If someone signs a SARON with a 10 year maturity or penalties calculated like a fix rate montage sorry but it’s a lack of research on their side (and I’m not sure this is even legal especially on the penalty side…), it’s just like signing a 3B product without understanding the surrender value calculation table.

Try to transfer a mortgage which is 100bp above market conditions with several years before maturity then we’ll see if this is that easy.

NB: I have worked in the Swiss mortgage industry for more than a decade and I see a lot of mis information in this thread, giving an opinion is surely fine but making wrong statements is another thing, I hope this forum keeps some form of self moderation.

For me, this is a strong incentive to lock in low rates for as long as possible (ideally until the entire loan is repaid).

Though if you’ve already locked in the low rates and still need to re-finance at the end of it, at least you had them low all through the period when they climbed to the top of the interest rate cycle and no worse off than having SARON at the top of the cycle.

I understood but market conditions will not always evolve in your favor and it’s important to stress that a fix rate mortgage can also be a burden. Might have been a no brainer 3 years ago when you could sign a 10 year for 0.6% but go tell that to those guys who signed a 2.7% one 6 months ago and have to sell now because of some life events. As a side note one option to consider if you have a low rate mortgage before transferring it is to give it back to the bank as they might have to actually pay you ^^.

The debate between SARON or fix rate is not black or white unfortunately, important is before going for one or the other to understand whether it fits your personal situation and your risk profile.

But that’s exactly the situation this thread is talking about. Getting a 10 year fix at 0.8%. Then only way the market is going to beat that by 1% is of banks start paying you 0.2% to borrow money!

I agree if rates are 2.7% it is more debatable. Although 2.7% is still be no means a high rate.

Well this is an issue somewhat separate from financing. As everyone should be aware, buying a house is a long term commitment that comes with certain risks and your life situation should be in order (and perhaps insurance taken to cover some events).

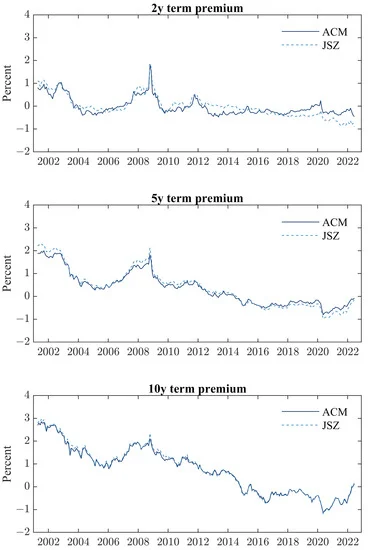

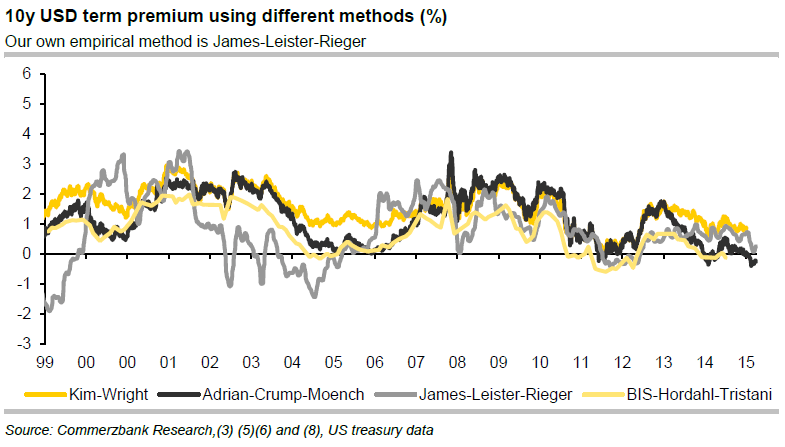

Interesting question, as far as I know, all of these three scenarios happen (depending on the market conditions). In the paper I linked about Norway, there is this figure:

Sorry, I would like to exploit the fact that you had already read these papers and pick your brain with a following question.

I guess they are talking about the realized difference between paying the short or long term rates, that came out post factum. In this case, the result is mostly the difference between past expectations and what had come true. You can see it: the premium is negative in 2020-21, during the period of very low interest rates as controlled by the central banks.

Am I right?

While it is interesting, it doesn’t help us to make a decision now. What I was wondering is if such a premium (or discount) is calculated into longer term rates from the beginning.

Say, a bank’s analyst says: we expect the “average” SARON over next 5 years to be 1.1%, so we are happy to borrow for 5 years at a fixed rate of 1.25%, giving 0.15% as a premium to the lender.

Not quite, they actually provide econometric model that decomposes the swap rate into the expectation of the short term rate and the term premium. So these models (and there are quite a few with different approaches / methodologies) could be used for what you describe.

