I had a interesting exchange with my health insurer when I informed them I was leaving Switzerland permanently to relocate to an EU country.

They asked my to complete a questionnaire which includes a question ‘‘will you retain a financial connection with Switzerland when you leave’’? So I asked the health insurer how should I answer this question since when I leave I will cash in my 3a and non-mandatory pillar 2 pension, but will retain no ‘‘financial connection’’ with Switzerland, i.e. no bank accounts or investments with the exception of eventually claiming my pillar 1 and the balance of my pillar 2 pension in several years once I reach the appropriate age.

Their response was that ‘‘the BVG lump-sum withdrawal also triggers the obligation to take out insurance in Switzerland, so that you must (continue to) take out insurance in Switzerland’’, but that I should check with the KVG.

I was very surprised at this reply because this practically means that anyone who has ever worked in CH retains a ‘‘financial connection’’ with the country because they will eventually get a Swiss state/company pension which triggers a requirement to retain Swiss health insurance.

Having looked at the guidance it seems that if you move to some, but not all, EU-EFTA-UK countries, then you can apply for exemption.

Given that the monthly Swiss health insurance exceeds the value of my Swiss pension this seems a completely nonsensical rule, and I was wondering if anyone has experience of this.

BTW I have written to the KVG (in English as my German isn’t good enough) for clarity, but still have not heard back.

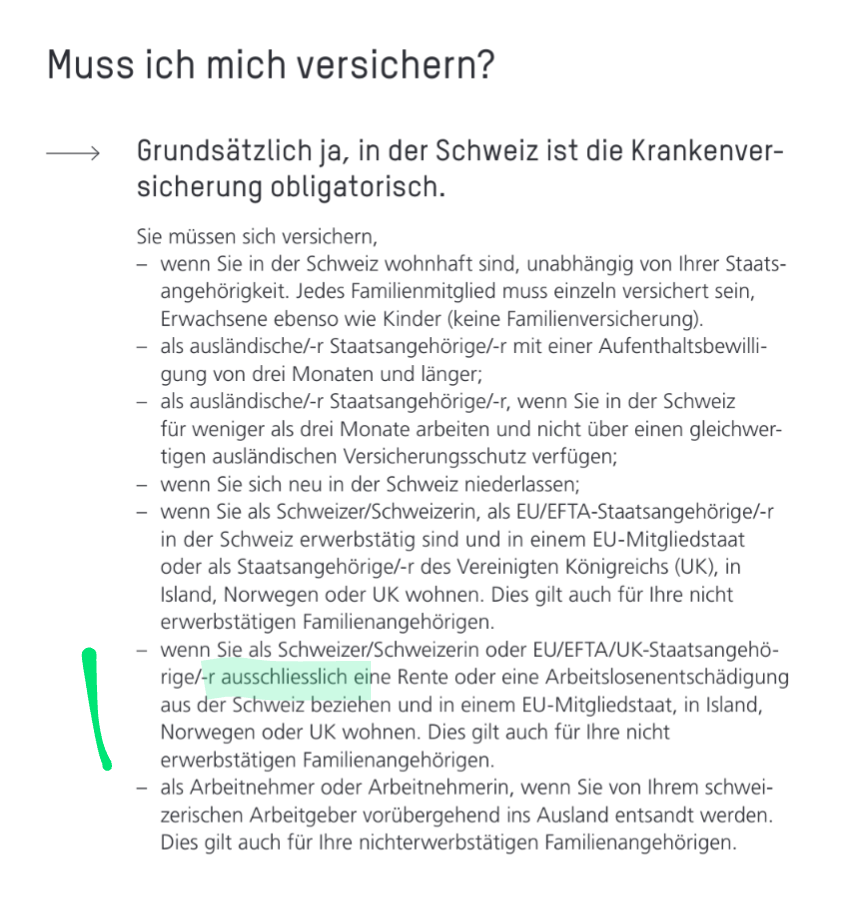

According to this document from the BAG it would be the RARE case that would fall under the obligation. Note that it’s only an overview and not the legal original.

You’d want to review the laws directly.

I have to speculate if it is the health insurers who are interpreting the rules in such a fundamentalist way - after all, they only gain from the situation should a customer of theirs continues to take out insurance with them after they have left CH.

(maybe they mixed up lump-sum and pension? this seem to only apply to pension)

The main question is: Have you reached retirement age? If you have reached the legal age for a standard withdrawal of your pillar 2 pension fund benefits for old age, then making such a withdrawal would place you under the requirement to keep Swiss health insurance. Early pillar 2 withdrawals (e.g. emmigration, home financing, etc.) do not qualify, and do not place you under the health insurance requirement.

Otherwise this only applies if you receive a pension from the OASI, DI, UVG, or BVG (occupational pension fund) and don’t also receive a pension from the EFTA/EU/UK country you live in or receive a higher pension from another EFTA/EU/UK country.

Of course, if and when you meet those criteria in the future, you will become eligible (e.g. when you begin receiving your OASI pension). But those future pensions do not represent a current financial connection to Switzerland.

It is worth noting that Switzerland has agreements with Austria, France, Germany, Italy, Portugal, and Spain that let you choose between Swiss and local health insurance when you move to those countries (if you are subject to Swiss health insurance).

Another situation in which you would retain a financial connection to Switzerland is when you are temporarily sent abroad by your employer. In that case, you can keep your Swiss health insurance.

If you have questions, the right office to ask is the Gemeinsame Einrichtung KVG / Institution commune LAMal. They are responsible for handling health insurance for people outside of Switzerland.

Daniel

Thanks Daniel, for your comprehensive response.

