I have been recently testing radicant in North Macedonia. I was curious how it’s gonna work with such a niche currency as Macedonian denars. And tbh - I have mixed feelings.

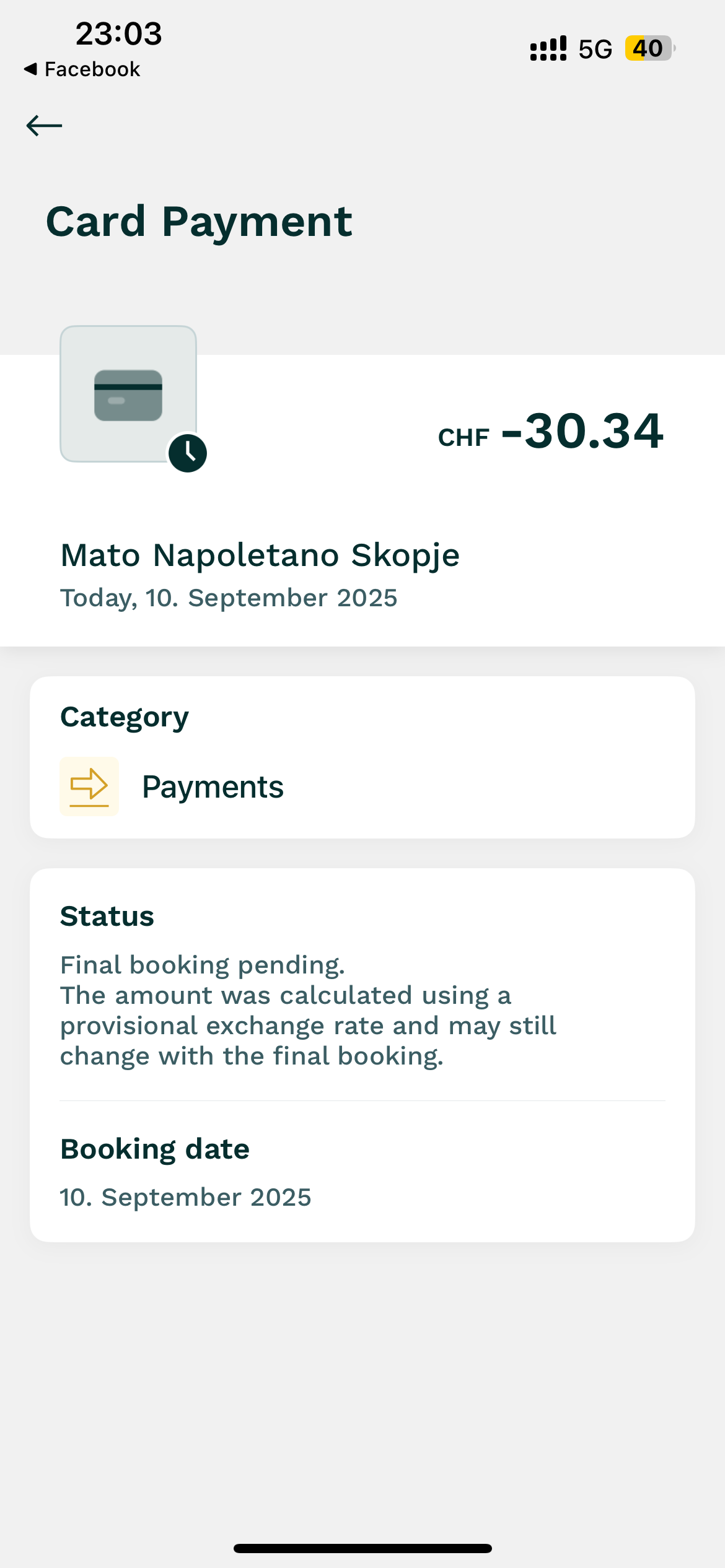

Initially, it looked pretty promising - here’s a transaction from 10.09:

