I did look at OCF and FCF/EQ as well, but that didn’t look better and I thus didn’t post.

Here they are:

-

Operating Cash Flow

-

Free Cash Flow to Equity

I did look at OCF and FCF/EQ as well, but that didn’t look better and I thus didn’t post.

Here they are:

Operating Cash Flow

Free Cash Flow to Equity

The nature of (Hardware enabled) SaaS business is fundamentally different (recurring revenues with high GM% and thus also rather different benefits of scaling fast). Whether right/accurate or not, multiples of Sales are more often used than multiples of earnings/CF for valuation and this multiple is influenced by other metrics (like the Rule of 40).

In the end, if everybody agreed on the same valuation, there wouldn’t be much trading on the stock market so these differences keeps things interesting:)

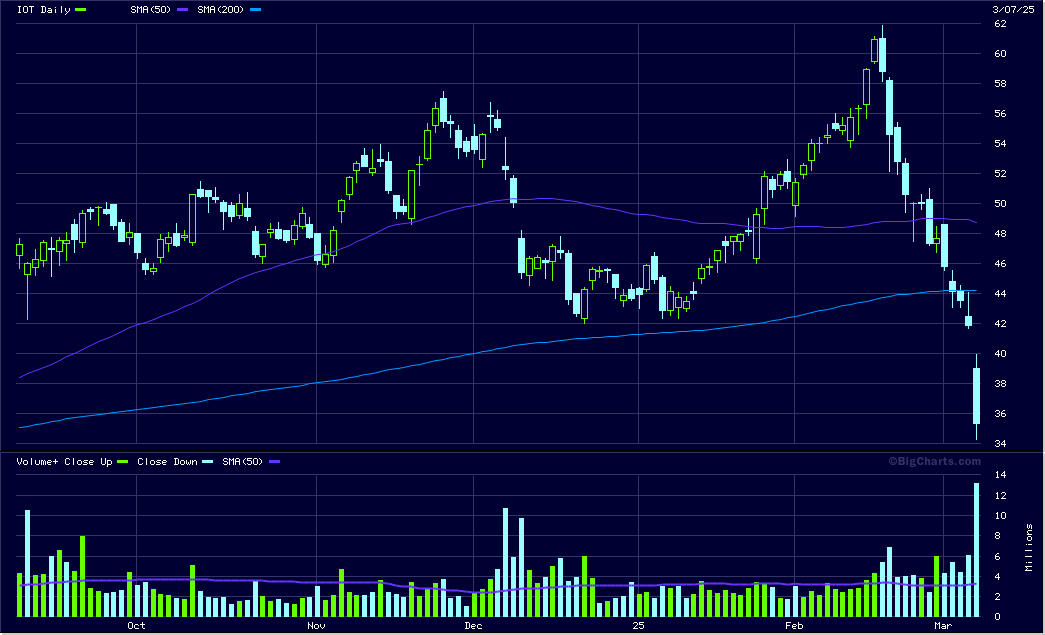

Finally found a listed company which one could use as a reasonable benchmark: Samsara (ticker: IOT)

That company is much further ahead (1B+ revenues) and sheds a light on what’s possible. The valuation is rather heavy also… which points to Blackline being cheap.

Quiet volatile:

