OMG you are right. I’m so sorry to all Yuh fans. That issue belongs 100% to Neon. Or better to the bank behind them.

2 Likes

I’ve started using Radicant, is there a way to receive push notifications when payments are made (online and in a physical store)?

For the small tests that I’ve done I’m not receiving them, and it’s a bit annoying.

I tried to look for a setting in the app, but I can’t find anything apart from “push notification for 3-D Secure”.

They released an update today announcing push notifications for card payments.

2 Likes

What’s currently the best coupon code when opening a radicant account?

2 Likes

Another question: is there a way to put aside some money each month into some kind of separate bucket, like you can with neon or Yuh? I haven’t found anything on their website…

No, There is no such feature in Radicant.

1 Like

Not the buckets feature, but at least a second account is on the roadmap now and upcoming:

After the fee changes in Neon, I am looking if it make sense to open and account in Radicant. what catch my eye are:

- No fees abroad

- ATM withdrawals for free

- and the free insurance

anyone ever had to use to insurance?

if anyone has an invite code or anything that gives me some benefit, I will be happy to be invited.

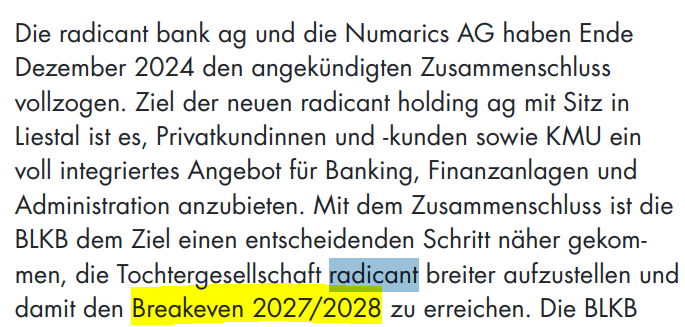

They might have to pivot a bit more before they hit the sweet spot. After trying sustainable investing solutions, they purchased an accounting firm and are now hoping to reach break-even in 2027/2028, while being owned by and tucked away in the balance sheet of Basellandschaftliche Kantonalbank.

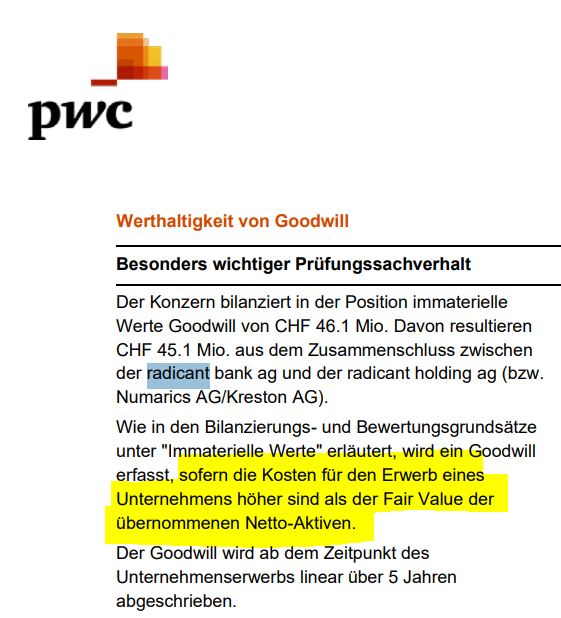

It looks like the revision company PWC does not believe that Numarics is worth the purchase value

I don’t know how the separate banking license works for Radicant, should BLKB Bankrat loose their patience and cut all ties.

Looking at the screenshots on their website, there’s some kind of CO2 value shown with each entry in the transaction list. Is that something that can be disabled?

I haven’t seen a setting for it, but it’s not really disruptive either.

1 Like

That question,

3 Likes

No, but it clutters up the interface for a… to avoid turning this into a political discussion let’s call it limited benefit ![]() When they list a value for my Coop purchase, they don’t know if I bought Argentinian beef or Swiss oatmeal, so the values are misleading.

When they list a value for my Coop purchase, they don’t know if I bought Argentinian beef or Swiss oatmeal, so the values are misleading.

I’m a stickler for things like a clean UI.

At least the interface is (still) quieter than Revolut and Yuh. Revolut keeps pretending there’s something important, and then it’s just another “Invite your friends and earn $80” message that shows up about once a month and Yuh sends you push message if you don’t use the card.

This is probably why I find the Radicant app uncluttered and almost boring.

But I know what you mean ![]()

1 Like

There’s no perfect solution, correct. Uncluttered and boring is how I like my banking apps, so might give it a try.

Their FAQ has an entry for exactly my question, but they mistakenly pasted the answer to a different question.

Let’s see what that means for the marvelous FX card conditions ![]()

1 Like

“„Die BLKB hält an ihrem strategischen Investment radicant fest“, versuchen die Chefs zu beschwichtigen.”

![]()

This is shaping up to be one of the biggest failures we’ve seen. Most people are willing to pay for a service - if it offers real value. As it stands, Radicant’s only clear advantage is handling foreign payments.

How much does the average user actually spend on foreign exchange per year? CHF 5’000? Maybe CHF 10’000?

With just over 10’000 clients by the end of 2024 and CHF 80 million in assets, that’s less than CHF 8’000 per client. How exactly is this supposed to become a sustainable business?

Have a look at neon: was anyone surprised that they had to introduce fees? At least - in my personal opinion - this story will last longer than Radicant’s.

Here an in-depth article in German on Radicant with some comparisons to other neo banks.

Summary

Due to “differing visions,” Radicant CEO Anton Stadelmann is leaving the neo-bank. The departure highlights the ongoing struggles of Radicant, which has faced significant political pressure and criticism from the canton of Basel-Landschaft over high investments. The future of the bank, created by the Basellandschaftliche Kantonalbank (BLKB), is now uncertain. The article suggests that Radicant may be integrated into its parent company, the BLKB, or sold off, marking an end to the neo-bank in its current form.

5 Likes

4 posts were merged into an existing topic: Financial setup for foreign currency exchange and payment [2025]