Why not - if it works in my favour? But I‘m not saying to deviate significantly from the index - even though in fact the ETF will (optimised sampling, costs…)

0.18% is the (theoretically) expected tracking error - not necessarily the actual, due to various smaller factors.

In this case, for instance, the iShares SWDA seems to have smaller actual tracking errors than XWDL. Here, for example iShares listed a realised tracking error of only 0.09% for SWDA.

So even though the TER (which does not include all costs and deductions) might be a base point more, the ETF might have better replicated the index - and returned more. Thus my earlier question about the „obsession“ with TER.

In this case anyway, the X-Trackers XDWL is a distributing fund, whereas iShares SWDA is accumulating, which might (also) be a more important consideration than than 0.01% difference in TER (which, as we saw, doesn’t even necessarily mean a more „expensive“ fund had „worse“ returns).

I have been thinking about this a lot lately. Do you think its best not to accumulate EM? I am considering it. I am also from a EM country (South Africa) and I know what’s going on back home and it seems things are just gonna get worse.

Hi guys, just wanted to clarify something. I believe that etf factsheets that are published include automatically the dividend reinvestment.

Consequently, for instance if you look at the SPI, the return include the reinvestment of approximately 3% dividend per year? I think this is clearly stated below the graph but i just wanted to make it 100% sure.

However, what about when you look at the index on Bloomberg for instance like here below for SMI. How are dividends taken into account when considering a specific index?

The charts showing growth of an ETF are accumulated and run against a total return benchmark. Indexes come in two forms: a price index and total return index. Price indexes are for example SMI, SPIX, SP500. Total return indexes: SMIC, SXGE, SP500TR.

But when it comes to Bloomberg, the tickers are confusing. SMI is the price index, but SPI is the total return. See the factsheets of SMI & SPI from SIX:

There are three standards flavours of indexes actually: price return (PR), total return (TR) and net return (NR). The latter considers dividends net of withholding taxes and this is the one that funds mean by “performance”. Your Bloomberg link indeed only shows PR index without dividends.

For NR index note that withholding tax assumptions that index providers make are often overly simplistic. Like for example they assume US always withholds 30% tax, but this is just not true for most investors: most countries have tax treaty and even when not you can go through Irish funds for 15% withholding. The fund industry perpetuates this little scammy trick because it makes their funds look better on paper than the benchmark with higher tax than it actually is in practice

To be fair, this setup might change during time. But in my opinion EU has not the necessary flexibility nor needed mindset of the important countries (GER, FRA, ITA, ESP), to handle a potential next crisis well.

I was searching a bit while, but I couldn’t really find the solution. Is there a possibility to build up in Interactive Brokers exactly the same portfolio like VIAC’s Global 100 strategy? I have the ISIN numbers, but I couldn’t search at IB on the mobile / tablet version by ISIN.

I really like the diversification of VIAC’s Global 100, and of course the performance. This is amazing! Pretty stable, solid as a rock, and performs like a dream

Any best practices, ideas?

Has any of you done the mirroring of the Global 100 strategy in Interactive Brokers already?

Hi Mustachians - amazing forum!

I’ve just set up an account with IB and now I’m trying to figure out how to set up a reasonable portfolio for myself.

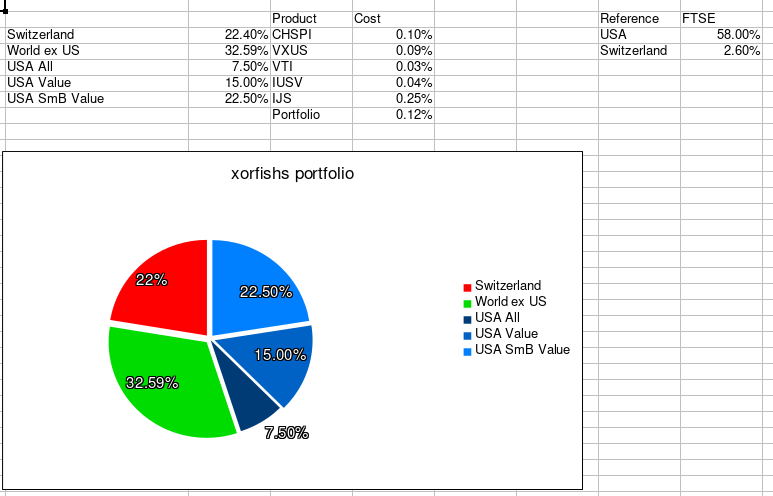

@nugget I like your portfolio idea of covering the world economy, 100% stocks & <0.1 TER. You have mentioned that the setup is close to VT (considering regions), but you have highly over-weighted mid & small caps (compared to VT). Is that also the main reason why you had to set it up using these 6 different ETFs?

I’m asking because I’m considering to go for a very boring portfolio and just go for 100% VT. Are there any other downsides of such a simple approach?

VXUS: Low TER Exposure to world without the US, including EM

VTI: Low TER Exposure to total US stock market

IUSV: Low TER and some exposure to the value risk premium

IJS: Reasonable TER and high exposure to value and size risk premium

I looked at other funds with size and value exposure, but many have a very limited exposure to the risk premiums or contain some clause for active management(looking at you VFVA). IJS is a bit more expensive but offers good exposure to the factors.

How would you summarize that paper? To me the tl;dr is not really a justification for home bias, it just says that investors have a home biases and in certain conditions it might be somewhat ok (but from what they say home bias is somewhat ok only for US, for the three other countries they would recommend investors to increase their foreign holdings).

From what I can tell, for a country like CH which no tax advantage and a concentrated stock market there should be even less justification for a home bias.

Figure 1 shows that the variance is the lowest with a home bias of

50% for Australian equities

30% for Canadian equities

80% for US equities

80% for UK equities

There is some tax benefit to holding swiss equities. Most Non-Swiss, Non-US equities will be have some non-recoverable withholding tax. I believe that holding Swiss equities will reduce currency risk a bit.

This is quite interesting as it is calculated in the home currency of each country. You can clearly see the risk/reward ratio sweet spots. I honestly would’ve expected some of the results to come out to 0% or 100% home bias. I’d love to see this analysis for Switzerland and somewhere in the Eurozone.

I wonder if they took into account tax credits that certain countries (e.g. Oz and Canadia) offer on dividends and/or capital gains from domestic companies. If not, I’m sure that would shift things significantly.

There is FX risk, just not directly. Roche and Novartis for example: only 2% of the revenues are made in Switzerland. The other big Swiss companies are similiar in that regard.

So the Swiss market is highly dependend on FX rates.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.