But still kind of expensive. Even after the drop of 15% on Friday…

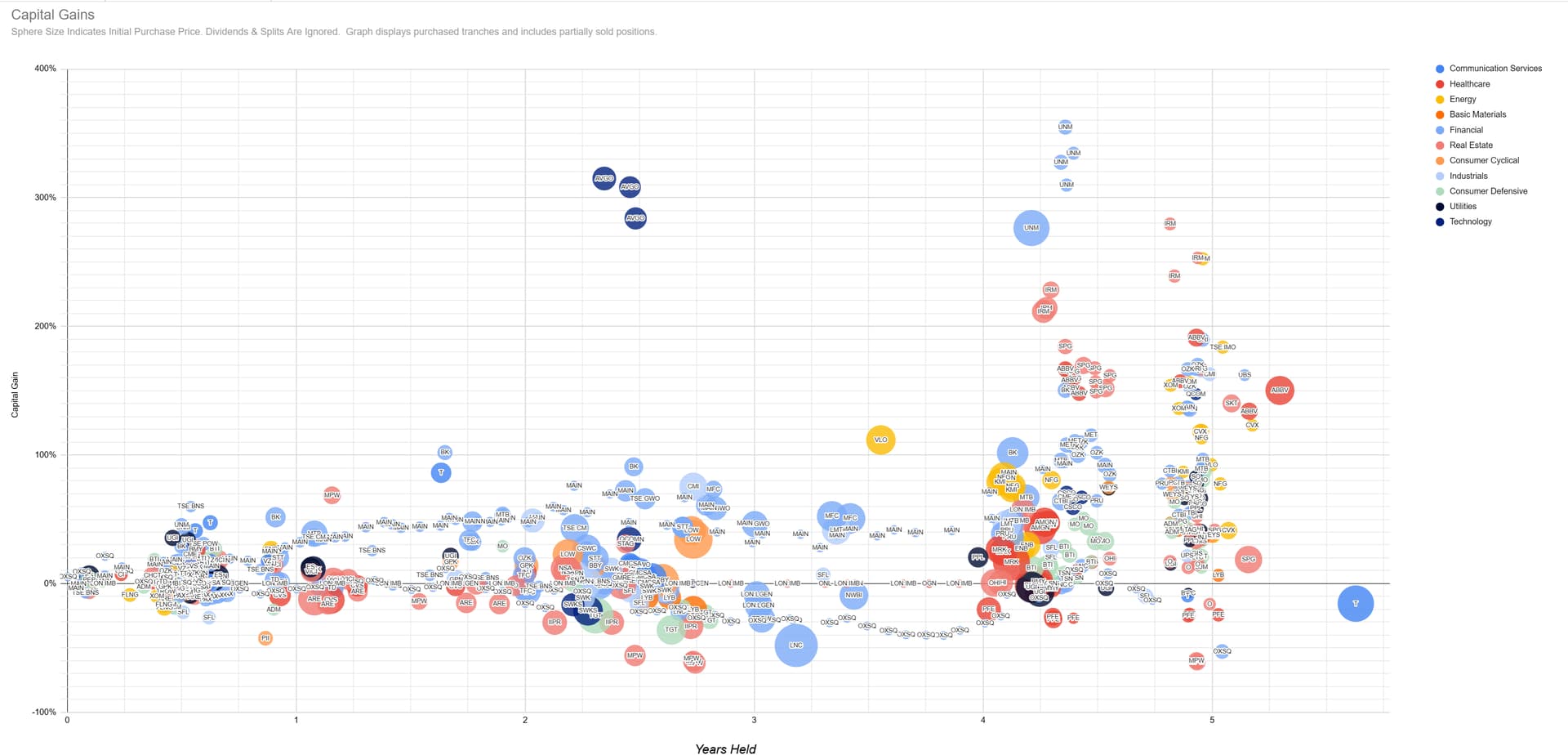

All my multibagger have one thing in common: they were completely surprises. At the moment I hold the following multibagger, some of it kind of boring bigcaps: ABBV,AVGO,CAT,CEG,CMI,FTI,MET,NUE,SMCI,TRI,UTI and VIST

Definition of a multibagger is a capital gain of more than 100% without dividends. The key for multibaggers is to hold as long as possible… but not longer.

I would agree …

You’re still paying a multiple of over 100!

Also, in my mind I expand their ticker IOT into “Internet Of Things” which is a term that has been tainted by my déformation professionelle (in the cyber security space people like to think of the “Internet Of Things” as the “Internet Of Shit” …).*

That’s where we differ: I planned all of mine. ![]()

Most of my multibaggers are also plain old boring companies (perhaps with the exception of Broadcom).

And as you state, time does most of the heavy lifting.

Agree that Samsara is expensive and what put me off a bit is that they’re not profitable despite having scaled quite a bit (more than 1 billion annual revenues if my memory serves me well).

Here is the recent earnings release from earlier today from Blackline Safety though:

"Blackline Safety Reports Record Fiscal First Quarter 2025 Revenue of $37.7 million, up 43%, and EBITDA of $2.1 million

Record Annual Recurring Revenue(1) (“ARR”) of $70.9 million, up 31% year-over-year

32nd consecutive quarter of year-over-year top-line growth

Blackline achieves “Rule of 40”(1)

Gross Margin improves to 60% in Q1, up 500 basis points year-over-year

Net Dollar Retention(1) (“NDR”) was 128%, seventh consecutive quarter above 125%"

So:

This is part of what makes investing so difficult and fun though… for every buyer there is also a seller with a different perspective:)

I like (understatement) the trajectory Blackline is on and the market opportunity they are addressing. THe Samsara reference was just to create some ‘fantasy’ about what the valuation of a Blackline could be (using the multiple on revenues).

I would never have uncovered Blackline if I was not an expert in the space they operate in. I suspect for the vast majority of investors they are well below the radar screen (due to being Canadian and small-cap).

