I’m interested and I’m very hungry to learn - I will take a look at the accounting for beginners, and the other articles on Net Nets which you wrote; that should keep me busy for a while

I think I understand; Net Net stock is only one type of “value stock”. I found this list on Investopedia defining what a “value stock” could be:

A share price that’s no more than two-thirds of intrinsic value. For example, if the intrinsic value is $30, the share price should be no more than $20.

A low price-earnings (P/E) ratio. The P/E ratio measures a company’s current share price relative to its per-share earnings. It’s calculated by dividing the market value per share by earnings per share. A good rule of thumb for value investors is to look for stocks with a P/E less than 40% of the stock’s highest P/E over the previous five years.

A low price-to-book (P/B) ratio. This metric compares a stock’s market value to its book value and is calculated by dividing the current closing price by the latest quarter’s book value per share. Typically, value investors seek companies with P/B ratios that fall below industry averages.

A low price/earnings to growth (PEG) ratio. This ratio is used to determine a stock’s value while considering the company’s earnings growth. It’s calculated by dividing a stock’s P/E ratio by the growth of its earnings for a specified time period. Value investors typically look for PEG ratios below one.

A low debt/equity (D/E) ratio. D/E measures a company’s financial leverage and is calculated by dividing its total liabilities by its stockholders’ equity. Like many metrics, D/E should only be used to compare companies within the same industry since a relatively high D/E might be normal in one industry, while a relatively low D/E might be common in another.

A dividend yield that’s at least two-thirds of the long-term AAA bond yield. For example, if the AAA bond yield is 3.61%, the company’s dividend yield should be at least 2.38%.

Earnings growth of at least 7%. Also there should be no more than two years of declining earnings of 5% or more, during the past 10 years.

In an ETF they will consider a stock to be a “value stock” provided that it meets any one of the criteria in the list above. Whereas, in your strategy you invest in only those stocks which are net net stock. Did I understand correctly?

So an ETF such as VTV would not contain 100% Net Net stocks; but it would likely contain some Net Net stocks + other stocks which were considered to be “value stock” for meeting one of the criteria in the list above.

You are almost there… almost because there is a BIG difference: In current markets no ETF will ever own a Net-Net stock. Why? Their market capitalization is tiny (think less than $50 million). These stocks are too illiquid for ETF managers. If they ever wanted to take a meaningful position in these companies, they’d make the price jump instantly… As an example, SHOS is currently worth $53 million, EGD is worth CAD 10 million… No institutional can invest in them, these stocks are too small!

So that’s also the advantage of the small guy, non-institutional investor… We get to go where the big guys cannot go, and uncover some big inefficiencies!

The second reason why you will very rarely find a Net-Net in an ETF is that they are quite rare in current market conditions… We are at the top of a 10 years heavy bull market, i’d say there are currently less than 10 relevant Net net stocks in North America…

Got it thanks

So ETFs will not include Net Net stock because the companies market capitalization is too small and they are rare. Well this motivates me even more to learn about Net Net stock investing and to include Net Net stocks in my portfolio because it would enable to intelligently invest in parts of the market which the ETFs are missing.

Thank you very much for your willingness to help - I very much appreciate it.

(I’m currently making my way through the accounting for beginners guide which you wrote - its awesome - I highly recommend it to any novices who might be reading this forum (even if you are not interested in Net Net investing!))

I have a hard time grasping, why commters seem to be ok with the idea that you can beat the market.

And not only that, but you can beat it with some back-of-the-envelope calculation.

Just to take on one example mentioned here:

