Indeed, I am happy with my rent. When I arrived in Switzerland, I was lucky that one of my colleagues offered to check if there was some apartment available in his Baugenossenschaft, and luckily it was the case. So i managed to enter into a BG without the usual hassle.

But even if the BG definitely helps, i think that the main factor for the low rent is the low-ish surface (65 sq meter, 2.5 rooms). Even if this is the biggest apartment I ever lived in, most of my friends call it tiny.

Quality is subjective.

In the end you do have to set your expectations.

Apartment: you could do with less than 1000 CHF.

Food: 650 CHF seems relatively high (though I don’t know what “Life” is supposed to mean)

Smartphone: Does that included the cost of the device itself? Otherwise could be halved

Coaching: Out of curiosity… what is meant by that?

Vacation: 6000 CHF a year? Seriously?

If you slash apartment and food/drinking out by a combined 500 CHF each month and vacation budget in half, you should easily be able to save an additional 10k CHF each year. Again, it comes down to what’s “without lowering quality” means and what your preferences are.

I am extremely frugal by nature. My parents are extremely frugal too, but they spared no expense for what they thought was highest quality for them: good education for me & my siblings. The highest quality for me is home cooked food, sitting on a couch and watching documentaries and reading books (other than to travel to places rich in culture, history, and beauty). Most of it costs very little. For my brother, the highest quality is buying new clothes every month (he probably has 50+ shirts) and eating out often. So he spends a lot!

Of course there are a couple of things I could realistically reduce. Others not really, lets summarize.

Apartment: Cheapest 2 room apartment where I live is 1160 CHF with 42qm, lol. Mine is 3 room with 82qm for 1197 CHF, so I actually got a pretty good deal. I could save probably 200 CHF if I moved further out, but I don’t have a car. The longer commute time, the longer time to get to the gym etc. would reduce my quality of life significantly. This is worth way more than the 200 CHF per month I could save. Time generally is the most precious thing in life IMO.

Food: As a competitive powerlifter and someone that weighs 100kg, I need 4000kcal/day. I already cook a lot (always have my tupperware at lunch in my office), but I want quality food, so Migros and Coop for me. Normal people eat 150g of raw Pasta, I eat 300-400g. You can really imagine my eating behaviour as 2 persons.

Smartphone: It’s Wingo for 25 CHF per month plus the device (27.55 CHF per month) that will be paid of in 5 months. I could potentially switch to Salt, but I would pay more because of the roaming options.

Internet: I could ditch the TV option and go from 300Mbits to 100Mbits. But I spend a lot of time on my computer and I like fast internet.

Coaching: For powerlifting, he is from Germany and a very good friend…and a great coach for strength. Usually things like this cost 150-300 CHF per month. 60 Euro is basically nothing for this kind of service.

Healthcare: I have the 300 CHF franchise. Because of my sport (and the level I’m doing it) I need to go to the physio on a regular basis. I run the numbers many times, I’m better of than choosing 2’500 CHF. It paid off in the last 5 years.

Vacation: For me the most important thing about quality of life for me. I know 6’000 CHF per year is pretty high, but I really enjoy going to places like Mexico, Thailand etc. and I like to go snowboarding for a week in winter, that’s expensive too. Despite Corona I did this in 2020: 1.5 weeks snowboarding in Bosnia, 2.5 weeks island-hopping in Thailand and 1 week in Rhodos/Greece.

So I think I optimized what’s possible and worth the optimization. Now I’m focusing on school and career development. I think increasing my base salary from 83k to 120k in a couple of years would make a much bigger difference than the things I mentioned above.

2020 was a bumper year for me because of Covid-19. Work from home meant that my lunch spending had a significant drop. Also, out of a budgeted 7’000 a year for travelling, I spent only 1’000 chf. Luckily, I was able to recoup most of my already booked travels or get a voucher. Additionally, I also got a bump in my income. So, in the end it looks like this:

Projected saving for 2020: 65’000 chf*

Actual savings for 2020: 86’000 chf*

Actual savings as % of gross income: > 50%*

I think that is the way to go and I was at roughly same salary as you not too long ago. Now is the time to really optimize your spending so that you are only spending to improve the quality of your life. As you earn more money, just save (and invest) all of it. My expenses stayed same (or even went down by 10%) even when my income saw a significant growth.

Then there is nothing to reduce, other than your school expenses that will come down once you finish your course. Increasing salary will lift your boat further.

+1 for finding such a cheap apartment.

