these happened to be spread among 4 different exchanges (EPA, AMS, SWX, BIT) - is that okay or should I pick one and stick to it?

the ETFs are issued by at least three different entities (iShares, SPDR, AMUNDI) - is that okay or should I pick one and stick to it?

0 contributions to 3rd pillar because I’m unsure where I’ll be in 3-5-7 years and not sure how to deal with taxes (have to file taxes before gain any benefits), should I change this?

anything else?

A bit about me: 30, would like to be FI in 15 to 20 years (45-50), currently contributing about 50% of net income, overwhelmed with the amount of information out there and worried that am making some stupid mistakes that am not seeing right now which will bite me in the future.

It’s a never ending loop with this “rate my portfolio”. What are you trying to achieve with it? How is it better than VWRL? If you ask Warren Buffet he will advise you to simply buy S&P 500. So do you think you’re smarter than him or that anybody else on this forum is?

I tend to agree with @Bojack, your question is rather generic maybe you could elaborate on the rationale behind your portfolio, what do you try to achieve and why did you choose this specific allocation.

How about you tell us why you came up with this, instead of something simple like VWRL.

You might have genuine reason to invest in IE-based ETFs instead of the generally cheaper and more tax efficient US-based ETFs, but how can we know? Are you going to relocate to an EU country in the near future?

Why don’t you have Japan? Japan is awesome. The BOJ (national bank of Japan) probably must keep buying stocks to avoid the implosion of their retirement fund. Even if it doesn’t, they have good companies. You can trust me. I drive a Japanese car, have a Japanise TV … and a Nintendo.

Is your broker really so cheap to make it more efficient to buy and rebalance 5 different ETFs instead of 1 just to lower the effective TER?

I can’t really comment on your exact choice of ETFs, but you should consider their AUM and the exchange as it may concern spreads and liquidity. This, again, may be more important than TER when it comes to total costs.

The only remaining question I have - why don’t you invest in VT through IB?

I get where you’re coming from but I really don’t have anything else to add to my initial message where

I said that I:

am overwhelmed with the amount of information out there

don’t have an idea whether what I’m doing is right or not

am afraid that I’m doing something stupid that could’ve been prevented

Because I picked DeGiro (because it seemed cheaper) which doesn’t have them. I suppose that was a mistake because this choice doesn’t seem to be very popular here. I also read different blog posts, for example this one where it seemed important to look at the fund size, TER, make sure the ISIN was listed at ICTax with several more things and everything I listed does satisfy that. I’ve also read at several different places that Ireland was actually a good choice for CH residents for tax reasons .

I don’t know, I am not planning but what if I do? Will I have to sell everything? Or will I simply not able to buy anymore?

As in “only in VT instead of everything listed here”? Or as in “why not also add VT to the list”? I assume it’s the first one since it covers everything already. But then the VWRL was mentioned in almost every reply and since I don’t completely understand the difference between them (except one includes small cap and the other doesn’t but what does that mean in the long term?) I don’t really have an answer.

–

I suppose I still don’t have a clear picture of what’s going on (after at least two months of looking into this) and need to reevaluate things (this is what I meant about being afraid making some silly mistakes, especially since I already contributed several months worth of income into this portfolio).

For Switzeland, the most cost effective and tax effective solution is to invest in US-based funds due to generally lower trading costs and available tax trieties.

If you are in the EU, then you have no other choice as EU made it impossible to buy US-based ETFs.

The VWRL on EAM exchange is comission-free to purchase once a month in Degiro so it is the best choice to start with if you want to stay with Degiro.