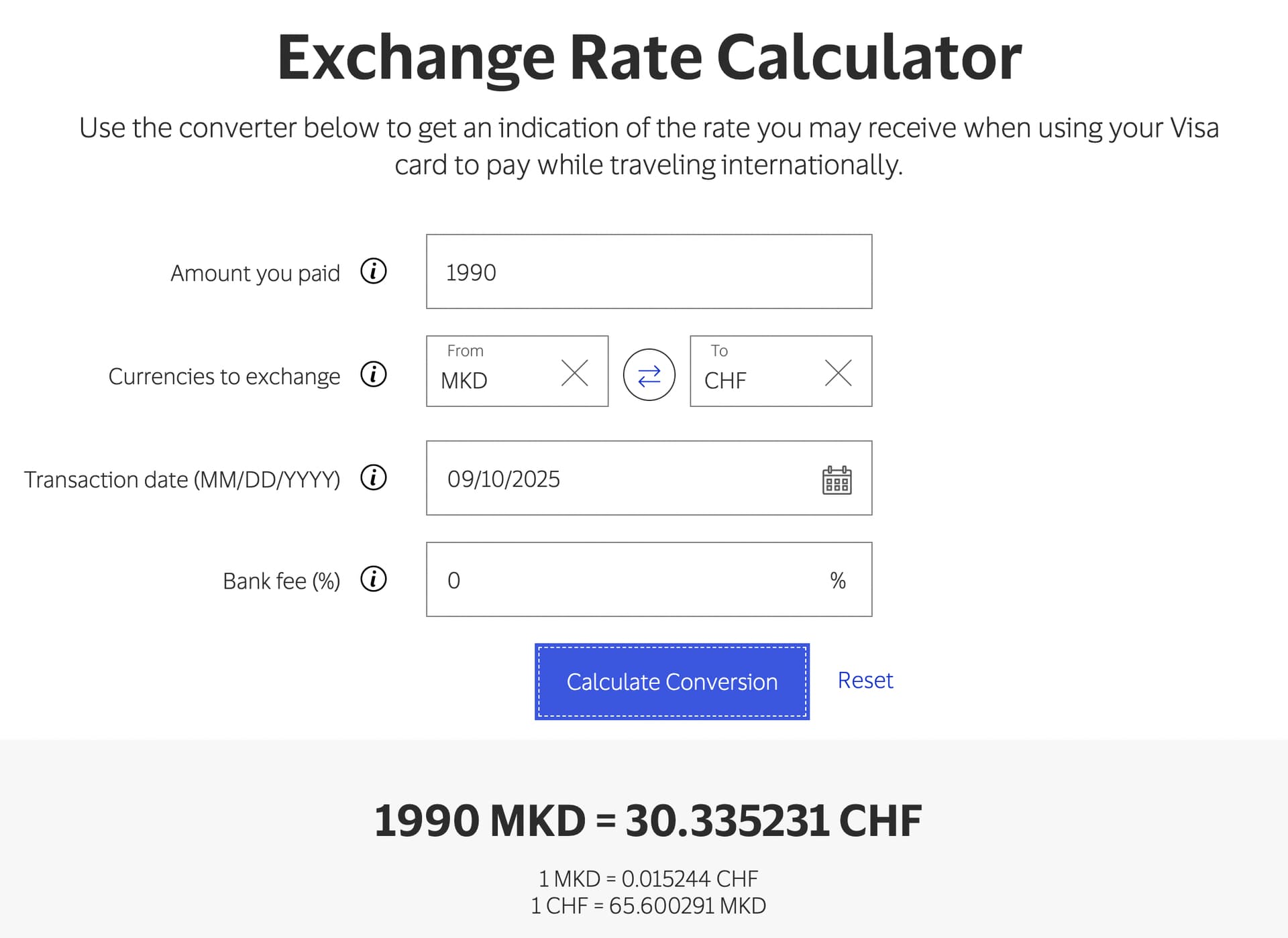

so it’s more than 0.60% above the initially booked amount / the amount in the Visa calculator. Of course - it’s still not a big deal, but it’s significantly higher than 0.1% calculated by Moneyland.

I wanted to understand the reason behind this, so I contacted radicant support, but their answer was quite vague:

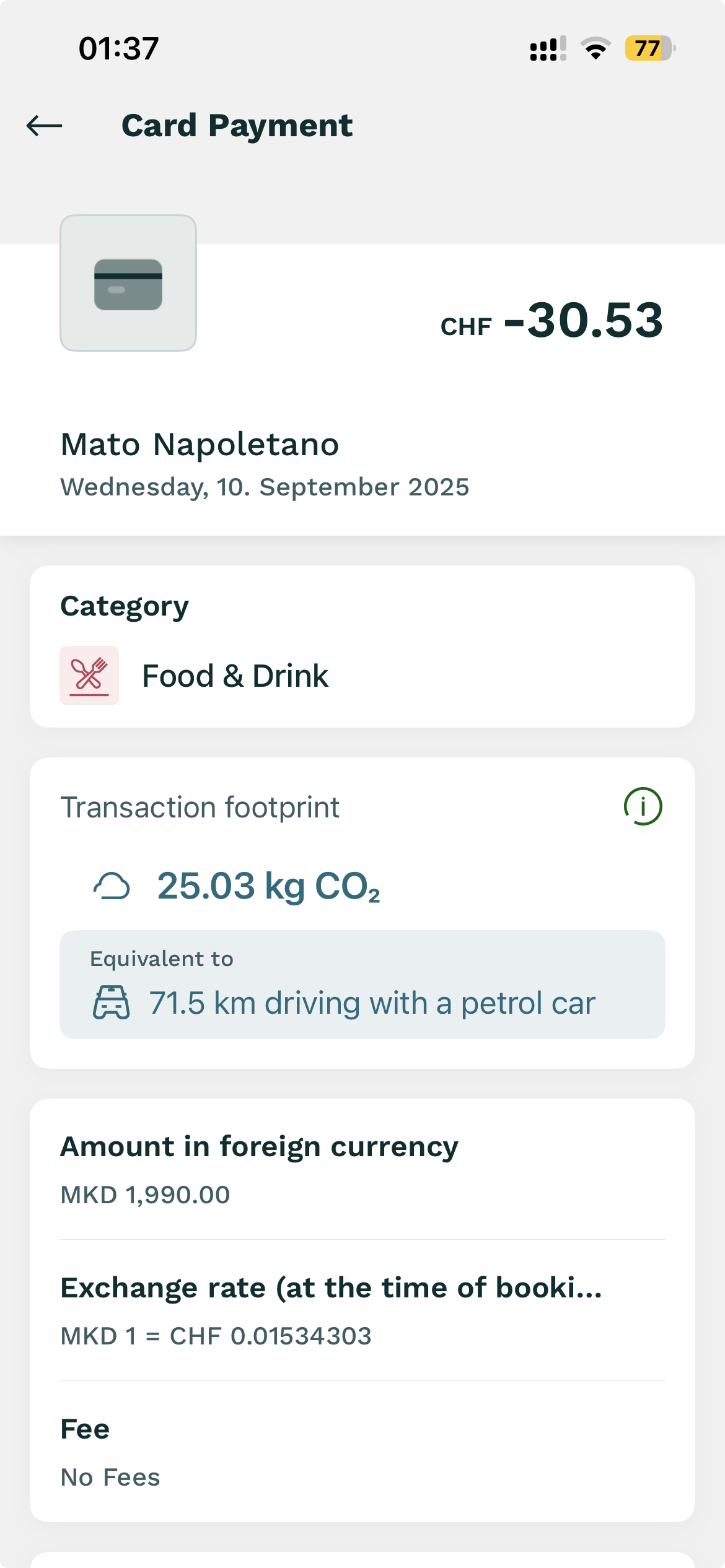

In that case - the actual markup is even higher: ~0.77%.

When I used Neon, before they introduced currency conversion fees for free accounts, final amounts matched the Mastercard calculator. So it’s a bit disappointing radicant is less transparent and it’s hard to understand what’s the actual source of FX rate they use.

PS Another annoying thing I noticed during the trip was that radicant messes up the order of transactions. They are not sorted by transaction time, but by booking time, which makes it difficult to keep track of transactions for a given day as they are in a completely random order.

radicant claims they use “interbank rate without additional fees”, so their FX rate should be better than both Visa and Mastercard rates, but it was noticeably worse

