For me the part with debt is relevant. I have margin debt and a mortgage. I suppose it does not matter what collateral is used for the debt, I interpret the text so that only debt on rented real estate can be deducted.

Here is a simulation of the new tax situation:

For me it says that I save now 2195 CHF in tax. In other words, without that tax I would pay 2195 CHF more than now.

Never thought I would actually save money with this stupid tax. Also I see it very unfair to limit the debt deduction to “immovable property”. That would not include stocks that pay dividends and I think this is not fair. Holding a house would then be more favorable to holding a REIT.

I never thought that I may vote no to quit that stupid tax, but it looks like I will and it will lose the vote again. Of course I could just pay back the debt, but then I may have liquidity problems as my cashflow from the stocks I bought on credit is higher than the debt interest.

That would save me some money but put me to additional forex risk. The mortgage is in CHF and the margin credit in USD.

But anyhow, if I interpret the text correctly there is no difference, it does not matter if the collateral for your debt is a house or stocks.

Next year they will rise the tax value of all real estate in Kanton Zurich, so I’ll have to check the new situation.

For me as always they put two non-related things together: debt and real estate. Now you can deduct debt that does not produce any taxable income, like buying a Ferrari on credit. And of course buying a house on credit.

The new situation would not even let you deduct the debt interest if it produces taxable income. I think that is not fair and it should not be combined with the removal of the imputed rental value tax.

Just a little change in the text and it would be OK for me: instead of the quota of “immovable” Assets to all assets it should be the quota of tax-income producing assets to total assets. Means you cannot deduct interest for the Ferrari or the house, but for dividend paying stocks.

Yes, but it states that you still can deduct interest if you rent out. But not if you buy dividend producing stocks with it. That is not fair and makes no sense. If you buy a REIT on credit you cannot deduct the interest, if you buy a house on credit and rent it you can. That is OK, but why not with the REIT?

It did not make sense however that until now you could deduct any debt interest, producing taxable income or not.

After reading carefully the law and the modifications, it looks to me that it won’t be possible to deduct any interest if you don’t own any real estate in Switzerland… which makes no sense

That would be an incredibly vast change and the amount is also tied to your real estate?

I see zero chance for that passing. Think about how many people take on loans for their BMWs and now tell them the interest just got 30% more expensive, because they don’t own real estate.