Interesting times ahead - also Blackline had a drop past week and I pulled up the truck to acquire more shares. Will be curious how the market reacts to todays earnings release.

New one here, only just started to look at it. In an interesting space (healthtech) which I know little about but their business model looks appealing and it’s an opportunity to get in ‘earlier’ than the Blackline Safety case mentioned above. Company is called: DarioHealth. Am curious if anybody here with a background in healthtech has an interesting PoV on it.

Nice, from 6000 to 0.5. Come on, still space to zero. At the cash-burn rate they have probably little time left to try. Or do they spend it on people promoting it on the mustachian forum?

They have the ultimate medication that could have saved my mother from dying from cancer I suppose. Too late for me.

A month ago a little pump-n-dump seemed to have worked, hope you did not get hurt there:

briefly looked at the 10K. Stock-based compensation is 60% of revenues? Looks a little suspicious if you ask me

I knew this one would trigger a response:)

I’ve not yet had the time to look at ‘what happened’ during the earlier years of this company’s existence - perhaps a case of a a group of execs/investors shifting their business model looking for something which works. In any case, I am intrigued by the space they are in with the potential it brings as well as by the revenue momentum and SaaS margins. While they’re still burning cash, the valuation vs. where this business potentially could be in say 5 years if it maintains this momentum is modest. Clearly a rather risky play compared to Blackline which seems to be going from strength to strength and is ‘out of the gates’ in terms of proving their viability as a business / offering. Blackline was in a similar position just a few years ago though (at much lower stock price). No guts, no glory:)

Blackline got a boost from US/China relations warming up and the recent news of awards for some of its products. Let’s see if the door is open for sustained increases going forward. Upcoming quarterly earnings will be key.

With a business / stock like this there’s always going to be volatility up and down but recent developments are very, very encouraging:

This is not a stock for those seeking faint hearted. Things will go up and down.

I’m a fan of this company/stock (if you hadn’t guessed).

They just announced quarterly earnings:

“Highest Ever Annual Recurring Revenue (1) (“ARR”) of $80.2 million, up 29% year-over-year

Record third quarter revenue of $37.6 million

Net Dollar Retention(1) (“NDR”) of 128%, surpassing 125% for the ninth consecutive quarter

Adjusted EBITDA(1) of $1.3 million and 5th consecutive quarter of positive Adjusted EBITDA

34th consecutive quarter of year-over-year top-line growth”

Blackline Safety Reports Record Fiscal Third Quarter 2025 Results

They also recently had a very strategic customer win in the middle east which confirms their trajectory and competitive position (vs. larger multinationals) is stronger than ever.

Biggest bull factor? I trimmed my position in it a few days ago ![]()

Roughly 30% premium over current share price.

Damn, there was a lot more potential in this stock (incl. for a future acquisition at a higher price).

Good pick. As always, sometimes our great picks get taken out by buyouts. Still bitter about ARM acquisition by SoftBank.

OK, here’s a new one that I’m starting to look at. 86M market cap, so very small: Aluula - a patented materials technology company with the “world’s lightest, strongest, and fully recyclable composite fabric” and with traction of adoption with a number of well known brands.

Will be doing more research and - potentially - taking a position.

Here’s their recent IR presentation: PowerPoint Presentation

“Key Q1 highlights include:

![]() 85% increase in overall ALUULA sales compared to Q1 2025

85% increase in overall ALUULA sales compared to Q1 2025

![]() 83% increase in Performance Outdoor channel sales

83% increase in Performance Outdoor channel sales

![]() 162% increase in Commercial Industrial channel sales

162% increase in Commercial Industrial channel sales

![]() 42% gross margin within target range

42% gross margin within target range

![]() Sales order book pending production exceeded $3.5 million CAD

Sales order book pending production exceeded $3.5 million CAD

![]() 54% increase in production staff to increase capacity in advance of new manufacturing facility”

54% increase in production staff to increase capacity in advance of new manufacturing facility”

They are substantially investing to expand capacity and the revenue growth coming in the future will enable higher gross margins and net profitability as the business scales.

Very interesting, thanks for sharing.

How do you hear about those companies, never heard of them ![]()

I think with these kind of companies the search for applications and the ramping up of manufacturing are the key. The question then is… does it become a 50m, 200m, 1b revenue company? Or crash and burn beforehand.

Sofar, the few applications marketed are civikian (high texh sports gear)

How do i hear about then?

These dont come from metrics screens like with large caps (eg “min market cap xyz and min div of x%”

Typically come from

In this case, imagine you pay attention to a brand like arcteryx and then notice they are using a new material in their products and then find out who supplies it

ie keep your eyes and ears open at all times