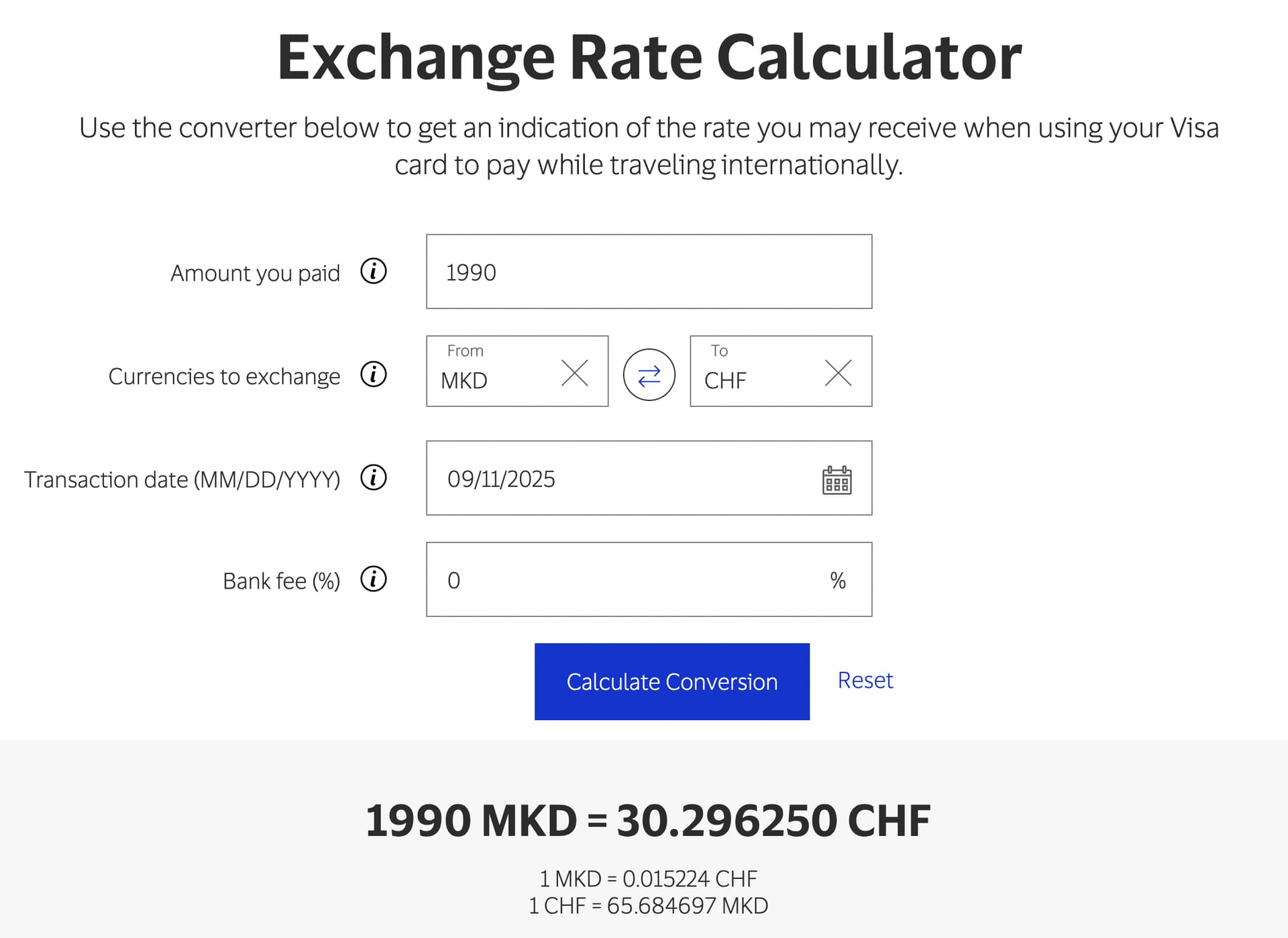

I think something to take into consideration is that Radicant don’t use the FX rate the day/hour/minute when you paid, but when the transaction is effective, and usually it’s calculated one day after (or even after week-end if transaction was on Friday). In this case it could explain why it is uncorrelated to Visa FX the same day. Try to compare one day later. Maybe..

Does anyone know what happens if they close?

I have a 100k parked there waiting for a RE purchase, which, fingers crossed, should happen next month or the following.

I assume they would ask for an IBAN to transfer the money, but I don’t want to risk having the money blocked at the wrong time.

I wonder if I should pre-emptively move it just in case? Plan was to most likely close the account after the purchase.

(Based on the figures floating in the thread, I realise I have a worryingly not that insignificant % of their total AUM, like 0.1%.)

Well, I either need to move it to an existing account and go over the 100k insured limit, or I need to open a new account at a new bank. And I’m already using a couple more banks for each other 100k tranche I’m parking.

Amounts below 100k should stay liquid I assume. Also they won’t close, if something happen their customers will be absorbed by another bank most likely (I’m sure neon or yuh would be ok).

If too many people decide on moving cash out (constituting a bank run), the bank will become illiquid and will have to impose a limit on cash-outs. Eventually, they can liquidate additional assets or call back loans to pay out to all clients. Only if they have to declare bankruptcy, the insurance will pay out a maximum of 100k per customer. But at the moment, they’re still looking for a buyer, meaning there are still valuable customers and assets in the bank.

A big bank buys because of tech stack or customers

Radicant closes down, customers must leave

Radicant closes down, customers migrated to BLKB

I think for Neon, Yuh, etc., a purchase is not interesting. They already have everything, and some customers are going to switch to them anyway when Radicant closes.

The client base of radicant is not that interesting; the did a LOT of promos (especially through 20min.ch, preispirat.ch and other (bargain hunter) websites, and I read somewhere of low volume of assets per client.

Therefore interesting to see which option will be the final one.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.