The detail per stock is not shared by Vanguard or Blackrock in the published documents but you could simply put the total of dividend and see if it’s accepted by the tax authorities.

a direct link to data which shows that ETF was holding the securities at time of dividend payment

a proof that investor actually held the ETF

The first two things needs some sort of tech to keep the databases using public or private APIs and most likely some agreement between Finpension and ETF provider

I believe this is why ishares was selected because then multiple ETFs can be covered

It’s very interesting for sure, but the way I read it it would currently apply to iShares ETFs held within Finpension? As far as I understand given some of the available investments in Finpension are institutional mutual funds they can already recover the taxes on dividends. In any case it could be a great start for wider reclaiming of dividends for funds held elsewhere?

P.S. hope nobody mentions you can already do this in IBKR, I’m aware.

People who prefer UCITS ETFs (where there is tax leakage for US exposure with other platforms)

People who like Custody in Swiss institutions (where typical custody fees are 0.3% like UBS, ZKB etc)

People who prefer a wealth management platform (bonds, alternate, Stocks all in one place) vs. DIY

You are right, buying VOO in IBKR is much better than buying IUSA via Finpension. DIY portfolio management at IBKR using US ETFs is cheapest and most tax efficient. But I think FP is offering a wealth management one stop shop. IBKR is just a brokerage.

Having said that, I am impressed that FP is trying to find a differentiation in heavily competitive space.

This sounds reasonable. I’d certainly prefer to have all eggs in one basket for simplicity IF I was sufficiently confident about it.

Finpension is great, and looks like they’re looking to do all the right things for people who dig into investing (eg domicile in Schwyz for lowest tax upon withdrawal, good, flexible and transparent platform and app, wide range of investment options including the CS institutional mutual funds like Quality which nobody else has to my knowledge) but the fact of the matter is it’s not tested, it’s just too young to have had any sizeable number of people withdrawing their 3As from it. There’s probably heritage being built on the 2nd pillar offering. I really hope all goes swell, my 3A is with them after long consideration and I’ve no complaints. There was talk here that they’re pioneers but indeed young and untested in a fiercely competitive space, and that if a whale systemic bank decided to match their offerings then they’d be in trouble.

P.S. re banks, PF has a flat 72CHF/year fee for custody which also considers 18CHF/quarter trading fees as custody fee credits, so the custody is essentially free with any sort of regular buying. UBS is indeed 0.3% and 1% per trade which adds up fast. I thought ZKB was looking to make itself free? Not looking into it as I am not in ZH.

@finpension for a measly 0.39% p.a. rebate, I’m sure we can find volunteers to lobby most if not all cantons to get out of the hypothetical, get your methodology validated and pressure the Confederacy to follow through.

I wrote to Vanguard Switzerland, asking if they could provide similar documentation for e.g. VUSA. Will report when they reply.

You can reclaim withholding tax with DA-1 on Säule 3a and Freizügigkeit, even though you don’t declare those for taxes, right? Or does finpension offer taxable accounts I’m not aware of?

I think DA-1 is to get a tax credit in switzerland. But pension funds want to have the withholding tax money back from the USA, because they don’t pay any taxes in Switzerland. I don’t know how they do it exactly, but the pension fund or the funds bought by them will have to get that directly from the USA.

I don’t know how you can make extra money with it, because it will probably be copied quickly. But if it works, it will be the best thing since sliced bread. This is real financial innovation and I hope that the publicity alone will fill your coffers many times over.

With this new approach, some other services might get released (through other service providers) which can help all investors get their tax credit back for unrecoverable taxes.

Personally I don’t like US domicile ETFs but I accept them because of their advantages. But if some services evolve to reduce the gap for DIY investors, this preference would change

Ideally a fund house like UBS or Swisscanto should start providing these (unrecoverable tax credit) services for CH domicile Funds. Since these funds can be bought on exchanges, they would also work for DIY investors and will make it easier for Ictax too as they would need to deal with just one/two verifications. This will also help them gain share from IE domiciled funds.

For example UBS S&P 500 ETF or Fund domiciled in CH with tax credit facility and TER of <0.10% will be great.

It’s a pity that Swiss residents are buying IE domiciled funds provided by American companies. Money from Swiss residents should be going to Swiss funds. And UBS / Swisscanto should make it possible. It would be best for everyone.

I understand that because of Swiss WHT 35%, CH domicile funds are less attractive for International investors. But for Swiss investors this wouldn’t matter

I think you are simply not Finpension‘s target audience. ANY roboadviser will have more fees than diy self-managing.

They could however offer a simple brokerage account with no such functionality. But that could cost them customers from the robo and therefore make it not beneficial.

German free brokers such as scalable offer both. Free brokerage and a roboadvisor service for ~0.5% TER

I’m just now reading up on reclaiming withholding tax.

