I’ve been lucky with some fortunate timing when investing in small caps which turned out to be multi-baggers.

My biggest win was investing in Fever Tree right after the IPO and I made 1000%. This was early on in the gin-tonic craze, I accidentally ran into the product, loved it, googled it and found out that it had just IPO’d and put my money to work.

I rarely make investments like this and only do so when I know the product and am a strong believer in it.

So, with that in mind, I am considering stepping into Blackline Safety PowerPoint Presentation

Canadian small cap / high revenue growth / high % recurring revenues / disrupting a niche industry and taking significant share / likely it’ll eventually be acquired by a major player.

Would appreciate thoughts on this business and also if others can provide any high conviction small cap ideas.

I like this model as well… it does require a lot of investigation. here are 3 that I am looking at but did not pull the trigger. I think all of these require a multi-year horizon. Not financial advice

Evolution = EVO

I-Tech = ITECH

Shift4 Payments = FOUR

I’ve seen the same run-up in the weeks prior to the previous quarterly earnings call… hopefully a favorable signal.

This should be the quarter where they make a profit for the first time (driven by strong top line growth) which will be a great signal and reduce/eliminate the risk if new shares being issued.

I did step into Blackline a while ago and the business and share price has been developing very nicely. I suspect there’s 200-300% upside on the stock over the coming years even without it being acquired. Without looking behind the limits of the current market they play in they could easily triple or quadruple their revenues. At that stage, I expect they can also expand into adjacent markets.

The did a webcast today (not related to earnings) and the share price popped up.

The company looks promising. I do wonder whether they can move fast enough to maintain their lead and avoid competitors from eroding their early advantage.

Whatever you gain, it can be way more when you are able to hold long enough. A bitter experience of mine: bought priceline in the 90s I think. Made a few 100% and sold again. Then they became booking and I think I would have made 10’000% or more. But would have does not buy you anything.

Big gains are bought with volatility. Since I do my mechanical growth-momentum strategy I had a few nice multibaggers. One has to lift many stones to find a diamond… but there are diamonds.

At the moment I hold Vista Energy with a plus of 1024%, Supermicro with a plus of 500% and Constellation Energy with a plus of 434%.

From the past I had Antero Resource with plus 750%, Console Energy before the merger plus 653% and a few more.

Supermicro was at 2000%. I take partial profits once it reaches 500%, 1000% and so on. But with such gains the position is always too big and the Hindenburg attack was a source of much volatility. But anyhow, Supermicro still exists and Hindenburg does not…

I’ve done that a few times as well and you can then wind up thinking “what if?” but I’d rather at the end of the day do that with the profits in my pocket than thinking “what if?” with it all having evaporated. Same in reverse, I was relatively late to step into stocks like Apple, Google, Nvidia and also Bitcoin… as I was constantly telling myself “it’s probably too late now” but even stepping in relatively late in such omnipresent stocks results in tremendous profits.

Good question to ask. It was also asked in the webcast Q&A and the CEO said they have a 3 year lead. I thought that was conservative and just as I was telling myself that he verbally said the same.

I have ‘some’ knowledge / experience of the market they are operating in and cannot see the larger players catch up in a few years. Partially due to the time it takes to develop new products/services like these (not just the hardware but also the software; there comes a point where throwing more resources at it doesn’t accelerate but may even decelerate development time). Even more so though because the larger competitors have an inherent inertia because they are not as focused, they have a lot of other products to invest R&D in, they have a legacy organization with hidden agendas to protect their own budgets thus hindering more progressive reallocation of resources, they have a sales/marketing organization which is used to selling widgets in a box rather than SaaS, etc. etc. - you can also see that (in the webcast) when the numbers are shared on competitors sales flatness or even (substantial) decline in this space.

So, very good question you’re asking but the larger competitors have had years to respond and are incredibly slow (keep in mind, Blackline has been in business a few years already - they’re far beyond being a start-up). The Hardware Enabled SaaS model is also gaining momentum with end-users so it may even become easier to extend the lead.

At some point though, a competitor will simply buy them as they recognize it’s mission impossible to develop this capability internally and much faster to acquire it AND gain a competitive advantage vs. other slow larger competitors.

I just wish there was an opportunity to buy options so I could have more leverage than when buying shares.