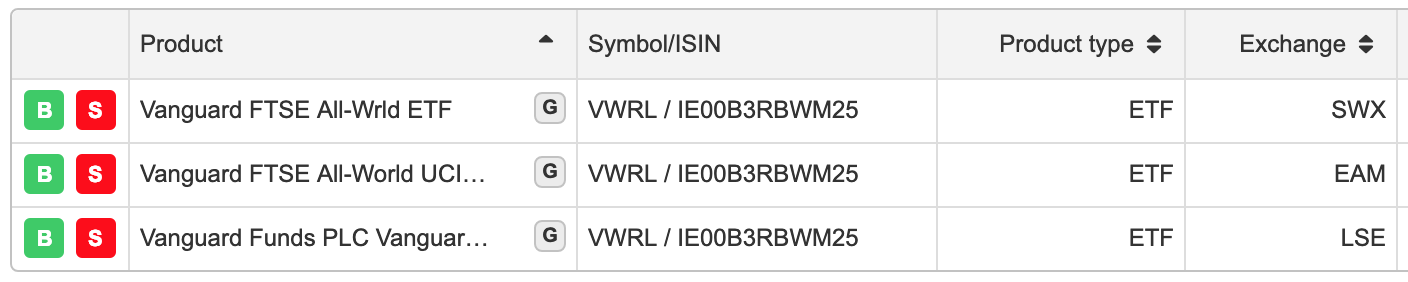

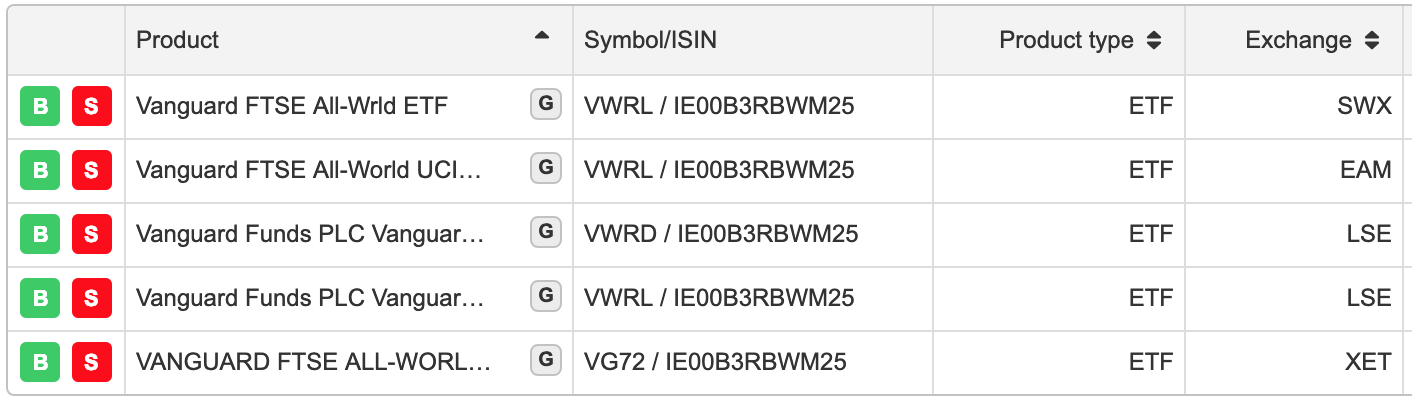

SWX: traded in CHF in Zurich

EAM: traded in EUR in Amsterdam

LSE (VWRD): traded in USD in London

LSE (VWRL): traded in GBP in London

XET: traded in EUR in Frankfurt

To be honest I work with a quite similar portfolio but mostly from Vanguard.

The difference is that I have a position in Japan which is an important capitalisation by itself.

For me, the 0 contribution to 3rd pillar is a good solution due to your young age, the high fees of third pillar and the fact that capital gain is not taxed in Switzerland but is taxed when you take out your third pillar.

The withdrawal tax is 5% to 15% according to amount and canton but there is no capital gain on regular investment. A good part of the gain of a third pillar portfolio comes from capital gain and you will pay the 15% withdrawal tax on it while in your regular portfolio it is tax free.

You have to be honest, the third pillar helps more the bank than the small investor. This sector of the market is not exposed to the competition of foreign bank institution.

OK, but I checked, and if I purchased any 3a pillar in 2018, my taxes would have been lower by 2350 CHF. I was thinking about finally buying VIAC this year, when they roll out the web access. When you invest in a 3a pillar, then all your dividends are income tax free and reinvested automatically. This can offset the 0.5% annual fee. So you have this initial 33% saving bundled with a final 15% withdrawal tax. So you’re better off investing in it either way, or?

IMO this 3a thing must be split into 2 separate (orthogonal) concerns:

tax savings when paying into 3a

how/whether to invest once the money is in 3a or if it’s better to invest outside 3a

So regarding 1.: I think that’s dependent on each person’s tax situation but obviously in many cases there are huge gains to be achieved - as you pointed out in your 2350.- example. So if you’re fine with this money being locked until you retire, build a house or leave Switzerland then that’s a great idea.

Regarding 2.: I just did a calculation yesterday here for a sample situation and the result for those numbers where: investing in 3a mutual funds/etfs has a tax advantage of 0.2% vs investing outside 3a in etfs. So, based on the chosen example numbers at least, dividend gain does not offset 0.5%, only 0.2%.

With that in mind (and yes, everybody’s numbers are slightly different, so everybody must calculate this themselves) I conclude: it is better to (a) pay into 3a to get the tax benefit but (b) keep just cash there and instead invest with what’s still outside of 3a. That is, for the amount of cash I want to keep as cash based on an overall (3a + outside-3a) portfolio view. So really, look at how much you want to invest in total, how much have emergency cash. Then keep a very minimalistic amount of cash outside of 3a (eg 5000) but invest everything else outside of 3a. If you want more emergency cash, keep that non-invested in 3a. And in case of an emergency do the investment-jugggle-trick I mentioned in the other thread

VIAC is the answer. You can create several portfolio which is key when withdrawing them in the future, as the withdrawal tax increases with the amount, better to have 5x30KCHF than 1x150KCHF. This was suggested by my Tax advisor too.

Quick thoughts:

That‘s two thirds (65%) allocated to one single country, the US, which only represents a 330 Mio. population. Sure, it‘s the biggest country in terms of GDP and market capitalisation, and (especially it large-cap) companies might operate globally. It‘s still a lot.

More baffling to me is the of MSCI Pacific ex-Japan, to be honest: Two-thirds of it (65%) are made up of Australia and Singapore alone. So these two countries represent 2/3 * 15% = 10% of your entire portfolio. To quickly it into perspective, in rough numbers:

Australia & Singapore: 30 mio. population, 1.7 trillion $ GDP = 10% of your portfolio

Japan (as already mentioned): 126 mio. population, 5 trillion $ GDP = zero % of your portfolio

What about Europe?

Eurozone: 315 mio. population, 13 trillion $ GDP = 10% of your portfolio

…and then, the EuroStoxx only comprises Eurozone countries, so there‘s the total (if we aren’t getting into technicalities of Unilever) lack of the United Kingdom:

United Kingdom: 66 mio. population, 2.9 trillion $ GDP = zero % of your portfolio

What about China? The mainland constitutes app. one third of MSCI Emerging Markets, and Hong Kong one third of MSCI pacific:

China: 1400 mio. population, 13.5 trillion $ GDP = 8% of your portfolio

There might be reasons to do this, but it certainly seems a disproportionately high, even huge bet on Australia and Singapore, compared to other markets.

I would like to highlight that GDP is not linked to market capitalization.

I like the idea to avoid Japan, however, I agree that 15% in Asia Pacific is too much.

Maybe it would be easier to simply buy an ACWI or FTSE all world ETF (VT from Vanguard)

I would also advise US-based ETF to reduce the withholding tax.

AMUNDI MSCI EM DR could be replaced with the Ishare fund with a TER of 0.18%

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.