Déjà, je tenais à préciser que suis novice dans le domaine bancaire.

Voilà, j’ai décidé de résilier ma police 3A Swiss Life Dynamic Elements Duo ( 75% actions) ouverte en 2021 avec perte estimée à 8000.-

J’aimerais transférer la valeur de rachat sur une police 3A de chez VZ ( 50% actions) car ils proposent aussi des conseils fiscaux et étant novice dans le domaine, je trouve ça intéressant.

J’hésite toutefois à ouvrir une police chez VIAC ( aussi 50/50).

L’âge de ma retraite est prévue ds 30 ans.

L’idée est de continuer à verser 7056.- annuels

Qu’en pensez vous ? Quels sont les avantages et inconvénients d’un pilier chez VZ et chez VIAC ?

Merci d’avance pour votre aide.

C’est plus cher sans plus-value (les fameux « non » conseil fiscaux). Le pilier 3a ne peut être retirer avant 60 ans au plus tôt, à moins de l’utiliser pour vous lancer dans l’indépendance ou pour l’achat d’un bien immobilier.

Donc en soi, une fois mis en place, il n’y a pas de conseil à avoir en plus…

My native language is not French, but if I understood you correctly, you are looking for a pillar 3a solution with 50% stocks and 50% fixed income (cash or bonds). You are coming from some Swiss Life mixed life insurance and investment product (those are nearly always a scam).

You try to educate yourself on your financial affairs. Congratulations, doing so is the best investment you will ever make.

As you know few, the improvements will be large, clear and easy to reach. But beware of scams. If something is too good to be true, it probably isn’t.

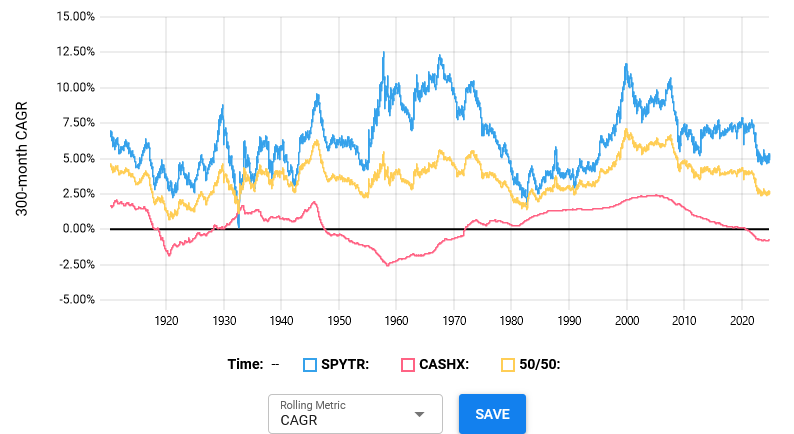

If you have an investment horizon of 30 years, 50% fixed income seems too conservative. Just to put things into perspective: Over any 25 years since 1885-03-20, the 500 biggest US companies (blue) have returned more than US inflation. The same can’t be said about USD cash (red). And only for 4 months during the great depression were cash or 50/50 slightly better:

But if you don’t want to hold cash (but bonds, or more stocks), then VIAC (or VZ) clearly doesn’t beat Finpension in cost. Truewealth has even lower fees for now (0% management + any fund TERs). But this doesn’t pay for itself, so they might end it at any time.

I think Finpension has the best offer on the market. Try to find out why that could be or pay some advisor to help you. But as with life insurance: Don’t buy intransparent services. Separate the components. Pay someone to give advice only, but don’t let them sell you their own products, or attach their name to a deal.

Edit: Ceci a été déplacé vers café francophone, veuillez utiliser un traducteur, si la lecture de l’anglais est difficile.

This is very much not a solved problem in Switzerland. Others were looking for this service and found nothing either:

But you could try VZ, tell them up front:

you won’t to buy any of their products, even if they are potentially better

you won’t let them sell you anything, nor put their name on a deal

you are ready to pay for their time, and come back if it was worth your money

Then make sure:

you have an idea of what you want to know

they explain why something should be done (vs the alternative)

you understand their explanation

you get a second opinion (maybe on this forum)

(give something back by describing your experience if you try this)

In general this forum is somewhat biased towards aggressive but rational accumulation. This is not suitable for everyone. But for learning how things work, and what products exist, it works well enough. In my opinion we still maintain enough diversity, knowledge and culture to challenge all ideas posted here. Scams and wrong information is flushed out, and things are are looked at from many angles, finding the edge cases.

It takes time, but by researching the concepts you read here but don’t understand, you will save a lot on expensive advisors, and even more with making good decisions.

Vous ne trouverez personne qui vous conseillera à ce sujet sans un biais ou sans vous vendre une solution où elle touchera une commission derrière.

Ce forum est une mine d’or d’information, mais cela va dans tous les sens lorsqu’on entre dans ce monde.

Ce que je peux vous conseillez c’est de lire le livre de Marc Pittet ou son blog et de vous faire une opinion propre en définissant vos propres objectifs.

La plupart des personnes sur ce forum sont chez VIAC ou Finpension (actions à 100%). Il y a des exceptions.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.