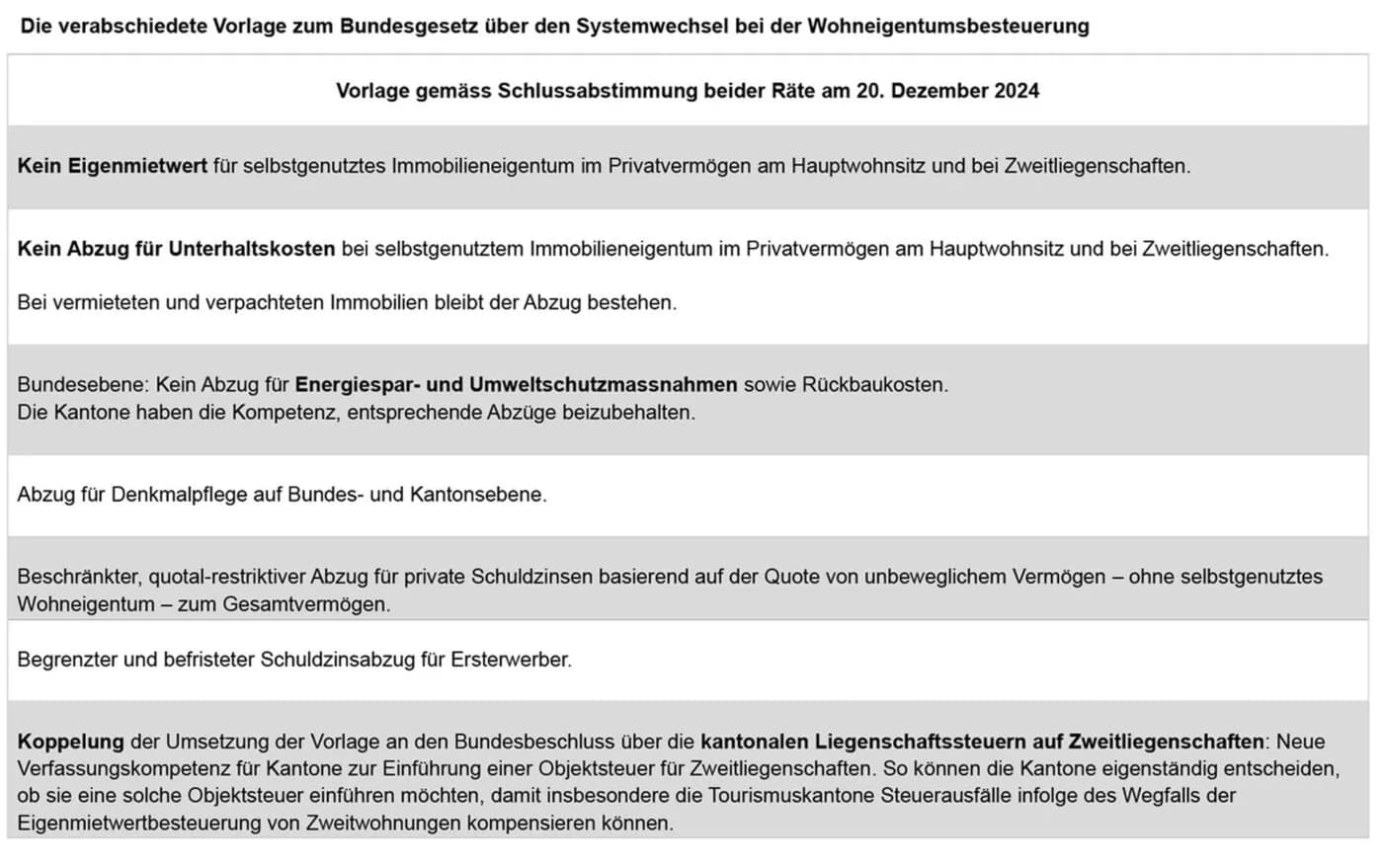

As I said the changes in loan interest deduction and imputed rental value are tied together. It does not depend if you own a house or not. This is the relevant part:

die privaten Schuldzinsen im Verhältnis aller in der Schweiz gelegenen unbeweglichen Vermögenswerte, mit Ausnahme der Liegenschaften oder Liegenschaftsteile, die der steuerpflichtigen Person aufgrund von Eigentum oder eines unentgeltlichen Nutzungsrechts für den Eigengebrauch zur Verfügung stehen, zu den gesamten Vermögenswerten

Example: you own a Ferrari worth 300k, a house you live in worth 900k and another house you rent worth 700k. Your debt interest is 50k.

Old: you could deduct 50k

New: you could deduct only the interest in proportion of the house you rent out to the total estate: that is 300+900+700=2m, 700k/2m = 35%, you could deduct 17.5k

If you don’t own a house you rent out you can deduct nothing.

This part of the law is very complicate and is not fair. There should be a difference between taxed income producing assets and non producing assets and then one could deduct the interest in proportion to that number. Instead of saying “unbeweglichen” it should say “steuerbares Einkommen generierenden” (strike out “immovable” and put in “taxable income generating”).

If they really put that to vote with this text I probably will vote “no”. Prefer to pay a stupid tax than to pay more of an even more stupid tax… when will it ever rain brains in Bern?

But that’s what will happen if you remove imputed rent (and keep deductions), people can splurge into high amount of housing with no taxes (compared to renters).

That is exactly what happens now already, without removing the imputed rent.

I never calculated the tax effect of my house before and was surprised that it actually saves me more than 2’000 CHF in taxes every year. However, they did not change the value of the property in like 20 years and plan to do so next year.

The tax savings are only due to the deduction of debt interest. I’m using only the flat rate deduction on maintenance costs.

Last financial voting was about 13th AHV and I did not vote with my wallet, did vote “no”, even I do profit. This time I probably will vote with my wallet…

FYI I think they assumed people are not stupid and would get into that kind of debt to grow their wealth (they don’t get into debt for the 300k ferrari, but to invest 300k in stock).

(and because capital gain is not taxed, “income generating” would be the wrong way to differentiate)

(they cover the reasoning in the commission report)

I think “income generating” is exactly the right word for stocks that pay a higher dividend than the interest rate.

Now “stupid” is a question of definition. In Switzerland people buy overpriced real estate on credit. There was a whole generation in Switzerland that has not seen a bust in real estate prices. There were several in the stock market.

Stocks are way more liquid than real estate and you can manage the risk on a micro level. You cannot sell your house room by room, it will be sold at garbage price by the bank once it is not worth enough for the collateral of your mortgage.

Now I have a really low mortgage, about 20% of the real estate value. And about 20% of my stocks portfolio is on margin. I do this mainly because I need money to live and don’t want to sell stocks just for that reason.

I was surprised that even with such a small mortgage I save money on tax. What will happen to the people that have 80% mortgage or more? The tax would kill them financially, it can be deducted only for a very small time.

Agree on capital gain tax, that would be way worse and maybe a reason for me to no longer have my tax residency in Switzerland. Last year I spent only 5 months in Switzerland and I keep my residence here merely for tax purposes.

As I said, I will vote with my wallet this time. If I lose I will still keep my tax residency in Switzerland as long as there is no capital gains tax.

Inputed rental income is maligned for whatever reason, but it’s actually a pretty fair tax, without too many distortive effects. As nabalzbhf said, if you want fairness between owner-occupiers and renters, you would need to let renters deduct their rent, but it has massive tax revenues effects.

Then there’s the removal of the tax deductions for renovations, which long term will have big effects on the quality of the housing stock.

All of this to apparently benefit almost no one but older people with fully paid out houses.

So to recap:

loss of tax fairness between owner-occupiers and renters

loss of tax revenues for the government

loss of incentives to keep the housing stock in good shape

doesn’t even help most people

Am I missing something? It seems bad in pretty much every regard, except for wealthy retirees.

I think you are framing it from very different perspective. Leaving aside the fairness or not, I see imputed income tax as a random tax where people need to pay tax without generating income.

If someone own the house, they pay wealth tax. If revenue generation is an issue, then wealth tax on RE should be reviewed.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.