I’ve been buying Realty Income (ticker O). In the past I looked at SUI/ELS but these were hugely over-valued and even now after substantial correction seems expensive.

Interested also in AMT and VICI if I can get a decent price.

I’ve been buying Realty Income (ticker O). In the past I looked at SUI/ELS but these were hugely over-valued and even now after substantial correction seems expensive.

Interested also in AMT and VICI if I can get a decent price.

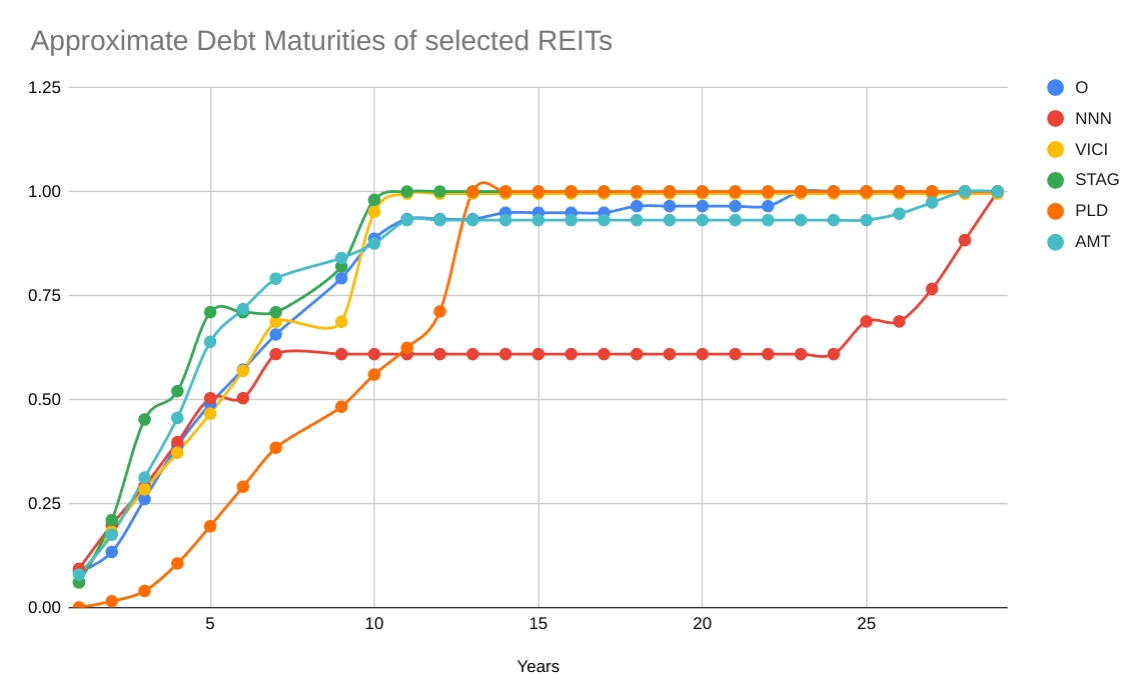

Since we are on the topic of REITs, is there anywhere which has research done on the capital structure of REITs? I’d like to identify candidates for investment by filtering to find REITs with strong balance sheets:

I’d like to identify candidates for investment by filtering to find REITs with strong balance sheets

I don’t want to spoil your enthusiasm, but aren’t you afraid you are getting a bit too active there? I mean, if you can get that information, then everybody else (especially big money) can, too. Which means that this information should be priced in (REITs are publicly traded as far as I know).

Maybe a bit of a fundamental discussion though…

Even if it is fully priced into the REIT (I’m not a believer in the EMH), why do I care?

Even if it is fully priced into the REIT (I’m not a believer in the EMH), why do I care?

Because then your exercise of finding better or worse REITs is futile.

Up to you though.

Why do you want to buy 50% REITs if ‘everything is priced in’? Would you saying buying REITs is futile because ‘everything’ is priced in?

Before you put me on a position that I don’t hold, I don’t believe in the EMH either. I don’t believe in believing. But in general, I think it is fair to assume that given the number of mathematicians and physicists, the sophistication of statistical methods and the sheer computing power that participate on today’s markets, the chances of finding arbitrage as a private investor are near zero.

But in this case, the historical data suggest that RE offers higher risk-adjusted returns than stocks, which is the whole point of this discussion. This may be in contradiction to my first statement, but the data suggest otherwise.

But it isn’t arbitrage. When you choose bonds over stocks etc. you are primarily picking a level of risk/volatility.

I want to lean towards the safest and most robust end of the market. Because I think everybody is way too sanguine and right now, the market is priced for a certain outlook. If that turns out to be too rosy, it will re-price violently against those with poorer quality balance sheets.

Now I’m up to 10% REITs (part of the holding displaced my 1-2 year maturity bond holdings).

Ok. Yeah I don’t know… My concern would just be that if you find a REIT that seems robust to you based on its balance sheet etc. then you would get lower risk, but also lower returns. Which can be a strategy. Still, you’re left with the work of evaluation and the risk that you may be wrong (pick the wrong REIT). Which is why I’m not doing it myself. But I guess I’m just reiterating “EMH lingo” here.

