5 Likes

As an example, as of time of writing I see my VT down 0.8%, but that is balanced by SCHD up 1.55%, SCHY up 1.15% and BRK/B up 2.8% so my portfolio is now up 0.21% today. I see this pattern quite a lot, and I think it is because the Mag 7 and tech have such a weight in VT that bad news in tech stocks often has a rotation to consumer stables, healthcare etc.

3 Likes

Factor investing theory says that certain systematic characteristics (“factors” like size, value, profitability, momentum) have delivered higher long-term expected returns than the broad market, historically and across markets.

Those higher expected returns usually come with higher risk, different risk, or periods of severe underperformance — which shows up as higher volatility, deeper drawdowns, or long stretches of disappointment.

So higher long term expected returns for value etfs can work aside efficient markets theory.

The mechanical SCHD methods seem to work better, goes through the roof at the moment:

Somebody pointed to an UBS research paper which did analyze factors for the last 200 years or so. They all had periods of under performance, the one with the least of those periods was momentum. That is my experience too.

But then factors are a really nice vehicle to be combined. I use “value” and “momentum” in all my strategies, the dividend strategy uses “carry”. But I use the factors in a non-standard way, want to be original… ![]()

I wasn’t exactly serious, very high yield products are rarely good strategies.

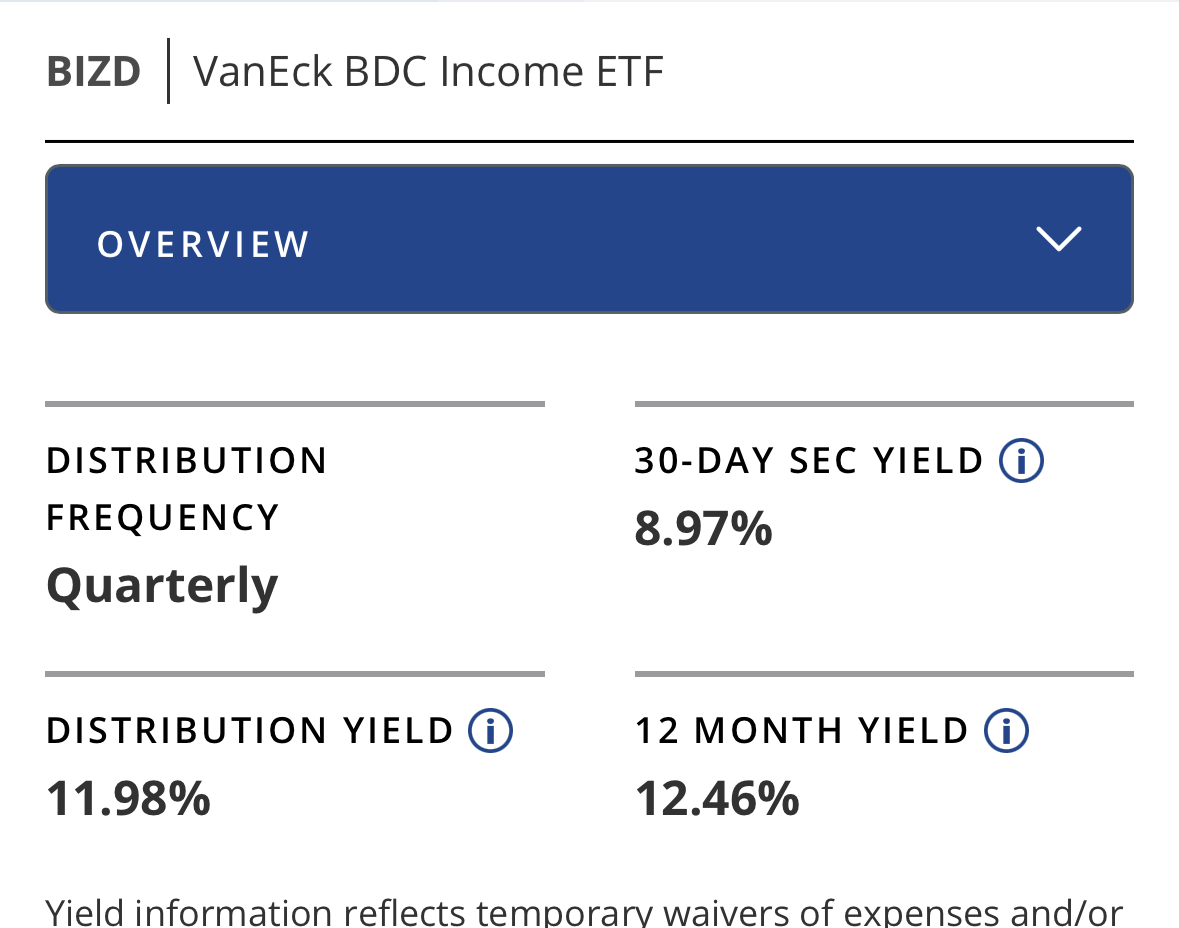

Has anyone looked at GPIX or GPIQ as income generating ETFs?

the yield is around 8-10% with dynamic covered call writing. I know it limits upside participation but investing 5% of my NW in these ETFs could generate a cashflow that might pay a substantial portion of my mortgage interest.

or staking capital in this would be too risky?

