I suggest that we share opinions about multifactor investing here. After taking a look at the 2018 edition of Gerd Kommer’s book “Souverän investieren” I got interested in this topic again (my first acquaintance with Larry Swedroe’s book “Your Complete Guide to Factor-Based Investing” was pretty overwhelming for me).

How much does it make sense to invest in a mutifactor way? How to combine factors properly? The famous proponent of this approach Larry Swedroe is making a point that you could leave a greater percentage of you money in “safety” (like cash or non-stock 3d pillar) and then take a greater risk (with hopefully some reward) with multifactor ETFs. That would be a nice thing for a low risk tolerant investor like myself.

I’ve been looking at these candidates for a simple portfolio:

(RODM or INTF) + (USMF or LRGF or VFMF) + EMGF

or

IFSW (without EM)

or all-inclusive

ACWF

Any opinions or experiences with multifactor ETFs?

I didn’t know what Multifactor ETF so I tried to read about it.

On the first sentence they talk about “smart beta”. I stopped reading. I still don’t get what smart beta is, it sounds like gibberish to me (or if you prefer, “portfolio manager” l33t speech…)

For me it’s also big finance corporation bla bla, to sell some new products, costing more, bringing you less.

As the lady from Allianz at 1:53 says, the answer is to diversify.

…and the best diversification is index investing. (she doesn’t mention that of course though)

Funnily enough, this was uploaded today, and sums up the topic well and logically for me: https://www.fuw.ch/article/crowdlending-copy-copy/

The last 20 seconds sum it up, it’s nice to have all those factors, but none of them are consistently better, so if you have to diversify over all those factors, then it may as well be index investing.

Great series btw (only German though).

What he’s saying is correct in the sense that single factors underperform the market in different periods of time. They do however outperform the market over the long term (more than 20 years or so). The factors work consistently because you are taking more risk by factor investing (at least with small cap and value stocks that’s the case). Check this out:

What he’s not saying and what’s the main reason for me to be interested in factors is this: if you are a risk averse person like myself you want to put only a small fraction of your money at risk (say 10% of your money), then you can invest in factor ETFs long term, which will give you the same return as someone who’ll invest let’s say 15% in stocks. So the advantage is, you sleep better at night, knowing that you can only loose 5% of your money, which is more tolerable.

I’ll never understand why modern finance says that you would be taking more risk by investing in value stocks. I mean, if you pay a low price for the book value (i.e assets minus liabilities), it looks less riskier that paying more for the assets.

Let’s do a thought experiment :

Imagine that I sell you a 1 CHF coin. Which alternative would you consider riskier?

buying the 1 CHF for 80 rappens

buying the 1 CHF coin for 1 CHF and 20 rappens

For me the risk is paying too dearly for a company (or in this example, the 1 CHF coin)

The fact that value stocks works better over the long term is just common sense, not a riskier behavior.

The reason value stock are more risky is because these are normally companies with some current problems (like lawsuits or declining income) or in some unpopular sectors (like agriculture vs. IT). So these stocks seem like they will be worth less with time, so you don’t want to risk by investing in such companies.

I see your points but these two reasons are not valid in my opinion :

regarding unpopular sectors : investing is not a popularity contest. I am perfectly fine investing in unsexy stocks as long as they give me good returns.

current problems makes a little bit more sense, but it is just an interpretation, and not the definition of a value stock. I’ll try to explain you what i mean : for these problematic companies, the risk was investing in them before they had problems (and thus paying a high price for something of a lower value).

The definition of a value stock is “the price is less than the value” (in the case of Fama theory he refers to book value). I agree that a stock can arrive in this category because of operational problems.

But a bad business with recurring losses can be a very good investment is the price paid is low enough.

Conversely, a very good business with wonderful margins can be an awful investment if the price paid by the investor is too high.

So I’ll reiterate : whatever the underlying quality, if you buy a diversified basket of businesses for much less that they are worth (i.e buying a dollar for 50 cents), it does not look that risky to me. Risk is paying too much for something that does not hold up to its value.

I see your point. In terms of probability of making money the best company to invest in would be with the price to book ration of 1 as you buy just what the company’s property is worth without the “promise” of future prospects. If you buy 100% of stock of such a company and it goes bankrupt, you just sell its property and break even.

I forgot to mention one important thing about the risk. It’s the volatility of the value stocks that makes them risky, so their price fluctuates stronger than other companies. Stocks of value companies react to market downturns stronger than other companies, but they also flourish when market conditions are good.

