Since you cite me directly… are you a friend of @kilyn or something? The two of you would do great in a blind date.

I just commented on this thread because it resonated well with me because I also was at around 160k net worth when I turned 30.

Since you cite me directly… are you a friend of @kilyn or something? The two of you would do great in a blind date.

I just commented on this thread because it resonated well with me because I also was at around 160k net worth when I turned 30.

Would you be willing to share some insights into what you did differently, what you Invested in?

Might move the discussion in a more constructive direction …

I have long underestimated the power of dogs over humans. There are few words to describe what they bring to us, but all I understood at the age of 27 is that they will always be faithful and play an essential role in maintaining the work/life balance. How many times I have been able to solve a problem by walking my dog outside is just amazing!

That’s so true! Especially now in Covid times working from home for 1.5 years now and my wife not being around due to work, the dog really helps me to feel less lonely and reduce stress. I mean what’s better than playing with your dog in the garden and seeing how much fun he has

Nice rule of thumb. It might be worth a separate thread. With more numbers. (at 9am I can barely calculate my age ![]() )

)

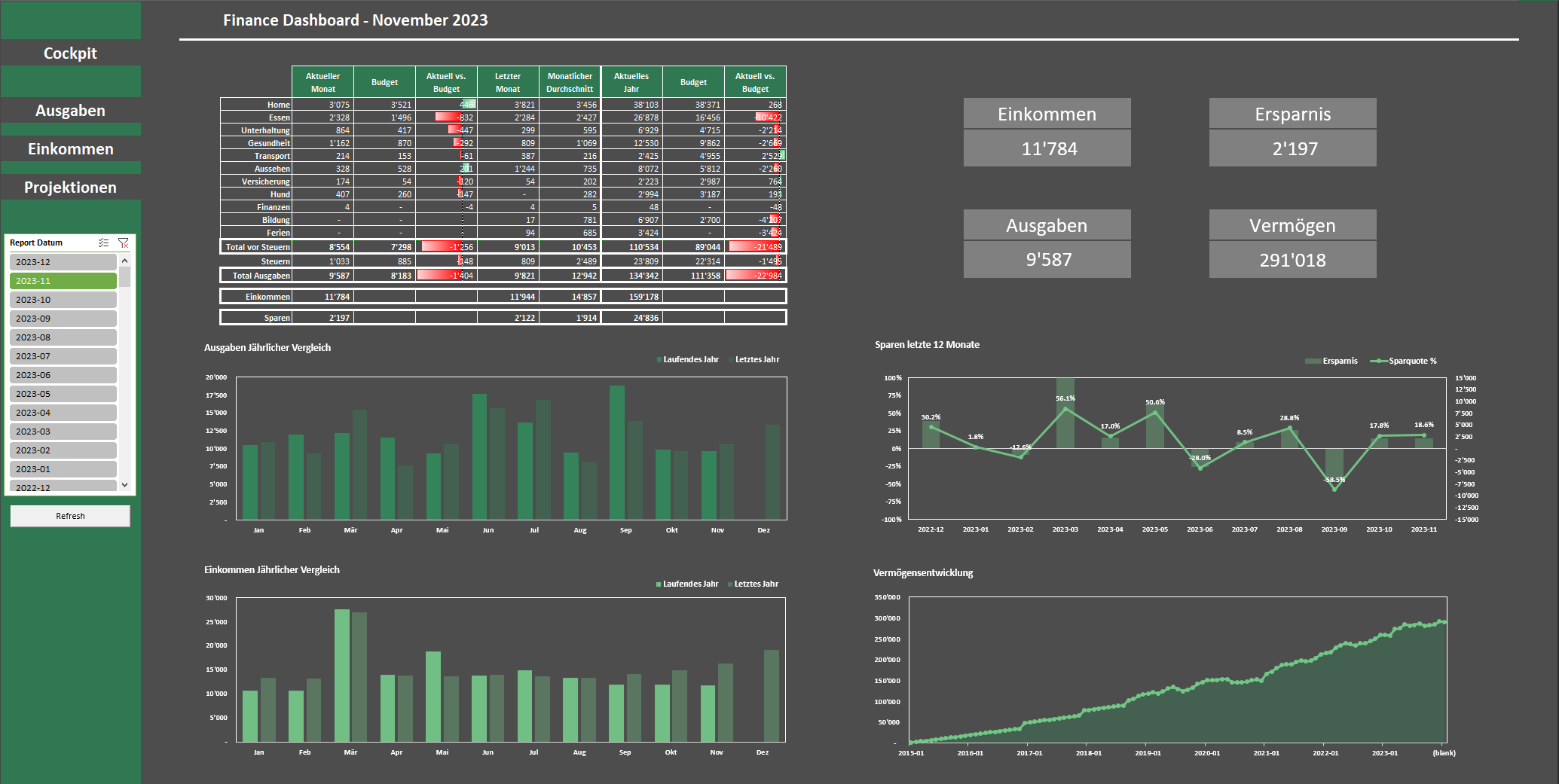

Very interesting read, and in particular how you keep track of your finances.

Where did you find your financial dashboard?

About buying a house, bare in mind this could be the last real estate you invest in, if you were to make that decision.

I personally invest in real estate to generate cash flow and value over time, while still renting my place at a low rent.

Thanks for your feedback!

The dashboards with the performance are made with Portfolio Performance, the last one I made myself in Excel.

The excel sheet looks very pro.

Would you be opened to share it?

I’ve trying to do one myself but can’t seem to have much talent for design…

Thanks, I’ve been working with Excel for quite some time ![]()

I can share the dashboard, however I don’t think it will be of much use for you, it’s specifically designed to handle transactions from beancount. Feel free to send me a PM about this if you are interested anyway.

Thanks @Luk_nuts for reminding me about an update for this post ![]()