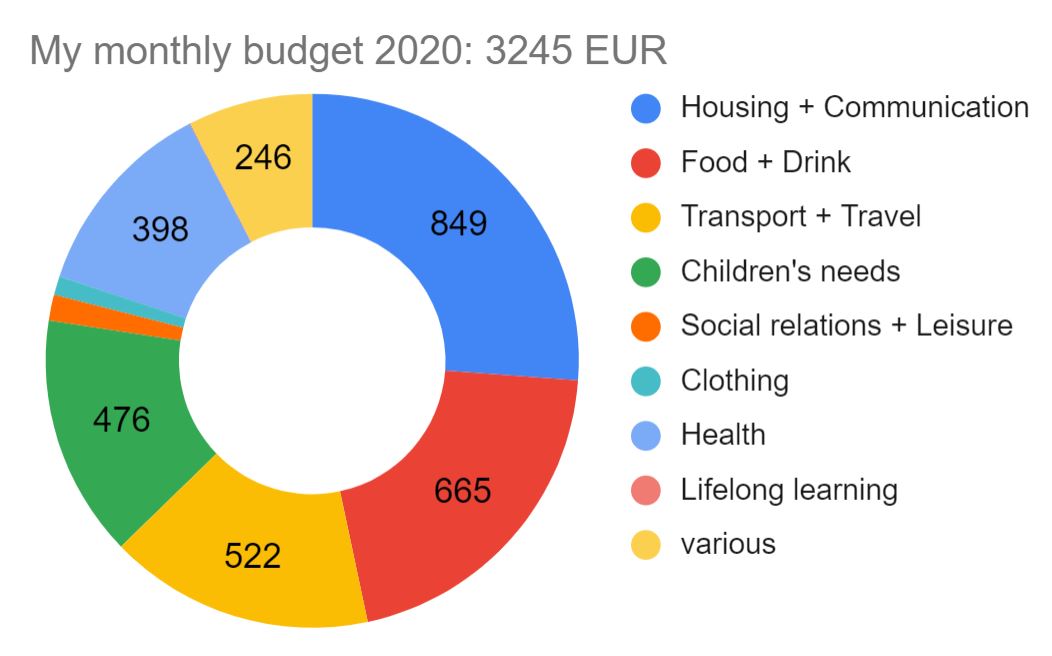

Living in Luxembourg City, I spent 3245 EUR (3500 CHF) per month in 2020, sharing an 85 sqm apartment and car with my gf. My adult son living with his mom got some pocket money during his gap year. Public transport is free in Luxembourg and during Covid I stayed home or used the car. We love to travel, which had to be cut down in 2020. Health insurance is deducted directly from salary and most costs (including dental) are reimbursed.

Another 3250 EUR go to taxes (every month - ouch!). And I have not yet considered the 17% VAT we pay on all our purchases.

Living on a fat budget, I identified 1326 EUR savings potential per month, which would land me below the poverty line for singles as defined by the Luxembourg Statistical bureau: 2014 EUR.

flat share with more people or move to suburbs: -150

avoid alcohol: -150

avoid restaurants: -50

shop at cheaper grocery store (Lidl instead Cactus): -50

I would definitely start with that. Dry January might be a good start to also look if there is a problem. It should be easy to not consume alcohol for a month.

476 Euro per month is a lot of spending money for someone who doesn’t pay rent.

@covfefe spends even less than me, @Julianek and @Goyero also live very frugal and spend less than me per person.

This year was also a bit special, there were no holidays or skiing expenses as the planned Iceland trip in June (~2.5k) was cancelled and skiing this year is just irresponsible in my opinion. Eating out was also much less common.

However I also spent over 1.5k on a new coffee grinder and got a dual boiler machine for 300.

How/why would you even be addressing that?

It doesn’t seem like anything you can really control, or?

Unless buying abroad (e.g. living in CH, buying from Germany and getting it - or the diff - back).

I could personally never go back to this, once out of the uni/internship life and into the working life, especially more so when living with a gf, and it “saving” me just those 150chf/month.

That’s part of the “quality of life” to me that has been mentioned a few times above.

Living near a border allows for efficient geoarbitrage. Plus in RE phase we might be mobile and can choose where we want to live. Cost of living index of course beats looking at the VAT rate, but when talking about tax, it is important to understand that we are taxed at many different points. I like the transparency of the German autorities with their “Steuerspirale”, I have not been able to get this from the Swiss authorities.

Here you’ll get the Swiss statistics. The federal finance administration has many more detailed files on their website (this specific one is IMF standard).

Out of CHF 151bn tax revenue in 2019 for the state (all levels including state owned entities) the biggest ones were:

For some weird reasons I like to track Groceries (eaten at home) differently from stuff eaten while outside of home and in Restaurants. But yeah 24k CHF in total consumption of ingestible things… (well the Groceries also include stuff like laundry detergent and diapers… so not exactly everything ingestible)

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.