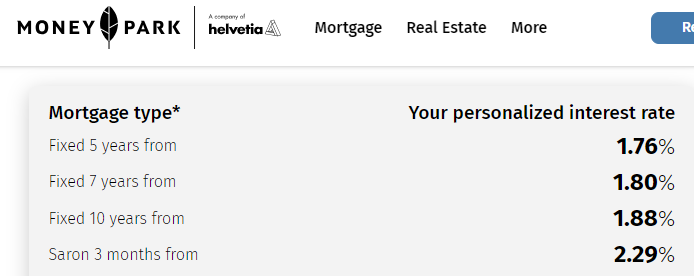

I am examining the prevailing mortgage interest rates. According to Money Park, SARON appears to be the more expensive option at the moment. I had always assumed that SARON would be the cheapest option. Could someone clarify why currently the fixed-term rates are lower? @Cortana ?

Depends on the interest rate curve; this can obviously change based on the market.

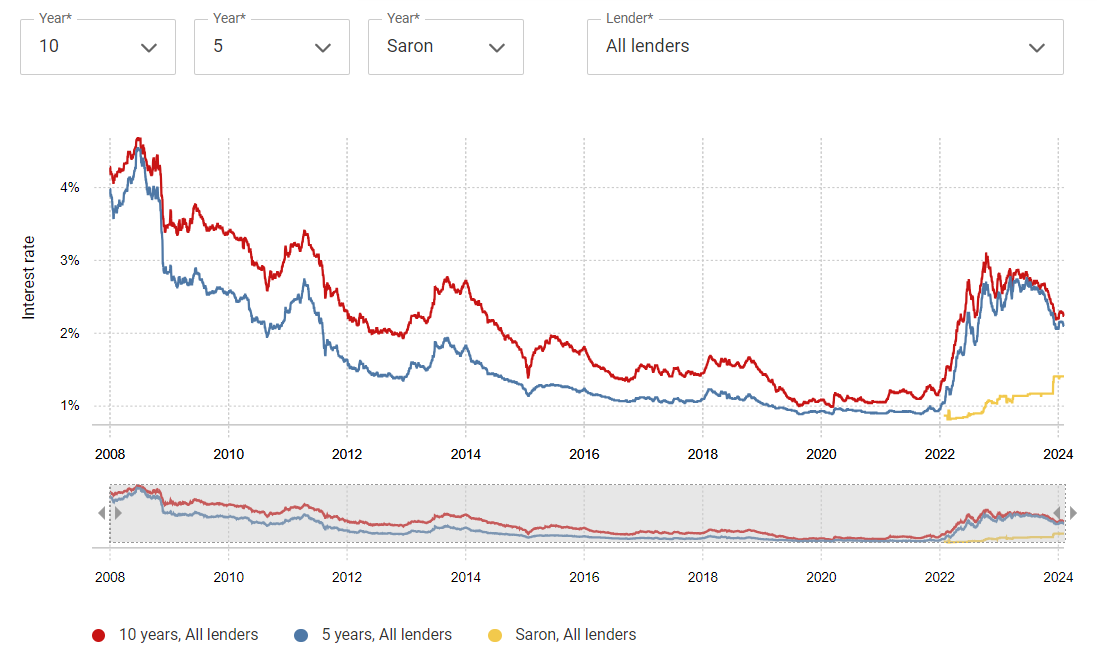

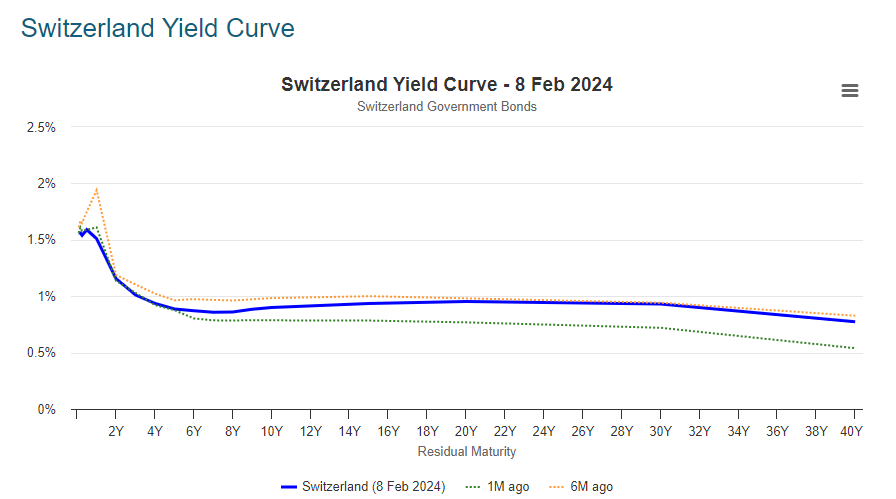

Swap rates are pricing in a decreasing Saron rate, therefore, fixed mortgages are lower (for the moment).