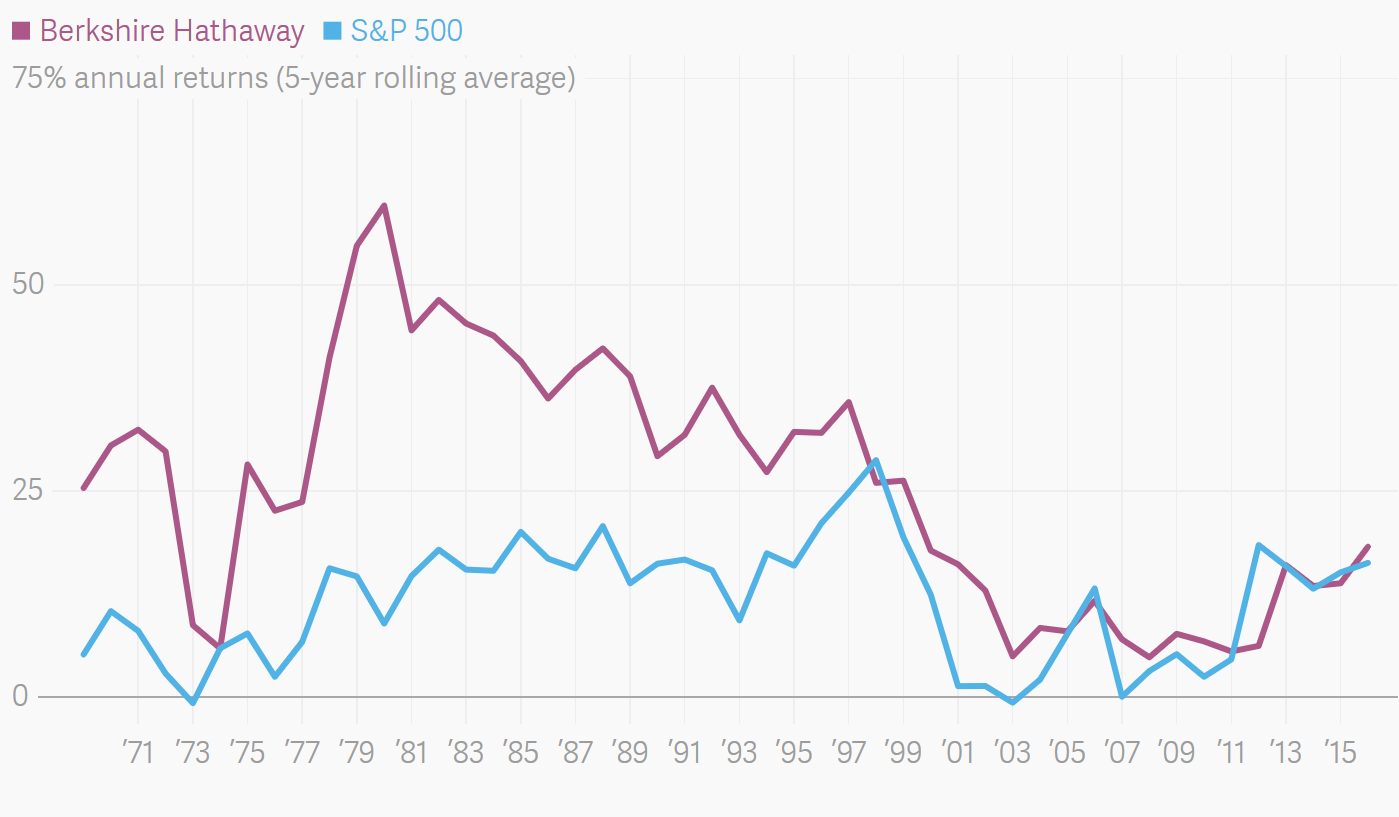

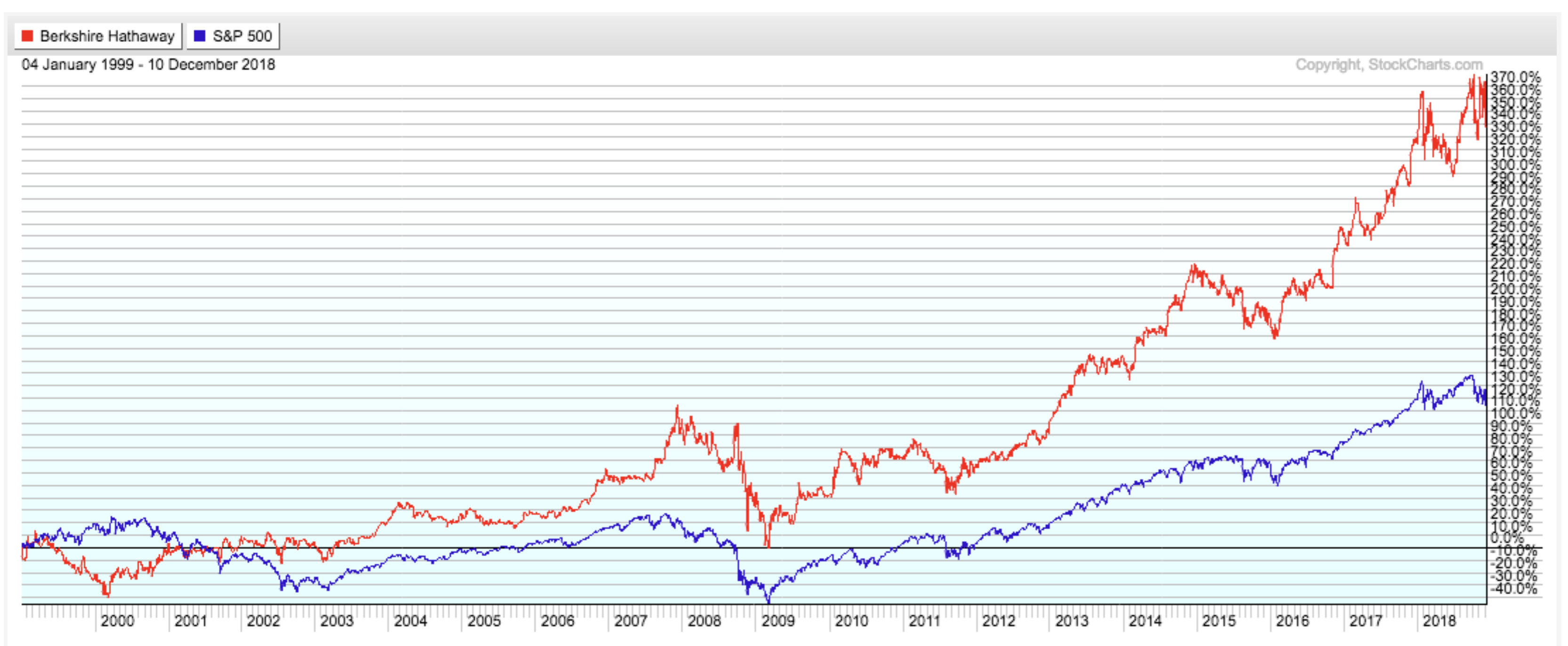

Berkshire Hathaway beat the market for 20 years. But they have been very inconsistent since around 1998.

As far as I understood:

They were pretty successfull back in the day because they identified undervalued small stocks.

Back then most stocks were only valued with high rigour by the big investement companies. These companies were mainly focused on valuing stocks of large companies. In turn stocks of small companies could often be undervalued for a significant period of time.

Nowadays there are many more financial institutions with a lot more knowledge and technology at their hand. This makes it much much harder to find an undervalued stock.

Oh, it’s alright. To take your example into account, Berkshire has “only” made 3.5 times the returns of the S&P500 since 1999. I’ll take this “inconsistance” any time.

And regarding my back of the envelope calculation, I prefer to be roughly right, than precisely wrong (ex: CAPM model, alpha/beta and other modern finance theories).

Fair enough, they are still beating the market overall/over a long time horizon. It`s just much less impressive now, then back in the day.

So, help me understand:

Why do you think, you can beat the thousands of small- to medium-scaled investement firms who would just absolutely love to get the kind of returns you have been getting?

I think they have similar time horizons as you have.

They have the means to correct false valuation of small stocks in a short time and they could make a killing doing it.

They have surely heard of Net Nets. They have thousands of employees at their hand, who could be running simulations on wether this strategy would have been a good tactic overall.

Why aren`t they doing it? Are they just irrational?

Yes, size is a big disadvantage. Especially when Berkshire is $500 billion big and the US economy “only” $19 trillion big. Given that Berkshire is ~1/40th of the US economy, that is still impressive to my eyes given the constraints. But yeah, it is unlikely they will have the huge returns of the 1970-1990 period in the future.

Oh yes, they should have heard about it. At least, those who believe in fundamental investing. Ben Graham talked about it first in 1934 in Security Analysis. The book has been re-edited 6 times since. He talked about it in the Intelligent Investor as well. Buffett practiced it at the beginning. Seth Klarman talked about it in his book. Joel Greenblatt as well. In the 1980’s there was as well the Oppenheimer study showing back-tested results of 28% annual. Heck, recently Mihaljevic consecrated a whole chapter to them in his book The manual of ideas. I am sure i can find 15 different books talking about it.