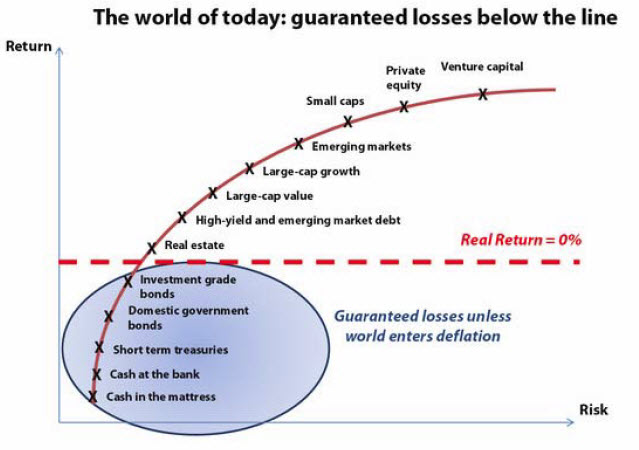

Is that really what hip economists say nowadays? What I came across is the efficient frontier concept, and there value stocks are rated as the least risky type of equity:

I really like this chart as it puts a lot of information together. The Risk axis is sometimes described as Volatility, and sometimes as Standard Deviation. It’s for you to answer where will you sit comfortably on this chart.

Btw, the source for this chart is an interesting read on its own:

Well, as far as I know, there’re two types of value stocks:

the most common type is that a company can be in financial distress, and thus it’s stock price is undervalued;

the other type is a needle in a haystack type, when a company wasn’t spotted by enough investors, and this kind of company usually is a small cap (because there’re so many of them).

In both cases, you have higher risk than blue chips stocks.

I understand that we do not have the same frameworks to think about stocks, but I am trying to understand your point of view and I have difficulties reconciling both views.

Let’s consider a value stock, i.e a stock whose current price is below a conservative estimated value of the company. For instance, let’s say the stock is quoting 50% below net tangible assets of the company.

I tend to think it is not riskier than a blue chip, but you tend to think the opposite.

Let’s review both cases :

The company is in financial distress, for instance it is losing money. If we consider a going concern principle (i.e the company seems to have a balance sheet strong enough to stand many years of bad results), then I would tend to think that :

Even if the company is currently losing money, I have a 50% margin of safety within the current price and the estimated value. That is, I would need either a big error in my estimation of the value, or new very bad events before the value of the company goes below my buying price.

I would tend to think that the stock was risky before being in distress, when the investor was paying fair value for the stock (or perhaps the stock was even overpriced), and thus the investor was paying too much for the company.

The company suffered a big loss in its market cap, so it is fair to think that its volatility has gone up. If we only look at the volatility, modern theory says the stock is much more riskier than before. However, if the investor had bought when the vol was lower (and hence thought as less risky), he would have endured severe losses.

Now the stock, due to its high margin of safety embeded in the price, has more upside than downside. The things that would make it go much higher are : either the company is making profits again (big profits for the investor) or just less losses than expected. Another factor is that investors adjusting the price of the stock to its intrinsic value. The things that could make the investor lose money is if the company does not redress its trajectory or if a lot of additional bad news occur. But there would need to be a lot of them, once again because of the high margin of safety.

So now the volatility is higher, but somehow the stock looks to me less risky than before.

If you compare it with a blue chip fairly valued, you really are at risk of bad news occurring, for instance as happened to Facebook recently.

So i am not sure if the distressed company is more riskier than the blue chip. I think the key hypothesis would be the going concern principle, i.e the company must have a rock solid balance sheet.

In the second case where the company is not in distress but investors have not seen the full value of the company, can you please expand on your thoughts? I really have a hard time understanding why it would be that much riskier than a blue chip. We are in the same case as 1., except we much less disadvantages.

I think the most important risk is the possibility of bankruptcy and a company in financial distress and/or a small-cap has a bigger overall chance to bankrupt than a blue chip with well-established, stable, diversified sources of income. The second risk is obviously volatility, and here also it will be bigger than blue chips.

Bad news can happen to both value and blue chips, and bad news is more dangerous to a company that has already financial problems and/or is small and might not have enough resources to survive the crisis. I don’t consider this a valid argument. Besides, 90% of the time you’re not at the edge of blue chips losing half of the value like in 2008. But even if you were, in such cases value companies might lose even more (or might be even everything).

You assume that a value company can only go up because it’s undervalued. Well, it can also go down or stay in place for a significant time. It’s not written in stone that an undervalued stock can’t become even more undervalued (for instance, you made an error in estimating conservative value) or remain undervalued for years (other investors don’t spot the value) or go bankrupt (for instance, there was a price bubble in the stuff that company owns, and their net tangible assets go dramatically down in value).

I don’t really believe that investing in smaller companies or companies with financial problems is less risky than investing in big, stable companies. It’s common sense.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.