2 Likes

Personally I think it’s rather meaningless to compare rates for different durations. Instead, you can try to compare them with “free market” interbank rates to determine the markup in each case.

Here I have started to sum up the sources for the latter:

P.S. another reference I use is the best interest rate of savings account (duration equivalent of SARON) and of medium term notes (usually Cembra), which are duration equivalents of fixed term mortgages. These are the best rates that you can earn as an individual investor.

P.P.S. My first impression from these data after I made a quick comparison once, is that for durations longer than 5-6 years, the markup really goes up.

I feel that people were really missing the woods for the trees in this thread. 0.86% is a great rate and you have it locked in for 10 years? Why were people not just grabbing this with both hands?

Sure, if rates stayed low for 10 years then you’d pay 2.6k more each year on $1 million. But at current rates, you’re now paying 14.9 more per year wiping out 5.7 years of the theoretical savings each year it continues and probably a lot more stressful to boot.

We had historically low interest rates and the cost of insuring against rate rises was low. Just take the gift that’s being handed out to you!

1 Like

Thank you @xerox5003 @Dr.PI - Does it mean the marked (banks, institutions, etc) anticipate a decrease in SARON rates? I’m considering purchasing a property and am currently unsure about the best option. I had the free consultation with Money Park, during which they suggested that I might opt for a 2-year SARON plan and reassess later. By combining my personal funds and pledging my 2 and 3 pillar, I will be able to meet the 33% requirement, thus eliminating the need for amortization

I suppose recency bias and the fact that they got greedy and perhaps felt it could keep falling. Absolutely crazy low rate!

1 Like

It is hard to tell, what the “best” option is - you definitely can tell that afterwards ![]()

But yes, the analysts are expecting lower rates towards summer/autumn 2024. If you trust them and you have a good gut feeling, you can stay in Saron and then switch into a fixed term mortgage - maybe the rates are better in five, six months?

I fixed my mortgage in 2019. Honestly, I didn’t even bother looking at SARON. I was just looking for the best 10 year fix and also whether I could extend beyond 10 years without increasing rates too much.

2 Likes

1.69% the current SARON rate and the 2.29% above is including SARON + 0.6% uplift, is my guess. I’m very risk taking with some investments but when it comes to primary domicile, even ~1.8% seems fair.

Exactly, the problem with SARON is the uplift (part for the bank) normally around +0.4 - 0.7. Making then worst option than the fix rate.

Currently, you can get offers around 3-5 years fixed from 1.75 to 2, and SARON is 2-2.4. So it needs to drop to less than 1% to start to pay out somehow.

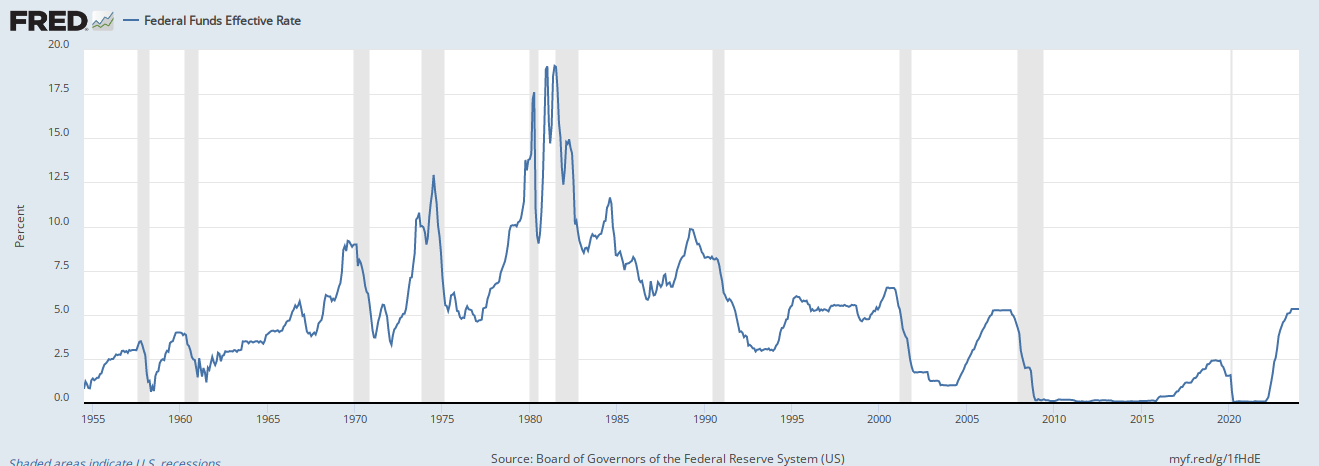

Then again, rates have been in a 40-year bear market since the early 1980s, not just in the US.