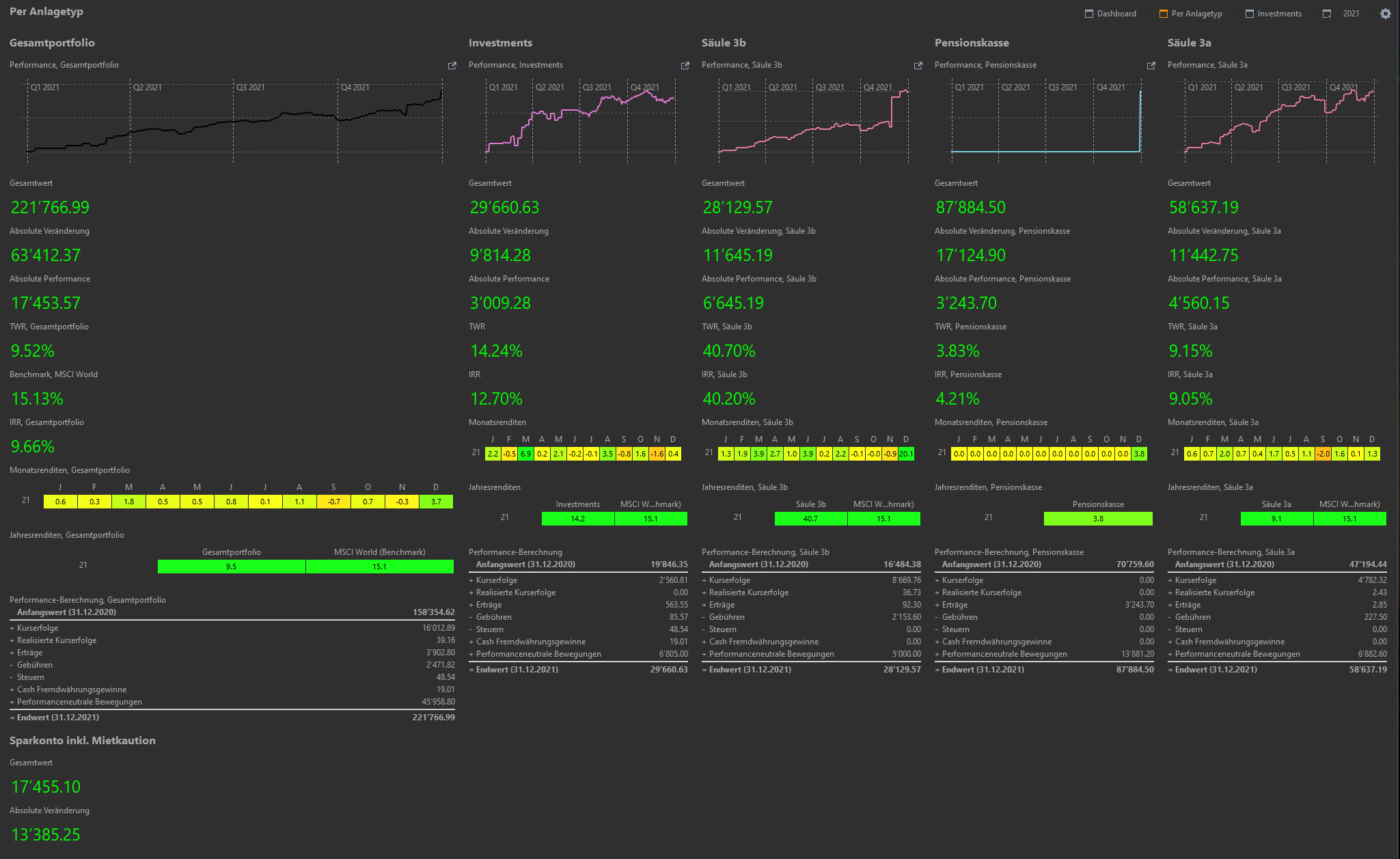

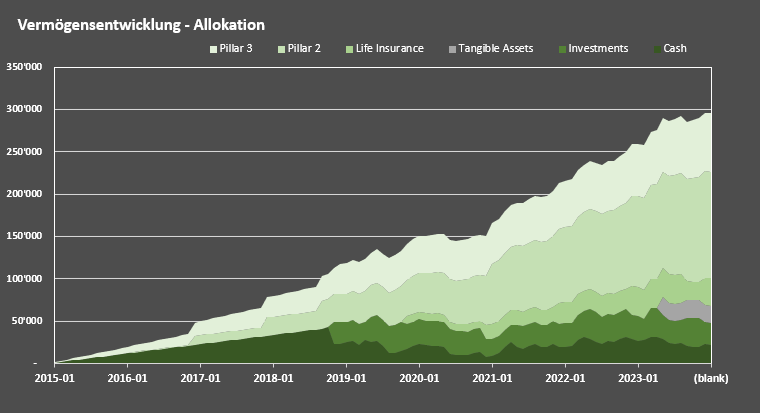

Net Worth Progression and Performance

Still using Portfolio Performance to track my investments.

2021

2021 continued being a good year. I filled up the 3rd pillar and made a nice gain there. I again paid CHF 5’000 to the life insurance of my employer and he topped it up with another CHF 5’000 as usual.