Maybe banks do this analysis, I do not know that. On the other hand, why should they care too much about the term premium? As a bank, I would be happy to always make 1% risk free, no matter if the client chooses a SARON or fixed term mortgage. Sure, if I think the market is wrong and the term premium too high for some reason, I could give out unhedged fixed term mortgages with the chance to maybe earn 1.2%, but with additional risk. My assumption is that banks analyse their whole portfolio regarding the interest rate risk (as far as I know, they have to because of Basel 2 regulation). Based on that, they can decide what the optimal hedging strategy for the whole portfolio is.

OK, let’s assume now that there is no built-in premium in longer term swaps; or they are rather small or we cannot identify it.

That means that we assume that swaps are “true” values reflecting the predicted evolution of SARON.

Even if it is not the case, these rates serve as a starting point to determine the mortgage rates anyway.

These are the reference, “true”, market-determined borrowing rates (under the assumption above).

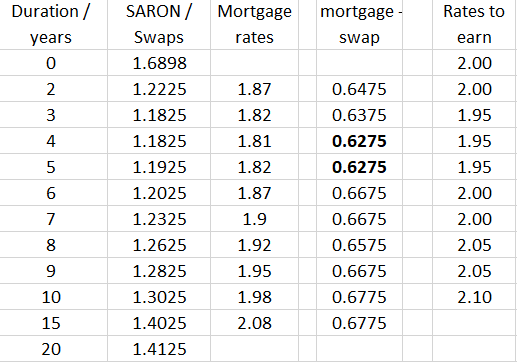

The rates are suspiciously increasing after 6 years. I suspect it is the built-in premium.

Best mortgage rates (Avantage Service), data from moneyland.ch, and their differences to swap rates for the same duration.

Note that the best SARON margin is around 0.6%.

Best rates for saving accounts and mid-term notes (Cembra), data from moneyland.ch.

These are the best rates that you can earn as an individual investor.

Huh. They are actually higher than the best mortgage rates…

So, this simple comparison shows that:

for the best advertised mortgage rates, the markup is not much higher than the best SARON markup.

The value of around 0.6% also corresponds to what was mentioned ones by @Cortana as a very good value.

the optimal duration for a fixed term looks like to be 4-5 years.

For longer durations, there are signs of the built-in premium in the swap AND the markups are getting larger.

Conclusion:

Always compare proposed fixed mortgage rate with the interest rate swaps to determine your personal markup.

I wonder if this dip could be due to banks passing on fixed costs of raising a mortgage and this being more expensive when spread over a shorter term and then reaches an optimum point before the term premium exceeds the spreading effect?

This is super insightful, thanks for sharing. I have a related question:

We financed our CH home on a 100% Saron mortgage with a 0.6% margin. We have a rental property abroad (DE) which will come up for refinancing soon. The DE bank explained to me that the Saron mortgage is viewed as a risk (obviously due to flexible interest rates, aka “stress annuity”) and will negatively impact the rates they offer for the renewal.

Personally, I have little interest in switching the Saron to a fixed rate mortgage at the moment, but it seems I will need to explore this and alternatively also look for other banks in DE which model stress annuities differently. I would be super grateful for some strategic thoughts by the mortgage experts here. Does it makes sense to switch to a 10 year to get better rates in DE or is this just an issue that certain banks have? Thanks in advance!

Totally agreed with @HoiZame, each bank has different rates and usually the rates which are public are negotiable. You don’t like one rate or how they treat you, go to another. Or better send your dossier to several banks at once and see who you like the most.

The rates are pretty high currently compare to 2 years ago. Can it go higher in Germany, with the inflation and forecast - maybe yes. But probably I would go more flexible in this times than save on some 0.x %.

Unless we hit a major recession soon and central banks need to lower interest rates drastically, it‘s not going down that much over the next years. A slight gradual decrease to a moderate base level, if no recession and solid economy.

Dont play here Dr. Doom, but look how Germany does de-industrialize itself, check how prices went up compare to your salaries of your friends. See how we eqsy financing lots of money to the 13. AHV payment, financing wars (which we are not involved), how easy many non-educated people with families are coming into Europe and require support. Those mega trends are costing a lot, but taxes will not raise. This will be financed by the inflation (tax). So I assume rates will not go down but rather go up.

One thing I don’t really understand is the following.

How can be the 1 year swiss government bonds at 1.01% while the CBR is at 1.50%?Additionally the 1Y Swap rate is at 1.18% according to UBS quotes.

For me it seems to be a too big interest gap to not get used for arbitrage. As a big bank i would short sell the swiss gov. bonds (1y) , pay 1% and get 1.5% from the Swiss national bank for the deposited cash. Just before the 1y is done, the bank buys back the bonds at par with the deposit at SNB for the profit.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.