If I’m retired with no taxable income besides dividends from US stocks, and those dividends are low enough to cause zero income tax (neither federal nor cantonal income tax), “only” wealth tax, then reclaiming the withholding tax with DA-1 is not possible, because the maximum that can be reclaimed is zero?

In that case, the withheld 15% of dividends are truly lost, both for IE and US domiciled fonds? At least until dividends grow until they exceed the threshold above which income tax gets >0?

Yes, not possible. You can only reclaim parts of your divdend taxes you paid. This credit is solely to prevent double taxation. And as you were only taxed once, not possible to claim.

In your case a fund like SPYI and VWRL would also be more cost/tax effective probably. As you lose a double layer in tax on ex-US holdings in VT for example.

E: Also in that case a home bias makes even more sense tax wise. You have zero withholding tax on swiss stocks/funds after getting back the Verrechnungssteuer and that is independent of you tax rate.

Other robo-advisors would certainly be the first to offer the same.

I could imagine that it will take many years until the data is integrated in ICTax, which would be needed for people buying a world or US ETF through a broker (Swissquote etc.).

But not every online service keeps a securities account for you and could confirm the exact amount of tax withheld in your name.

Gotta look at it from the taxman’s perspective, who is used (and encouraged) to grant tax credits/refunds in a restrictive way: Are they going to accept a report from some random online services that doesn’t keep your account and can’t tell how many shares you actually own - vs. receiving a report from a Swiss financial services provider through which you actually hold your shares?

No, wrong.

Though pension funds held through such accounts may be exempt from foreign and/or withholding tax anyway.

Keep in mind that most US-domiciled ETFs (that are popular on this forum) will also hold non-US securities - which would then be subject to 15% withholding tax (with W8-BEN).

Example:

British company distributing to US ETF: 0% withholding tax.

US ETF distributing to you: 15% withholding tax.

British company distributing to Irish ETF: 0% withholding tax.

Irish ETF distributing to you: 0% withholding tax.