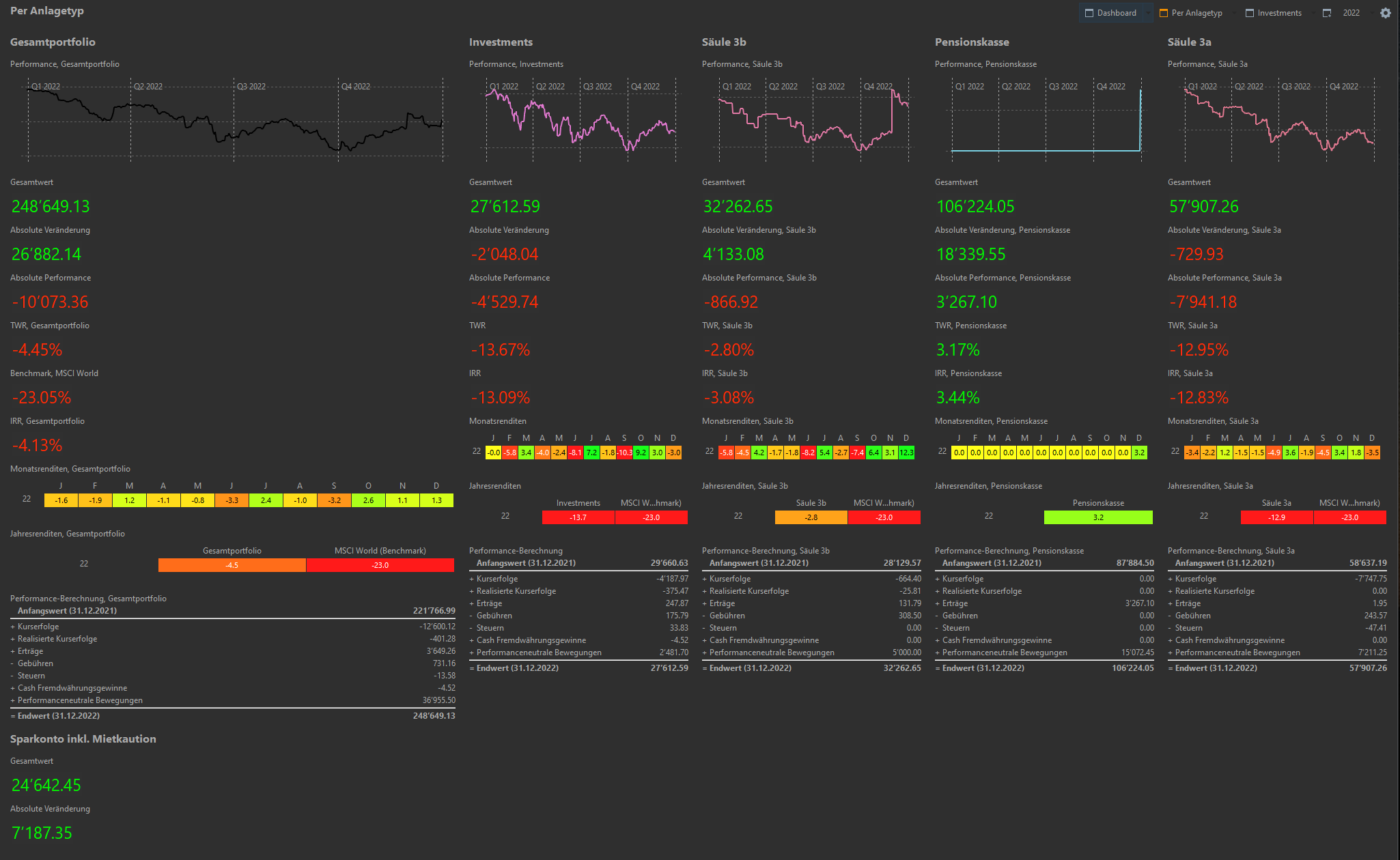

2022

2022 was a bad year performance wise, I “lost” more than CHF 10’000. I moved my investments from VWRL to Fundsmith (FEET) and Smithson (SSON). I again fully paid into the 3rd pillar and life insurance. I became a father in August, so I had some “unexpected” expenses.

