Monkey brain is happy.

Monkey brain hasn’t filled the tax statements yet, but that shouldn’t be a big deal since taxes would have been to be paid anyway.

I’m happy but I won’t put too much % on those ETFs because at the end of the day I’m still too poor and can’t live off dividends. I also have JEPI and I’m still monitoring it to see if it’s less volatile than other stocks only ETFs.

I also have chdvd that behaves like chspi so I’m happy there as well.

I guess the nuance is that if divies are 60-70% of your total return (as is the case with the JEPx ETFs) vs 1-2% then one’s losing a lot more to taxes than they could, but as long as one is aware and ok with it it doesn’t matter.

You are basically saying that the virtual dividend of IcTax are way lower than what they “should be”?

That might be correct, but it all depends on what you want to hold. Like if I don’t believe in dividends I should sell CHDVD and get SPICHA, but they are two different products so at the end it’s not the dividend the problem, but which company you believe in. The topic will slowly shift to a different topic. If you have the same ETF div and acc , then you can try to calculate that, but everything else is difficult/impossible or illogical.

Anyway I won’t have that much invested in those ETFs, not even at a later stage of life.

No, just that if you’re holding non-income focused products you’re not taxed on any on-paper or realised capitals gains (and dividends which are taxable are a much smaller part of total return), while if you hold income products the dividend distributions, which are fully taxable, are a far bigger part of total return. This is the argument against dividends in Switzerland.

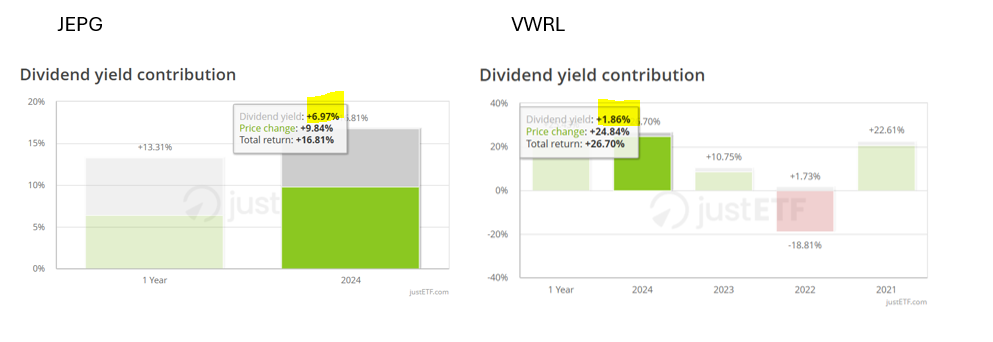

If you look at JEPG vs VWRL side by side, the highlighted part is the taxable part, 40% of JEPG’s return is taxable, while only 7% is taxable for VWRL.

I agree that VWRL and JEPG are different products, with different goals, and both work pretty well at what they’re designed to do, so it’s up to the investor to look at what they want to get out of it. Talking personally, in a situation where UCITS ETFs and their dividends are fully tax-free, and I have enough to invest in JEPG to fund my life, I’d ditch VWRL in an instant (maybe save some for my kids). Until then there’s no good reason for me to get JEPG.

I’m just longing for the day I will switch to these ETFs being what’s covering my living expenses and then some, but it’s far.

I didn’t think about that. Both have dividends, so the Confederation cannot invent taxes on them (for now). you get that 1.86% taxed. If VWRL wouldn’t have had a dividend, they might invent taxes for more than that. I always thought about ACC vs DIV.

I need to relocate to live with dividends. Or wait.

Talking of dividend ETFs, I bought 5k USD of FUSD about a year ago to see how it’ll go and now thinking of ditching it as I’m still in profit with it. My original plan was to see how it’ll go and then keep adding to it but it’s had 4 years without a dividend increase which is making it a dog in my eyes.

… and also still talking about dividend ETFs I bought TDIV around 2 years ago as my waiting stash for paying taxes, quite happy with it especially lately as the EU stock market has been doing well. Dividend is stable around 4-5% per year. Probably the only downside is it’s home country (NL), I believe this is not optimal for WHT compared to IE.

That’s the only reason I didn’t get it, to be honest, I too “believe” the same but have not done research to back the belief up. Have you? If yes it’d be good to record here.

I didn’t do any research here on the WHT difference disadvantage. I don’t understand too much about the differences of WHT between different countries and to be honest it does not interest me to dig that deep

So I did the research, NL-domiciled ETFs need to withhold 15% dividends paid out (while IE withhold nothing). Private investors domiciled in CH appear to not be able to reclaim it, if I understand this form and point 17 correctly, pension funds can.

Right, not the same thing (ie getting a refund from an ex-CH country) but the result could be the same, and likely easier/faster than getting money from abroad. Good to know.

Hi THE5Z, are you still happy with the dividend coming from MSTY and UTLY ? I am considering to start buying into MSTY, however the dividends from ULTY seem to have depleted quickly…would be great to have an update from you.

Currently the dividends help me with the market downturn. I’ve just run a total return analysis (dividends vs downturn). for example I have received from MSTY 4,220.77 USD in Dividends, and in this current market I am down -4,085.20 USD (before taxes) so not a bad investment. ULTI and RDTE are currently my worst investments, there I am 1’000 USD short.

But I keep receiving the dividends, and it doesn’t matter what the market does. it is currently around 2’200 USD per month, So I am happy.

Unfortunatly I can’t invest more in the market, because as i’ve written in my first post last year I am going to study abroad in the summer, so I need the money. I’m putting my spare money into a normal bankaccoun, just to be safe.

But If I had the money, I think I would’t put money into ULTY. The payout is steady, but the NAV-Erosion is big. MSTY is holding quite well, also XDTE and QDTE. Since I am in this experiment the most steady where allways the Roundhill-ETFs. So in the future I am going to invest in them.

Thanks for this update. So you do NOT reinvest (DRIP) your monthly dividends, right ?

Roundhill-ETFs seem to yield way less than MSTY and ULTY.

Can you share some details on the taxation, assuming you are based in CH ?

I guess US Withholding Tax is 30% on the dividends and you file for 15% tax return via form DA-1 with ESTV ?

I am just wondering if it this dividend strategy is worthwile after deducting taxes.

Whats your call on this ?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.