Oh you need much less to start a hedge fund.

And just to be sure, there are other persons practicing it. For instance, the Belgian blog Les Daubasses has been practicing it since 2008 (with other similar strategies), with +978% gains over the period. It’s not like it’s hidden.

Now for the question why institutionals are not doing it, there are several reasons.

First, there is a size reason: if you want to start a fund, you will soon discover that between compliance and legal costs, infrastructure and process costs and of course paying your employees, it’s not worth to have a fund if you manage less than $50 million of assets. Let’s say you want to invest a 10% position of your fund in a Net Net, you need to invest at least $5 million. EGD is a Net Net, it’s market cap is currently $10 million. Explain me how you are going to buy half the company without making the price jump mutiple times. There is simply not enough liquidity for them in these stocks.

Alright, let’s say they manage to buy some anyway. if you look at its financial reports, there is a reason the company is cheap: it is making losses, usually since a long time! Most manage don’t like to report to their investors that they are buying consistently money-losing companies, it’s just very uncomfortable. If it works out, they are a genius, if it doesn’t, they are fired. Their career risk is just too high. They are not irrational, they are very rational within their own rules, which is not the same as their investors’ rules.

And just to be clear, as stated in my first post in this topic, i do not advise anybody to follow this strategy. I am just explaining what i am doing and why, not why people should do it. To newcomers, I’d say people are more likely to be successful if they index the market.

And Buffett and Greenblatt say the same: just buy the market.

But, once again, neither Buffett nor Greenblatt are indexing. Thanks for their shareholders.

My thought wasn`t really that investors should follow the path of Les Daubasses but that they would allocate a small amount of their assets in this way.

This way of finding undervalued stocks would be super cheap and easy. Basically every local bank, insurance or retirement planning company could automate this.

I still don´t understand why these companies would not be doing this strategy. They often have at least some leeway to have part of their investement be of higher risk.

It wouldn`t take an enormous amount of banks/insurances to do this with a small percentage of their investements for the valuation to be corrected.

Let me answer this questionmarks after ten years at a bank and now working every day with these so called institutional investing specialists: managing money is not about performance in the first place, it’s about charging a management fee!

Most investors - and especially institutional investors - are not mentally strong enough to live with temporarily negative performance. And so the fund managers too. Don’t think of these guys that they are geniuses. They are still normal people like you and me. I seldom met one which acts really really rational and unemotional.

Goal of an AM firm is to grow AuM. ALWAYS. You are not able to receive big funds with an “experimental” strategy. Because at year end closing (or mostly even every 1-3 month) your investors are comparing your performance to others, thus the market. No asset manager could allow oneself to have a much worse performance than the overall market. As a result funds flow out of your fund and to others. No fund manager wants to lose clients, because they pay their salary. So, better than losing money is doing average, even if this means not beating whatever market index you want. Nobody loses his job doing average.

I could add several points more, but my fingers are getting tired as I’m writing on my phone

Thats already the whole story behind your questions

After reading the article on the blog, I started to look for more info regarding value ETF and found these awesome answers. Many thanks (a year too late then )

If you don’t have a thesis of why that is the case, no. Book value != cash, don’t just assume market is stupid, and banks are notoriously difficult to analyze.

Many large banks and reinsurance companies quote around or even below book value since the begin of the financial crisis. It doesn’t necessarily mean that the market is missing opportunities with those stocks, but perhaps that there is not so much trust in the solidity of the book value.

I’m really interested in trying Net Nets out (only paper trading for a start, but still). Since I’m lazy, I want to automate the first step. For that, as @Julianek wonderfully described, you need market cap and a few lines of the balance sheet. The market cap is available for free from almost any data provider, but I had no luck with API that offers balance sheet information. Does anyone know where balance sheet information can be gathered in an automated (and free) way?

If noone knows anything I will try scraping the data from somewhere, but I’m not looking forward to that.

Try https://developer.edgar-online.com/docs .

However, i’ll give you a warning: since i have posted this strategy three years ago, the market has been getting more expensive and net-nets become rarer and rarer. It is hard to have a diversified basket of 15 good net nets nowadays (that is, excluding shady chinese companies or biotech companies).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.