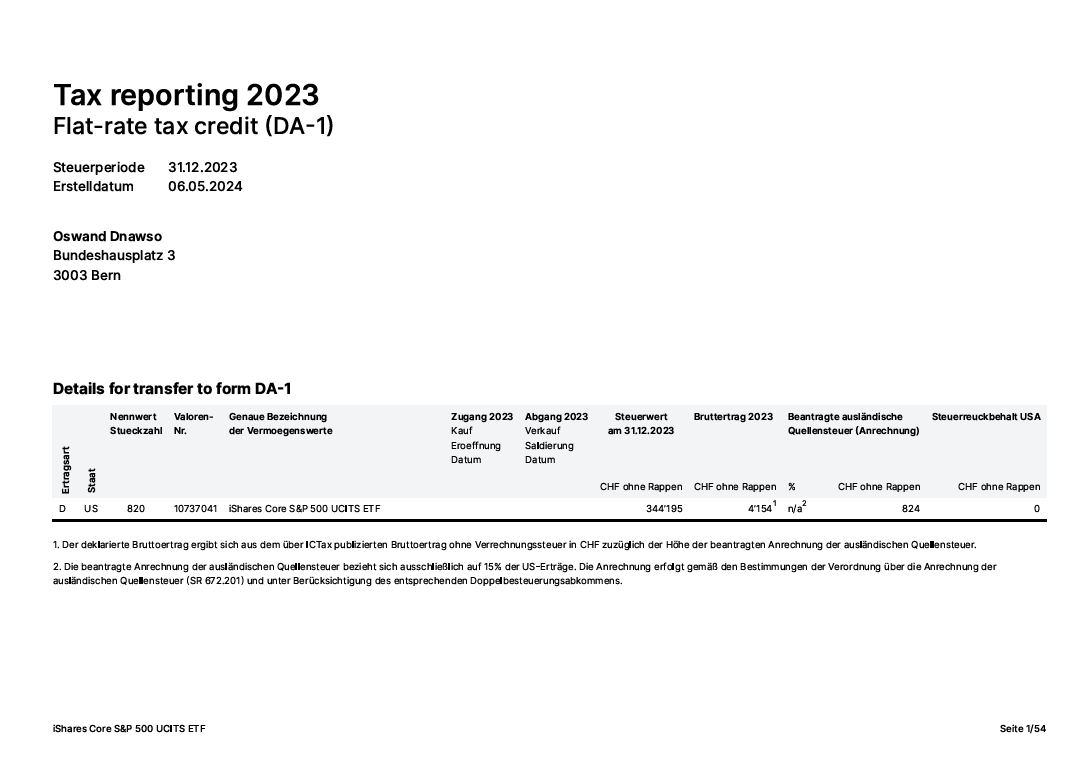

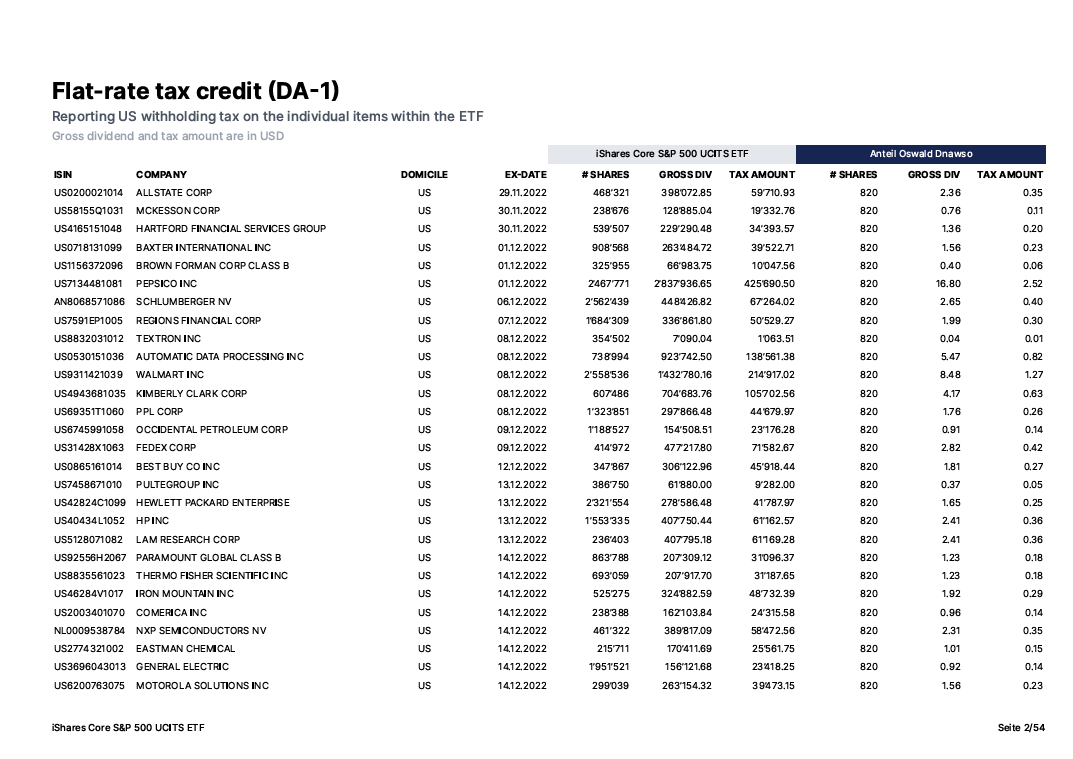

I’ve looked into Finpension’s tax reporting module [source] and coded my own implementation. Obviously the numbers aren’t correct yet (but I use real data, just have to fix all the calculations). It’s actually very easy to do. When I get it to a end-user usable state I could release if for free and you can generate your own reports.

These are screenshots from a generated 54-page PDF. Kinda copied the layout from Finpension a bit, sorry…

Why is it 54 pages? It basically contains all received dividends, sorted by date.

Things I still need to implement:

Right now I assume that outstanding shares don’t change and the ETF owner holds the same amount over the whole year. Obviously that is impractical, but it’s a first MVP. So that’s an important thing I’d have to tackle.

Getting calculations right.

Zugang/Abgang: @finpension It wasn’t visible in your article what is meant by that. Just a list of buys/sells of the asset?

Dynamically fetch all data to generate reports for lots of different ETFs on the fly if required.

Where do I get the data from?

Blackrock offers Excel + JSON with all required information, meaning: outstanding shares, what companies are in the ETF, their share, etc.

ICTax’s database is completely open-source [source]. I downloaded the whole dump for the year and match ISINs with their database and get all data, even dividends in CHF. Nice stuff. This one for example is for Apple Inc.

@oswand when we now combine this with the Tax Declaration & ICTax logic, which is that your tax declaration shall contain daily transactions and that the tax authorities believe this. Meaning that if a share had an dividend ex date, the tax office just believes you that you had these shares at that date… the tax office does not require any bank confirmation that you either actually had the shares or received the divident.

If we apply the same principle, we could indeed just create a script that downloads all Dividend Ex Dates as per ICTAX (grossed up, pre-WHT), downloads the daily amount of shares the ETF Held, downloads the number of ETF Shares that existed at that time… and tadaaa we can in combination with your specific number of ETF held at that time create such a report.

So long story short: IF tax authorities approve such approach, we can as well do it for any other holdings we have even outside FP. So we all give FP big kudos, remember them in our daily prayor to lord mannon and then just proceed our DYI investing.

To be honest: I just can’t believe that the swiss tax office was willing to give up on all these tax revenues…

Where was you able to find the .json ?

Also I don’t think blackrock shares all the holdings by day. I mean the porfolio at the end of the year is different than at beginning of the year

I think that the data from Finpension is directly coming form Alladin (the software from Blackrock)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.