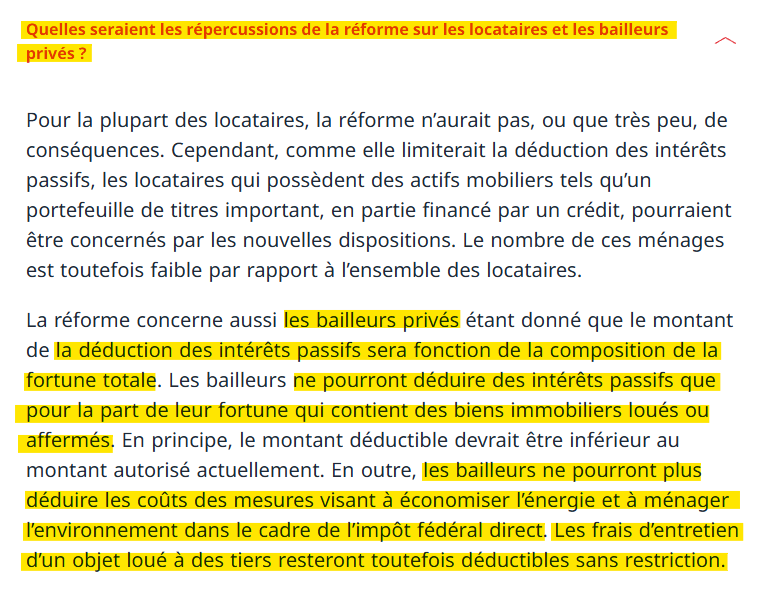

Current law provides tax incentives to maintain a high long-term mortgage because the associated interest expenses qualify for deductions. The system change approved by Parliament, with its new regulation on the deduction of debt interest, significantly restricts these debt incentives, since – apart from the first-time buyer’s deduction – only debt interest on rented or leased properties is deductible. If, for example, a person’s assets consist of a home, a bank account, and securities, they will no longer be able to deduct debt interest after the system change.

As a result of the reform, debt interest can no longer be deducted even for credit-financed investments in securities (e.g., Lombard loans), provided there are no immovable rented or leased assets. The current tax planning options are thus restricted. The tax incentive to generate debt-financed dividend income or capital gains will therefore be significantly reduced after a system change.

Limiting the interest deduction strengthens the incentive to repay debt more quickly, for example, by reducing savings deposits or securities investments or foregoing non-essential consumer spending. Swiss households pay off their mortgage debt comparatively late (e.g., by withdrawing pension fund assets in old age).

The reform can therefore lead to a long-term reduction in private household debt and thus have a positive impact on banks’ credit risks and, consequently, on the stability of the financial system, since mortgages represent an important component of banks’ balance sheets—to varying degrees depending on the bank. At the same time, the lower securities holdings and mortgages can reduce banks’ earnings.

1 Like

Two of my friends living in Zürich canton claim to benefit greatly from the change. I think the only debt they have is mortgage (in other words: they only have the cheapest tax-deductible debt on the market). They are not retired and aren’t planning on repaying beyond the requirements, as far as I know.

@Tony1337 most likely knows. Hence the mention of risk free rate. If nothing can be deducted anymore, superior margins win.

1 Like

Which is funny because lowering household debt was an explicit goal when they made the tradeoff/agreement in parliament.

I’m sure it’ll make sense for some debt, so the overall level will likely go down.