The older amongst us may remember times were quite different in the 1960s/ 1970s:

2 Likes

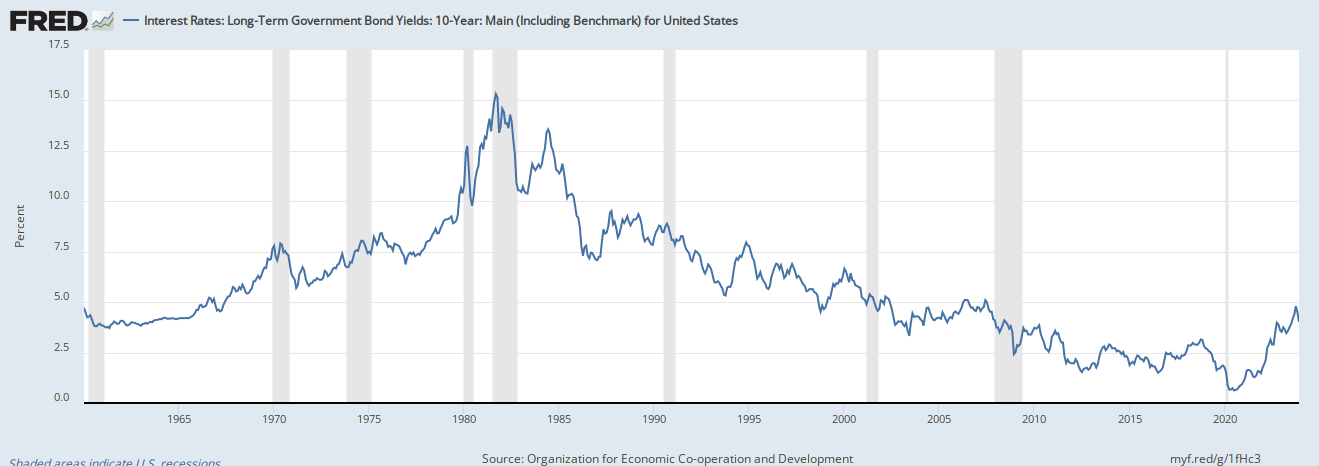

The yield curve is inverted, which does not happen too frequently. If it does, it forecasts recession with quite some certainty.

Past performance…

This highlights how people lost ‘situal awareness’ of where we were with interest rates. Relying on recently bias and simply mantras:

“interest rates always go down” => “floating rate always beats fixed rate”

Not realising where we were on the chart. You show the 10 year here almost getting to zero.

Sure, maybe some people did actually take this to the logical conclusion and say “you know what this is going to keep going down until it goes negative and the bank is going to pay me interest”.

Someone more sensible might have said “if this isn’t the lowest mortgage rates are ever going to get, it is damn well close enough that I should grab it now.”

3 Likes

I do not think that this is necessarily true, banks can completely hedge this risk with interest rate swaps. Because of that, you can also look up the implicit margin by subtracting the swap rate (with the same duration) from the rate of a fixed rate mortgage. In my experience, these margins are not higher than the ones of SARON mortgages.

A SARON mortgage is cheaper than a fixed rate mortgage if the avg. rate is lower than the current market expectation over the time span, which is off course very hard to predict.

1 Like

Costs / any premium (e.g. a term premium) are incorporated into the swap rate, the bank pays this fixed rate to another party and receives SARON payments for it. So yes, I guess there is some hidden hedging cost within the swap rate. No idea how high that is, but it looks like there are researchers that try to estimate it using various (non-trivial) techniques, e.g.: JRFM | Free Full-Text | Term Premia in Norwegian Interest Rate Swaps

2 Likes

As mentioned, in practice long term mortgages are implemented with swaps. This should be relatively efficient as the market will match those who want to swap fixed for floating and vice versa with each other.

And for every market participant who is betting on higher future rates (or hedging as you call it ![]() ) there’s another betting on lower future rates (or who are also be hedging against their own floating rate liabilities).

) there’s another betting on lower future rates (or who are also be hedging against their own floating rate liabilities).

Whether one is ultimately more expensive than the other to the homebuying consumer, I don’t know. I guess this is also a competitive market so the banks can charge what they can get away with.

2 Likes

More precisely, the market thinks inflation pressure will subside, and therefore SNB will lower the interest rates vs today.

Inflation subsiding often happens during a recession but it is not always the case. Hence economists currently discussing whether or not the US Fed has pulled off a soft landing in the US

2 Likes

Hello all, and sorry for the off-topic a bit question but how the interest rate of Saron is calculated? I understand there is a portion of the compounded overnight Saron interest rate over the last three months (where and how can I find that?) plus the fixed margin % (around 1%) that you negotiate with the bank, correct?