If only there was a crystal ball showing the future to the mighty and great financial people ![]() . I share the same sentiment as @Natural_Ascetic that you shouldn’t overestimate your ability to know more than the market for getting the perfect risk adjusted returns.

. I share the same sentiment as @Natural_Ascetic that you shouldn’t overestimate your ability to know more than the market for getting the perfect risk adjusted returns.

This is absolutely and utterly wrong! Private investors have a number of great advantages over institutional investors:

Sure, you will not be faster than algorithmic funds, but then we should stay away from the HFT arena and compete in areas where we are strongest.

To give an example, around 2018 Super Micro Computer (SMCI) was the subject of a hit piece by Bloomberg claiming that a trojan horse chip was inserted into their motherboards. Their stock price crashed from over $20 down to around $12.

With the right expertise to know that the entire article was BS and the fall was unjustified (though you still need to take care as just because a report is false, it doesn’t mean it can’t hurt the company). It wasn’t just idle speculation on my part, a friend who was in the IT security arena spotted the exact same thing and bought at the same time.

What’s more, the company was quite small so not maybe institutional buyers were watching this and even if they were prevented from buying because SMCI had failed to file account on time and so had been de-listed and so fell out of their universe of investible stocks. The private investor had no such limits and could buy the stocks OTC so you also had an illilquidity discount.

If you had the accounting knowledge, you’d have known the reasons for the delay were no cause for concern. On top of that SMCI had long secular tail winds with datacentre refresh ahead (around the same time I was also buying AMD on the fact that they were going to take significant market share from Intel).

So with all these positive factors you’d think that investors would be piling in, but prices remained depressed until 2019.

Maybe ‘smart investors’ like Buffett could have bought? No, it’s not in his wheelhouse and even if it was, the company is too small for him to invest in without creating liquidity issues.

I’d even bought for my girlfriend’s account at a 60% premium to the price I’d bought for. She recently sold it all for a 14x return.

This is absolutely and utterly wrong!

Sorry if I have offended you… That was not my intent.

Some thoughts to your points:

To follow up on your older post:

Which shows Real Estate is under 3% sector weighting.

Yes, that’s because the MSCI US Broad Market Index is a stock market index. So its composition reflects economic activity. But in terms of global assets, Real estate makes up 68%, according to McKinsey.

Why profit only off the stocks, when such a large fraction of the assets are there for investment, too?

I’m not at all offended. I hear this line all the time and I think it is wrong and self-defeating to believe you have lost before you have started.

But even those who think long term are at the mercy of their investors and forced to index hug. I think the only ones immune are maybe PE where funds are permanently locked up.

And like I said, you can pick your own arena by moving to smaller caps where the big boys can’t play. Or invest in frontiers where you have more expertise e.g. semi-conductors.

While I’m sure Munger and Buffett are great investors, I suspect a good 28 year old investor would probably be better able to understand the investment environment around TikTok for example.

I’m talking about holding onto winning positions, if you can’t even hold onto your winners, then you already have a huge disadvantage.

e.g. only invest in US companies, or with market cap >$xm. Or in the example I gave above where institutional investors were not able to invest in SMCI because it was de-listed.

Data is everywhere. Knowledge and understanding is another matter.

I hear this line all the time and I think it is wrong and self-defeating to believe you have lost before you have started.

I think it’s a waste of time to put in a lot of work when the chances of success are small. But prove me wrong.

I’m talking about holding onto winning positions, if you can’t even hold onto your winners, then you already have a huge disadvantage.

The problem is, which ones are the winning positions? You never know beforehand. You might just as well be holding onto a losing position. In hindsight it’s always easy to tell.

But I’m curious about your SMCI example. Could you follow up on that move on other occasions? How many such trades have you made? What is your net gain over all those trades? Because if your claim is correct, you should have been able to, and made a substantial profit. If not, I’ll take your example as a lucky punch…

My biggest/highest conviction trades so far were:

Generally, my approach has been to:

So how did I do? I managed a 7 figure return in the last 7 years or so. That’s in spite of all the rookie mistakes I made and includes close to a 7 figure write-off on Russian stocks (which I hope I manage to recover something from eventually).

I wish I started much earlier so I had the last 7 years of experience and more time to build. I’m still learning.

Thanks for sharing. 7 figure returns do not contain much information. Could be short-term government bonds on 9 figure capital, could be crypto CFD’s from near zero (figuratively, since you showcased your strategy). Do have a TWR on your net worth?

Unfortunately, I don’t - though I guess starting at 200k 7 years ago and adding monthly from salary gives a broad idea (I also had some withdrawals to fund a house purchase).

I had transfers from brokerages with messed up basis and haven’t gone to do the fix-ups and analysis because ultimately I don’t care.

The status of my portfolio is pulled together with a custom script and even that does not calculate gain or loss on open positions, only the status - as I deliberately don’t want to have any anchoring bias.

The only ‘performance’ figure it calculates is the absolute gain from around 2017/2018 when I wrote the script to the current day value.

I tried to do a comparison vs SP500 using this:

And came above the return there. But of course, this means nothing. The performance over only 7 years is way too short to draw any conclusions from.

Ultimately, I don’t want to actively manage forever and so will need to transition to (most likely) low cost tracker ETFs at some point.