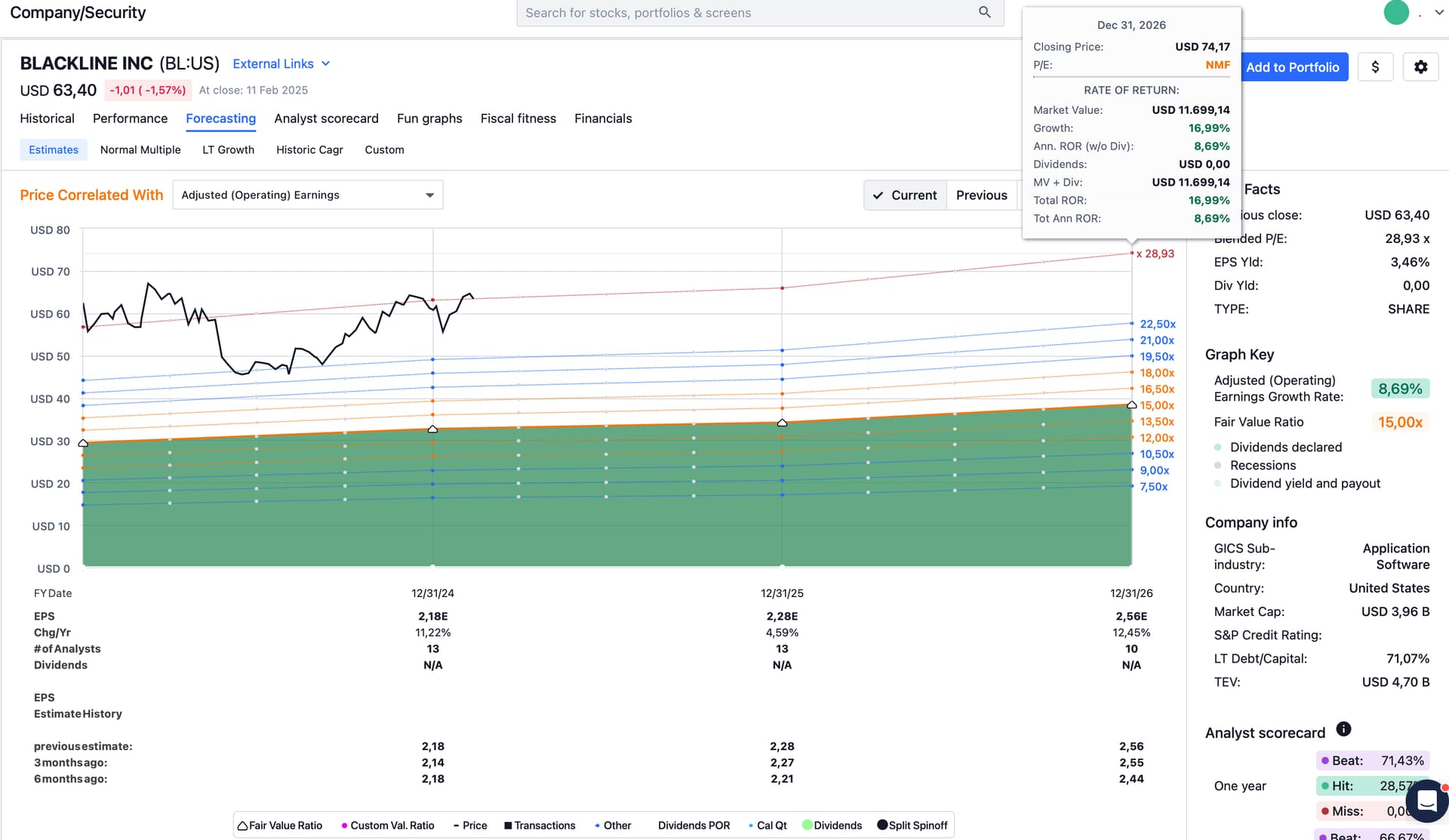

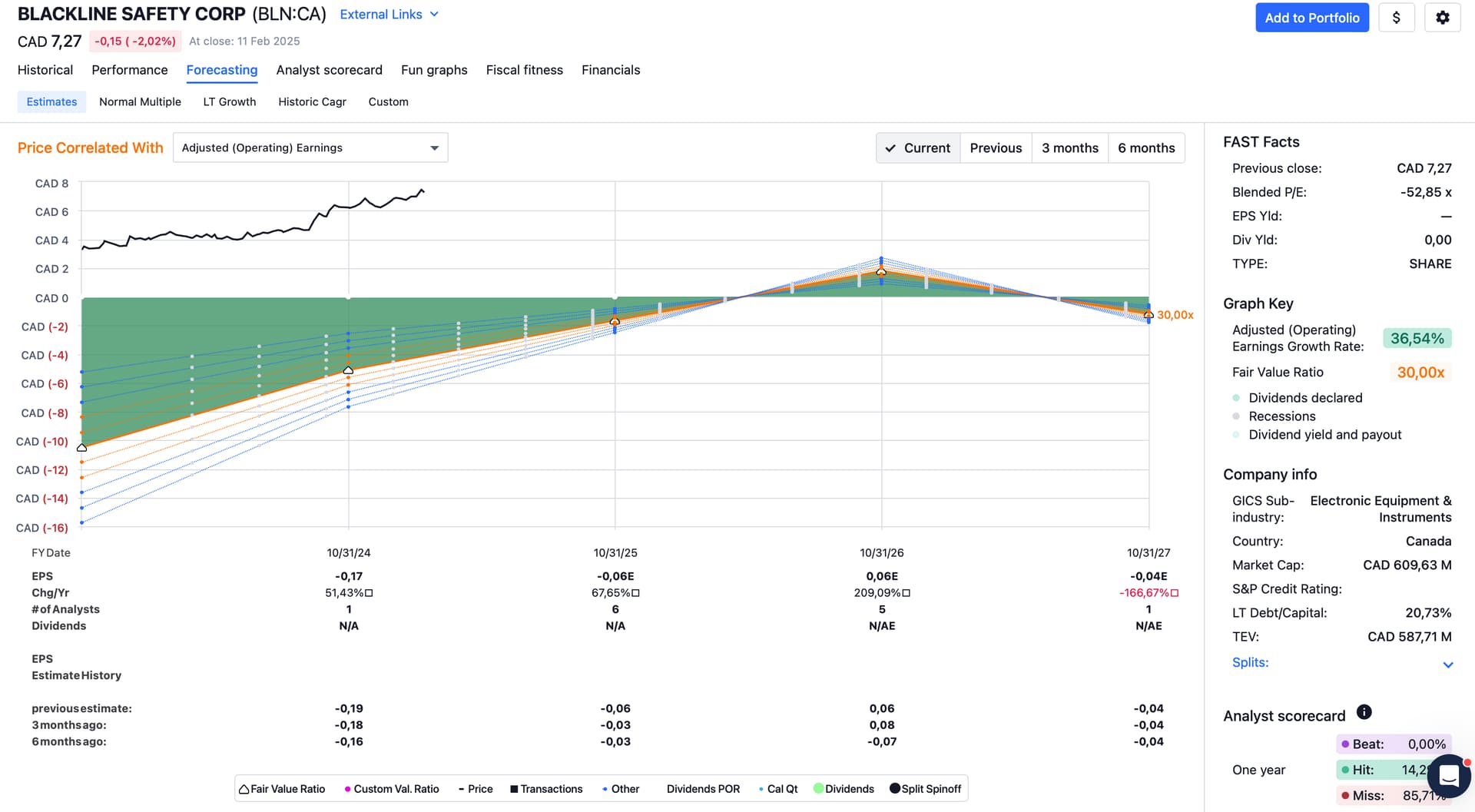

Re valuation

Current market cap is around 500M Canadian $

If they just deliver on their formal target then they’ll hit $400m in revenues at 30% EBITDA = $120M in the not so distant future => given they are makign 80% GM% on SaaS part of their revenues (and how sticky this is with multi-year contracts), this is a very reasonable target

It’s not outragous to assume a EV/EBITDA multiple of 12 for such a business = 1.4-1.5B $ valuation

That’s just with them staying in their current lane though. Once they start generating serious cash they can start doing acquisitions and plug in additional offerings in their connected SaaS model and there’s also a lot more ‘detection’ offerings they can expand into.

For the time being though, all they need to do is keep executing.

It’s obviously a very different business than Fever Tree but I’m getting the same feeling here of the business being very solid and operating in a market where there is just a wave they need to ride vs. stale competitors. Those three elements of capability + market momentum + slow competitors can make for a nice return.

I’m intrigued by the other poster with his list of multi-baggers and especially that some of them are energy companies. Thanks for listing them - need to look into it!

“Seems the analysts were a bit underwhelmed by the earnings call. ”

The boost came after the webcast (organized a bit later than the earnings call, it was facilitated by an IR advisory firm working for Blackline).

To a certain extent I’m not surprised by the limited interest so far. It’s a relatively small company in a niche industry with some large shareholders who’ll determine its future in the end.

A major reason I am bullish is because I know the industry and the company pretty well and if this means I can keep adding shares at a reasonable price, then I’m fine with that.

Another angle: 3-4 years ago the share price was close to $9 Canadian… since then the company has continued to execute on its revenue growth trajectory, has seen GM%'s increase and has streamlined expenses all resulting in it breaking even. I just can’t see why their trajectory will dramatically reduce in speed any time soon. The reason for the drop a few years ago was because they were close to running out of cash (and there were some other factors related to Covid / chips shortages which hindered their growth trajectory for a while). That’s now also resolved and no longer an issue. Again, adding to my high conviction on the fundamentals of the business.

This is a case where I believe in the business and I do not just look at it as a “stock” to own (this should always be the case but realistically I also frequently acquire shares more purely on a metric basis).

We’ll see where this ends. I realize it’s a difficult company to value based on traditional metrics like PE or cash flow ‘as is’ so I revert back to the question of “what if they deliver on their targets” (around market share and implied growth, around gross margins, etc.) and then you can more easily model the forward looking valuation.

Another example where this helped me get over my worries about buying something too expensive was ONON - the Swiss ‘Nike’ so to speak.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.