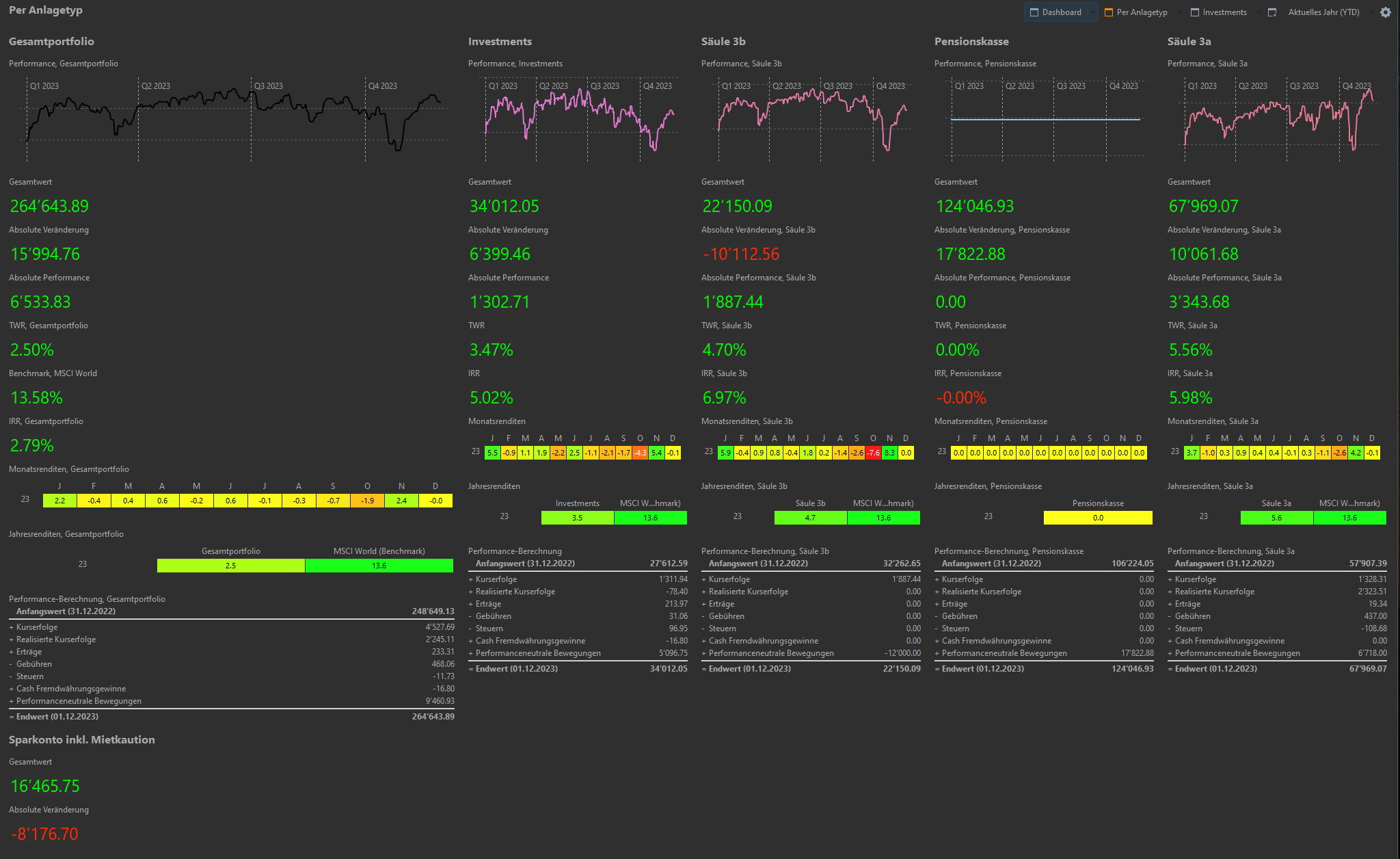

2023 YTD

I couldn’t really save a lot of money besides filling up the 3rd pillar and the life insurance (not paid yet and not visible in the graph).

There were many reasons for this, we bought a bigger car to accomodate our dog and daughter. It is a new car (not really mustachian I know :), but I got a huge fleet rebate from my employer and we don’t live in a big city with good public transport). In addition my wife took a few months unpaid leave to care for our daughter and I reduced my work to 80% for a few months for the same reason. On top of that, life got a bit more expensive :).

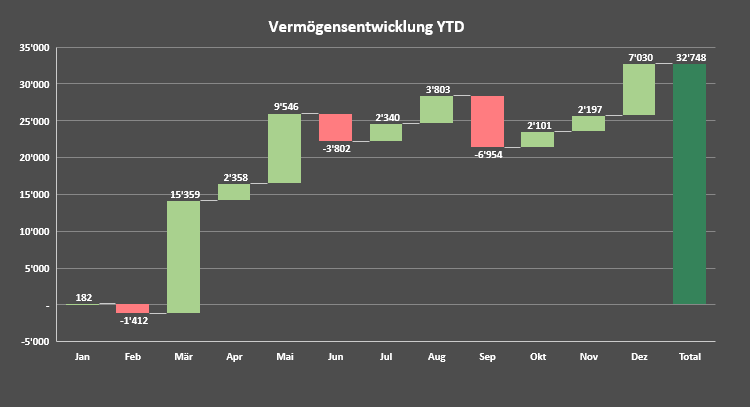

Since 01.01.2015

Overall I’m still very happy with my progression. Returns are rather low due to the big allocation to the 2nd pillar. But all in all it moves in the right direction ![]()

Expenses and Budget

I extended my Excel “a bit”.

