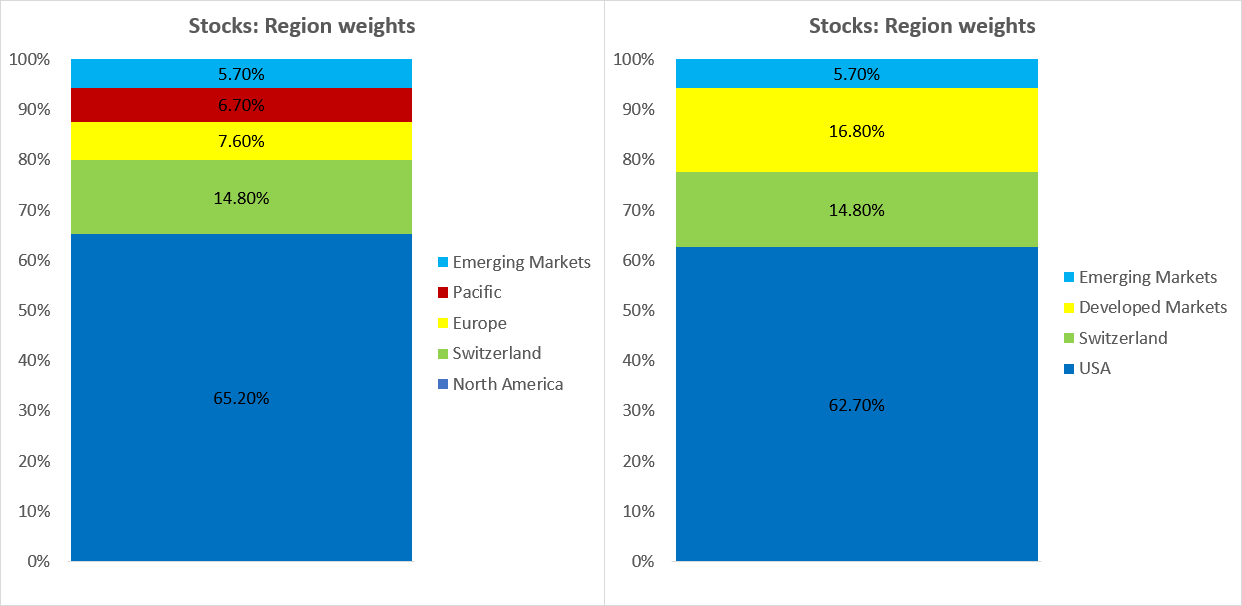

Home bias for Swiss folks is a bit weird, you have 3 giants who mostly have revenue from outside of Switzerland and represent 55% of SPI, they are headquartered in Switzerland but they could have been anywhere.

Given that by law your 3a investments are already biased towards Switzerland there’s little argument towards introducing more biasing, or at least use something that does not include the big 3.

There is nothing wrong with some home bias, but 40% is really pushing it. I wouldn’t bet almost half of my assets on 2.6% of the global market. Frankly 3rd pillar has already a 30% allocation to Swiss equities and 40% of the foreign equities are hedghed to CHF. So that should give you more than enough home bias. No need to add any additional Swiss ETFs.

The 10 largest companies in Switzerland make >90% of their revenues abroad, Nestle for example even 98%. Are they really Swiss in that regard?

What’s the point of hedging gold? I guess you understand what it means, right?

(4% is really small as well, is there any scenario where it makes a difference in your investment?)

Not OP. I know what Hedging is… But what does that actually mean for Gold? Is it like the same as owning gold-backed CHF? Or is the Gold just traded in USD somewhere, and then that money gets hedged for some reason?

My understanding is that it will (try to) replicate the movement of gold when expressed in USD, but in CHF instead. It’s fairly different from owning gold directly (personally I’m not sure I understand why people would do that, but shrug )

New to this forum, so bear with me! I started my interest for index ETF three years ago, but didn’t have the energy/guts to open a brooker account. Now, i am set with IB and Degiro (for kids) and 100k to be invested (the sooner the better even though it’s a weird “timing” amid the crisis - but hey we don’t wanna time the market, right). Nonetheless, I was wondering about one thing. There was a bull market over the past decade and almost all portfolios posted here started somehow in this period. Any ideas how to be well diversified for an upcoming bear market (if there will be any - or am I am already trying to “time” too much …)? Thanks for hints/replies!

Degiro for kids because of cost-averaging and portfolio way below 100k.

How old are you / investing horizon? Are you swiss / living in ch / working in ch / gonna stay in ch? Do you rent / buy your home?

I am 39 (2kids), Swiss resident, working in CH, gonna stay hopefully in CH. still renting in CH but I own an apartment in Europe that is sub-rented and “generates” about 6k / year (net).

About the horizon: the big unknown obviously, we would aim for 10-25years but it depends if we would buy some real estate in CH (in that case I’d sell the foreign property).

Just do IWDA+EMIM on Degiro and VT on IB. No hedging necessary for 15-20y time horizon.

If you feel like trying to beat the market, allocate a small part of your portfolio (10%?) for this purpose. If it outperforms, congrats.

If your purpose is to maximize profit throughout a bear market, I’d play the long game, take the bear market as an opportunity to buy cheap and make my profit once the stocks start going up again, turboboosted by all the cheap stocks that I have bought up to then. There are plenty of examples of portfolios that would sustain this strategy in this thread.

If you are afraid of drawbacks and feel you may be tempted to sell through a bear market if taking too many losses, an option is a conservative assets allocation (60/40 or 40/60 are popular ones you may want to study). Another option are defensive portfolios, meant to limit drawbacks rather than optimize returns. One example would be Ray Dalio’s All Weather Portfolio, another one the golden butterfly.

I can’t help if what you want to reduce is currency risk since that’s not something I’ve put real effort into understanding as of yet.

14.5k IBKR, 14.2k VIAC and 17.8k ValuePension, so 46.5k in total. Future contributions: 1.5k IBKR and 568 VIAC per month. I will quarterly adjust the MSCI World/USA ratio in ValuePension so that I don’t get overexposed in the US because of my higher contributions to IBKR and VTI.

Well, you are 39 with wife and 2 kids… and you want to go all in on shares? Whilst I understand you already had wealth of about 100k… i suspect that your ability to materially save will be constrained. Unlike people that save 30%+ of their current wealth you won‘t be able to buy low in case the market crashes.

Hi @TeaCup, thanks for your reply and consideration! Sure, I don’t wanna play lottery with my family, hence I am here to gather more understanding (apart from reading books about investing).

I haven’t been explicit enough maybe. We do have an emergency fund of 40k in cash, +contributions to pilier 2 and 3a (~120k) and some real-estate (~200k worth). So, the 100k for shares at IB are definitely not 100% of our net worth. As with many other mustachians on this forum, I also “accepted” the fact that my pilier 2+3 are some sort of bond investments (hence my balance bond/shares is already at about a 40/60 split).

My current problem/question is rather should i lump-sum invest the 100k onto the market or do cost-average quarterly over the next 24months for example. For the latter, does anybody know how much of negative interest rates are applied at IB for parkign CHF cash assets?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.