I completely agree with your interpretation of the rules. However, despite being fully aware of my situation (age, early withdrawal of pillar 2 pension fund, emigration etc.), my Swiss health insurer insist that I meet the criteria to retain insurance and are refusing to cancel my policy unless I can provide them with KVG confirmation. As I will leave CH at the end of September I have already cancelled my Swiss health insurance direct debit as my new policy, in my new country of residence starts then.

I have written to the KVG, over one week ago but still haven’t received any reply.

If you aren’t old enough for a standard pillar 2 withdrawal, you do not receive any Swiss pension, and you are not being sent abroad by your Swiss employer, then your health insurance provider is likely the one that is mixed up. That happens often enough, since they often don’t have experts for these situations.

Ask them to send you their arguments for not terminating your contract, and then contact the health insurance ombudsman for clarification:

Have you tried calling the Gemeinsame Einrichtung KVG? I also like to get things in written form, but calling is often more efficient, since you’re leaving this month.

Between the Gemeinsame Einrichtung KVG and the ombudsman, you should get a clear answer for your situation pretty soon.

Maybe there’s a mixup with Tourists abroad and globetrotters and what they want to see is the certificate of residence abroad?

I think I don’t get it. You reach 65, withdraw all your 2nd pillar and go to live in Polinesia. Why you have to pay Health insurance?

If you get the 1st pillar pension then it’s kind-of different. Still not logic that you need to forfeit 300-500chf monthly for the health insurance even if you live literally at the other side of the world.

Most of Polinesia is not in the EU/EFTA/UK, so you won’t need to insure it.

Isn’t it pretty easy, work one year in the new country of residence and get a minimalist pension from the new country ?

Answer: no.

It’s because of bilateral agreements between Switzerland and EFTA, the EU, and the UK.

Basically, all of these countries require some kind of basic health insurance and healthcare for residents. I suppose the agreement prevents pensioners from one country from mooching off another country where they did not contribute to the system. Or it could just be regulation for the sake of regulation.

As with so many other things: If you move to a country outside these blocks, then it isn’t an issue.

This is the best thing to do. Even if it turns out that you do have an obligation to remain insured, you will generally be informed about that by the Gemeinsame Einrichtung KVG.

But in the OP’s case, he was unsure what that question meant (who can blame him?) so he already has the issue.

Thanks Daniel

I haven’t tried calling the KVG since my German isn’t good enough and in my experience calling Swiss authorities without speaking the language often ends in frustration. So I set out the facts in written form and sent them an email (in English) - hopefully they will respond soon and clarify this is a misunderstanding on the part of the health insurer.

If time is getting tighter, I would still suggest asking a (Swiss-)German speaking friend to call on your behalf, after you explain the situation to him/her. It shouldn’t be the case, but the authorities are often more helpful that way (as you’ve experienced yourself).

Well, if you prefer to write, take your time to write an email in German. (Use an automatic tool and then correct the wrong parts). You want them to be comfortable when reading and answering your questions. It doesn’t matter if it takes you 1 hour to write and 1 to read. IMHO.

Yes, just give the text to Chatgpt and add an intro that this is an automated translation due to your non-familiarity with the local language etc.

Thanks both, I have done that - will update the post when I receive a reply.

I received the following reply from the KVG. Interestingly they fail to mention the UK in the list of countries (which I assume is an administrative oversight), but their reply clearly states that an application for exemption is only required if you only receive a Swiss pension. I will forward to my health insurer.

Gerne senden wir Ihnen hier die gewünschten Informationen.

➢ Falls Sie ausschliesslich eine schweizerische Rente (AHV, IV, BVG, UV, MV) beziehen:

Sie verfügen über ein Optionsrecht. Das heisst Sie können sich von der Versicherungspflicht in der Schweiz befreien lassen. Voraussetzung ist, dass Sie den Nachweis erbringen können, dass Sie über das Gesundheitssystem im Wohnstaat versichert sind oder werden.

➢ Falls Sie (ebenfalls) eine Rente aus dem Wohnstaat beziehen oder im Wohnstaat erwerbstätig sind:

Das Einreichen eines Gesuchs um Befreiung ist nicht nötig, da Sie nicht der schweizerischen Versicherungspflicht unterstehen.

➢ Falls Sie zusätzlich zu Ihrer schweizerischen Rente eine weitere Rente aus einem anderen EU/EFTA-Staat als Ihrem Wohnstaat beziehen:

Sie unterstehen nur dann der schweizerischen Versicherungspflicht, wenn Sie in der Schweiz länger in die Rentenversorgung einbezahlt haben. Erfolgten die Beitragsleistungen länger im anderen EU/EFTA-Staat, besteht die Versicherungspflicht in eben diesem Staat und das Einreichen eines Gesuchs um Befreiung ist nicht nötig.

Das Gesuch um Befreiung muss innerhalb von drei Monaten nach Wohnsitzverlegung bzw. nach Erstbezug der Rente gestellt werden.

Bitte übermitteln Sie uns die unten aufgeführten Unterlagen via https://versicherungspflicht.kvg.org/

I sent Olten’s response to my health insurer who claim they have also checked with Olten and still insist that I have to submit an exemption request since in their opinion my case aligns with the first section of Olten’s response (i.e. receipt of Swiss pensions AHV, IV, BVG, UV, MV)

I explained to my health insurer in my first exchange with them (& Olten) that when I leave CH I will only cash in the non-BVG part of my pillar 2, and my pillar 3a so the first section does not apply.

Any ideas on how to proceed are gratefully appreciated since I am getting nowhere with either my health insurer or the KVG, and in meantime they are continuing to take direct debit premiums from my Swiss bank account.