Cockpit

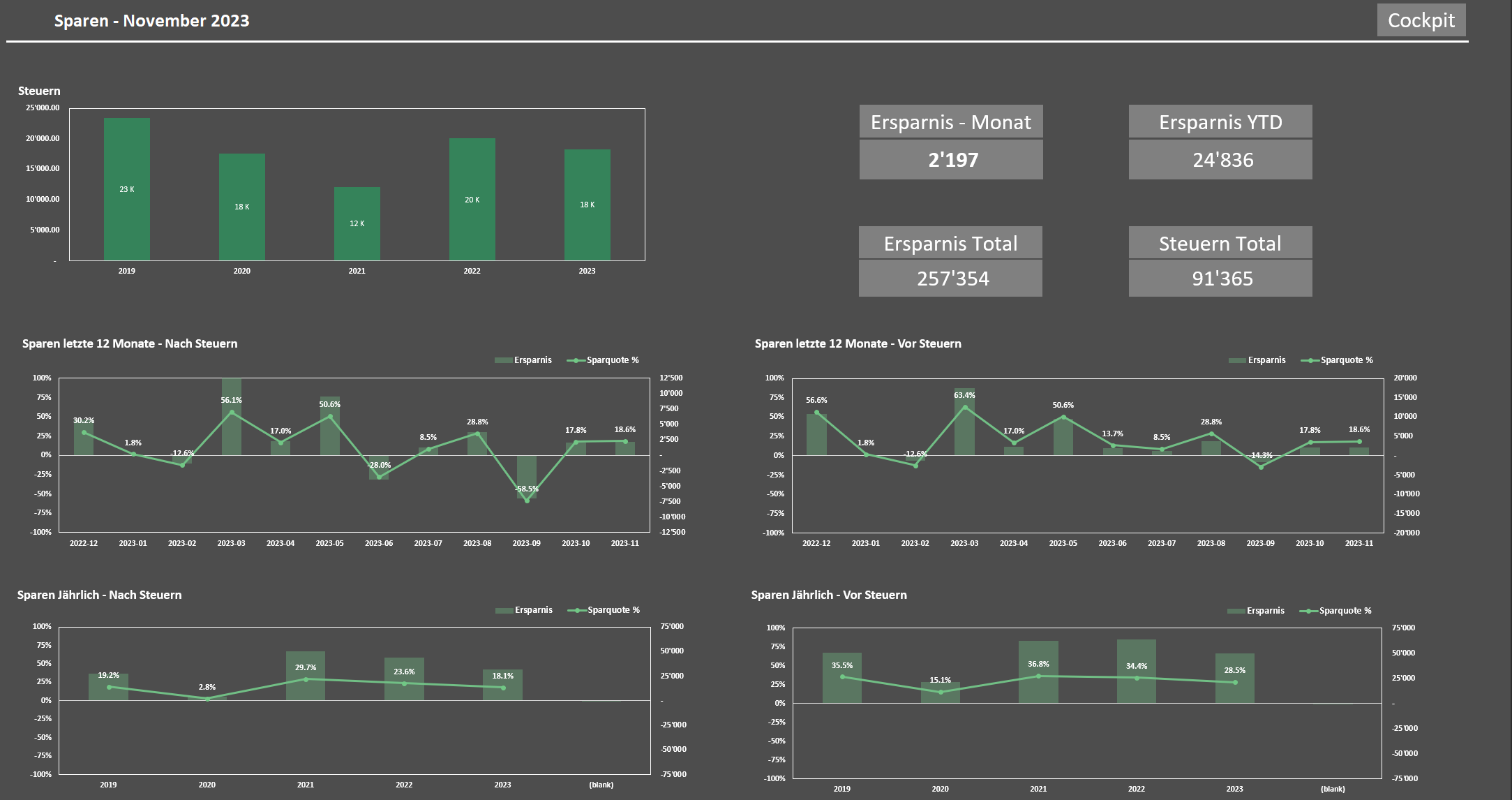

Savings

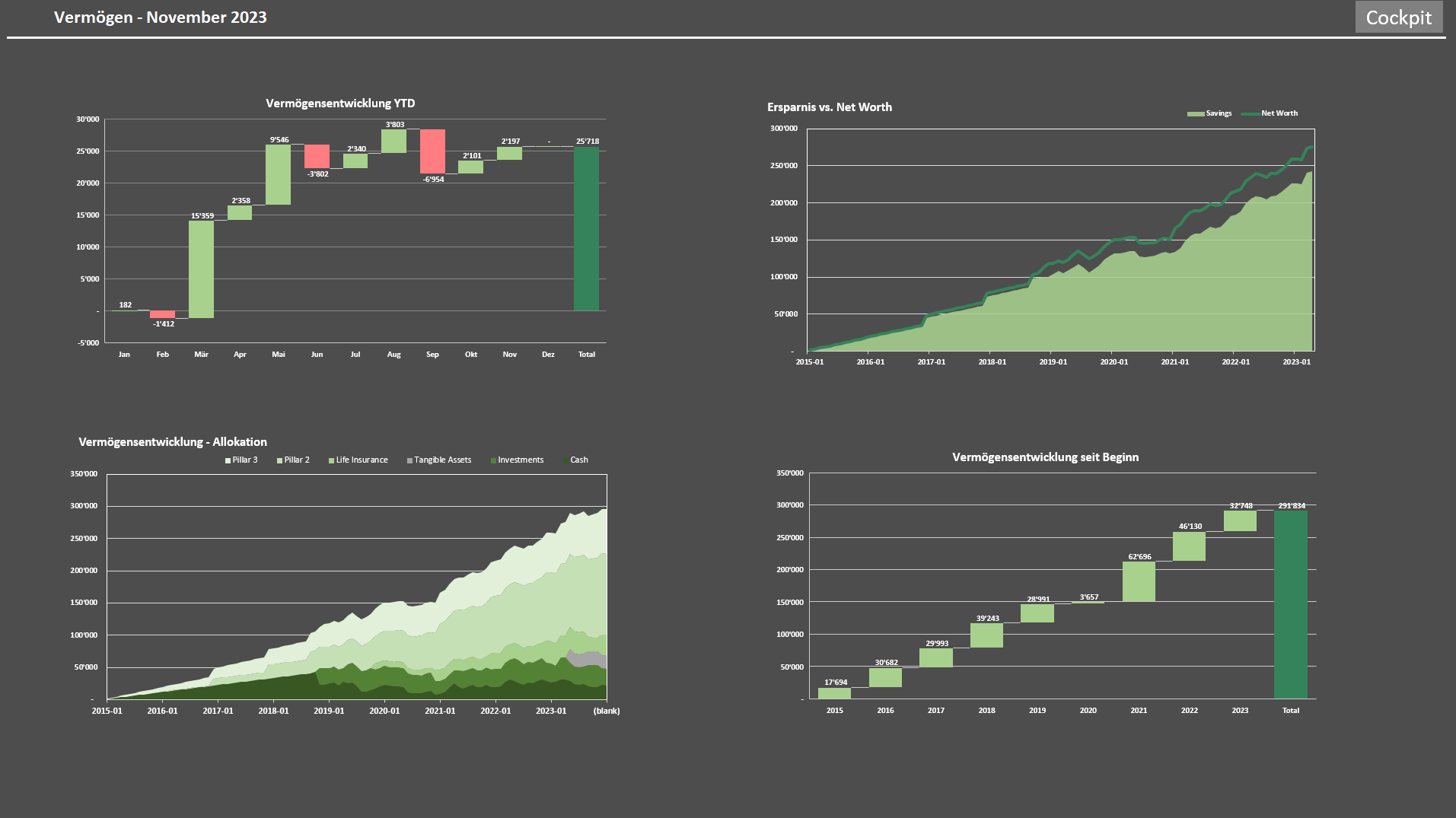

Net Worth

There are 2 other sheets that I won’t show here for privacy reasons, but they show more detailed views of our income and expenses.

As you can see, we still don’t live frugally at all ![]() We didn’t buy a house as we intented, but moved to a new big house with garden and are more than happy with it for the moment.

We didn’t buy a house as we intented, but moved to a new big house with garden and are more than happy with it for the moment.

I plan to FIRE at around 55 (prediction sheet in my Excel is in the works), but for now my focus is on my wife and our daughter and I try to not invest too much time in our finances at the moment.

