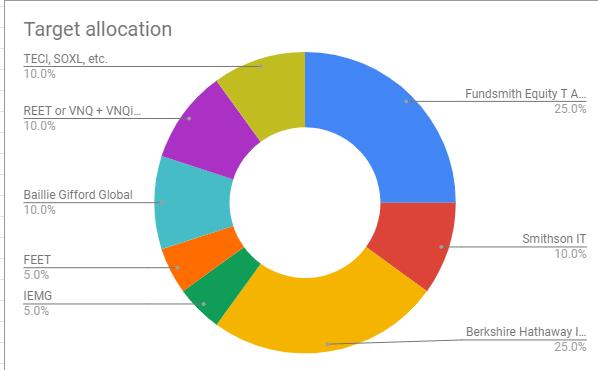

Berkshire and Fundsmith are actively managed and they promise to beat the market, so a higher TER is justified. the question is if they can deliver. I guess your portfolio idea comes from the English Forum, where Fundsmith is strongly advertised by the user “Fatmanfilms” . I personally am too afraid to invest in an actively managed fund. Even if Fundsmith sounds wonderful on paper. But that’s my personal feeling, not backed by any research.

You can have a less defensive portofolio by adding small cap and EM. (Real estate is more defensive than offensive)

My portfolio, as I’m quite young with a long investment horizon, is 40% EM, 30% VT and 30% VBR. Europe and Asia are covered in my 3a

you guessed right on Fundsmith and fmf “advertisement”. So far (8 years) I am more than happy with the returns.

But the rest comes from my own research. Berkshire I see as a 0 TER us fund focused on financials, infrastructure and insurance, sectors which Fundsmith does not cover.

BTW: neither BRK, nor Funsmith do promise to beat the market.

15 years is very short - and will feel much shorter than the previous 15.

So time is to consider being more defensive.

Finally you don’t want your portfolio being toasted during these 15 years (and the years after too), right?

Ah, OK.

So the strategy is to be aggressive as long it is “minimum 15 years”, then to be defensive with what remains of the portfolio when it turns into “maximum 15 years” ?

So as I see it, you’re basically placing almost all your wealth in hands of two admiteddly very talented individuals - Warren Buffet and Terry Smith. Have you considered the posible ripple in your investments in case of their death or some fraud/scandal related to these funds? A single company can easily lose more than 50% in a day. Don’t underestimate that risk.

I don’t hold too tightly to the idea of indexing but index funds will always be a minimum 60% of my stock portfolio.

I’d also argue you’d have as much return as Fundsmith with a plain MSCI World Momentum ETF, the latter being way easier to buy, cheaper to hold, more liquid and more tax effective.

Then your play money. 10% in Crypto, Leveraged ETFs etc. Assuming these are, as some say, a losing game, you are looking at recurrent lossess and recurrent rebalancing of your remaining portfolio to compensate for these losses. My tip : keep play money separate from your long term retirement portfolio, but by all means use any winning positions to fund your main portfolio at its fixed proportions.

With respect to individual/ fund risk: I will definitely consider this. I might go with other funds for small caps and emerging markets to limit my risk exposure to Terry Smith. I am not too worried about Berkshire. The “retirement” of Warren Buffet will at most be a good buying opportunity as I am sure the successor(s) are already doing most of the work anyhow.

All-in-all, I am not a big fan of index tracking as it is buy high, sell-low.

Play money: good observation: Actually my play money is 10% of my current portfolio and I do not plan to add more money there. Like in a casino: I have a fixed amount and when I run out of money, I leave.

My prediction is you will underperform S&P 500 with this strategy. If this is ok for you due to risk considerations then that’s fine. But it is hard to beat SPX

I see a logical flaw here, or perhaps you haven’t really considered rebalancing as of now. For many here, it’s of utmost importance to stick to the plan, or “stay the course” as late John Bogle would say.

You decide on an allocation (say 90% global stocks, 10% cash) and rebalance once or twice a year to keep these proportions in tact. It’s a proven way to long term success.

With 10% allocated in play money you should cash in any wins and allocate into other assets at predefined intervals and proportions, but also cover the losess by selling other assets in order to keep your predefined allocation of 10% play money. Otherwise your chart in the title post simply makes no sense.

In that case you should count that 10% as already gone and not count it as your portfolio, at least not as a fixed part. And of course you should never fund your play pot with extra money, that would be dangerous.

Including the 10% in the portfolio or not is purely psychological. From a mustachian perspective every single CHF in any bank account should be considered part of the portfolio. Allocating 10% of all funds to something else and then not outperforming the main investment vehicles will lead to underperformance of the entire portfolio

What confuses me often when I see these kinds of posts here is why people emphasize so much on the asset allocation. The intent is quite simply to try to outperform the indexes which science has proven is very difficult

The only acceptable deviation from a 100% Low TER index fund portfolio should be risk considerations

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

?

?