Regarding 3rd pillar, I opened 4 accounts at VIAC invested in the Global 100 Portfolio and I’m filling them up equally now. The 3a account at the cantonal bank will not be filled anymore and I’m probably going to use this one in the next few years for buying a house.

Could you explain why you open 4 accounts at the same time? I hear people saying you should open a secound account after you fill the first with about 30k.

2023 was a good year so far in regards to performance. I moved the 3rd pillar at my cantonal bank (around 40k) to finpension and joined the quality club

(@San_Francisco)

Why did you move your 3rd pillar to finpension and not to viac, you could have opened a fitth one? What is the quality club? Anything special about finpension? @San_Francisco

This has to do with withdrwals of your third pillar. Once you can finally withdraw money from your pillar, the full amount has to be withdrawn. But if you have for example two 2 accounts, you can withdraw one account every year. This has a huge tax advantage [source]. An example in Canton Zug:

1 big account: CHF 100k = CHF 3.4k in taxes (3.4%)

2 accounts of CHF 50k = CHF 900 in taxes (1.8%), times two is CHF 1.8k

So by splitting up your accounts, you only pay 1.8k in taxes, instead of 3.4k, with tax savings = 1.6k. Obviously you have to take into consideration, that for 2 accounts it takes two years, instead of one.

The Quality club most likely is the 99% asset allocation into this fund at FP: https://finpension.ch/app/uploads/factsheets/CH0253609066_fact-sheet_en.pdf

MSCI World ex Switzerland Quality Index is a Strategy Index and seek to reflect a quality

growth investment strategy by targeting stocks with historically high return on equity (ROE), stable year over year earnings growth and low financial leverage. They capture quality factors.

This has to do with withdrwals of your third pillar. Once you can finally withdraw money from your pillar, the full amount has to be withdrawn. But if you have for example two 2 accounts, you can withdraw one account every year. This has a huge tax advantage [source]. An example in Canton Zug:

1 big account: CHF 100k = CHF 3.4k in taxes (3.4%)

2 accounts of CHF 50k = CHF 900 in taxes (1.8%), times two is CHF 1.8k

I know this reason. But I was wondering why he opened 4 accounts at a time and then fill the up evenly.

Why not open 1, fill up to 30k. Open second one, fill up to30k. Second pillar has reached 30k, and then open third one and fill up to 30k.

What is the strategy behind it?

The Quality club most likely is the 99% asset allocation into this fund at FP

Is this better than the global 100 viac?

I opened frankly a few years ago and put 100chf in it, the performance is so bad, still at 97CHF. Meanwhile viac has over 10% gain. I wonder how finpension performances

Because the ones filled up to 30k continue growing and can reach multiples of that by the time of retirement/withdrawal (unless you keep them in cash of course).

You probably want to keep them relatively evened out for that time.

All strategies work.

Option 1 -: open 5 accounts at same time and just fill them up uniformly

Option 2 -: open one account, fill up to certain limit, and then open another , and so on

In option 2 , one need to do a bit of math. Because every account will have a different holding period and hence different gains until retirement.

Four variables at play

Cost of accounts -: what is the cost of these accounts (frankly 0.44%, finpension 0.39% etc)

Strategy selection -: what strategy did you select when you opened 3a account. Different strategies can result in different performances. Frankly 75 will perform different than Frankly 45.

Timing -: when exactly you deposited the money, for example if you deposited 100 CHF in OCT 2022 vs OCT 2021, the current value will be very different

Buying fees (if applicable) -: some of the accounts have one time fees when you buy, so that money is lost

When I opened the accounts at VIAC I was not aware of finpension’s offering. And after some research I decided to try out the Quality fund (CSIF III Equity World ex CH Quality - Pension Fund DB) offered at finpension. In addition its a diversification of providers. So far it was a good choice ![]()

@Burningstone

Do you still have your 4 Viac Accounts or did you transfer all of them to finpension?

Yes I still have them and filling them up, they are in total only around 23k, while the one at finpension is at around 55k (up from 44k when I opened it last July ![]() )

)

Maybe at one point in the future there will be other interesting 3a provider and I’ll 1-2 VIAC accounts there to diversify further).