Well, you know we’re in the monkey thread, so there’s an element of…monkeying around with numbers AKA mental accounting.

If you mean that you’d mentally segregate the % allocated to these sort of funds to cover interest payments, then go for it. It may be that staying invested in broad index funds and selling as and when needed may turn out to have been less risky (= you end up with more money than the CC fund option) in the long term, but keywords are “may turn out to have been” - AKA crystal ball, nobody knows.

Knowing myself, covering the occasional car loan interest payment with dividends is something I find deeply satisfying, because in my monkey brain that cash is free money.

2 Likes

I would add that whatever you do with <=5% for your portfolio will not have a big impact anyway. So if it makes you feel better and stay on course, go for it.

(Personally, I would just sell whenever was required to pay the interest, as it is optimal and there is no psychological benefit of doing it differently anyway)

I usually check the volatility. The first (dumb) thing I’ve done is to compare the graph of it vs VT and VTI and I don’t see less volatility. Maybe I should compare with JEPI too. So it’s just a monkey-brain ETF and how it’s build doesn’t matter.

yes, it is comparable to JEPI or SPXI

it is not 5% of my invested portfolio but rather 5% of my net worth. This money and a bit more has been lying in a high savings CHF ![]() (1%) account for a while now and I think I could use to it generate a bit more cash flow. I know I cannot compare this to a safe investment like a savings account then also keeping a sizeable portion of cash has only been detrimental in the long run.

(1%) account for a while now and I think I could use to it generate a bit more cash flow. I know I cannot compare this to a safe investment like a savings account then also keeping a sizeable portion of cash has only been detrimental in the long run.

I have read a bit about CC ETFs but apart from NAV decay, are there any other downsides?

How does tax reporting work for these? anyone had any experience as I could not find these ones in ICTAX

@JEPG had pulled the ICTax table for JEPI (I think), and it looks like only a small % of the distributions is taxed.

I don’t see much NAV decay with JEPI and the like, NAV decay you get with the silly ULTY type funds, but these are meme “funds”.

Somewhere on this thread it’s written how they are expected to behave in various market conditions but the gist of it is that in flat markets they may overperfom the underlying, in bull markets they definitely underperform, and in bear markets the loss is somewhat buffered by increased distributions (overall, distributions go up in times of higher volatility).

1 Like

JEPI and JEPG are on ictax in their ucits version and most of the yield is capital gain (option premium are, dividends from the position it’s long aren’t).

However it trails sp500 or vwrl A LOT, in terms of total return, yield reinvested. So you have a stock etf, no diversification, no downside protection, capped upside. And a nice monkey yield.

3 Likes

thanks!

yes, I could see JEPI and JEPG in ICTAX

I could not fix GPIX and GPIQ, the 2 that interest me the most.

What could be other income generating ETFs? mixing CC ETFs with cash secured Puts ETFs?

I’m curious if any div/yield enthusiasts, especially when it’s a side “small part” investment to cover mortgage/loan/holiday/feed-the-monkey money, would be ready to “park” that in a classic but dedicated equity portfolio and withdraw from it / same expected amount as the yield product would produce.

According to…hum…theory…it should get better results.

If the practice of withdrawing -good training for fire btw- by selling / transferring / spending is too cumbersome, the experiment could be done with the cheapest robo and a recurring monthly withdrawal order from it. You forget about it and just enjoy the money in your bank account every month.

Monkeyfying the (growth?) equity portfolio.

I wonder if the anti-divi investors would just let their portfolio grow and margin against it for spending instead of manufacturing dividends by selling?

That’s more engineering and margin has to be eventually refund, or you’d have to live with debt.

Monkey brain can’t be fed this way.

I’m quite convinced that part of the psychology of not selling is also practical. Place an order, pay fees, even small, trigger the action that makes you “lose” / “decrease” units, think of rebalancing if your PF is not a one-etf thing, think of your future pain filing your tax return if not automated (etax statement), doubt if it’s the right time to sell,… these are obstacles. And it eats the monkey brain.

while the div just looks like a freshly laid egg with nothing to do. You keep your number of shares, it just “produces” money.

However, according to, hum, theory*, you’re better off if you invest in broadly diversified equities instead of chasing yield, whether you compound or spend.

I don’t want to initiate the debate, we’re in the monkey thread, but if my feeling is right about the “in practice withdrawal is a hindrance and eats the monkey” for most,

I suggested an alternative, best of both worlds?: instead of putting 100K in some high yielding product, put them in a broadly diversified portfolio at VIAC/Finpension/TW/whatever the cheapest, and set a quarterly 875 CHF (3.5%) standing order to your main account and never touch the investment again.

Use your “div” for your spending or saving into your main PF.

Monkey is happy and your investment should not be depleted over time and it’s frictionless in practice.

* Ben Felix has made simulations on both scenario comparing sp500 and CC ETF whether it’s reinvested or spent, CC never wins.

2 Likes

Exactly, I mean live with the debt. 100% stock people are anyway saying that stocks outperform bonds, so just let their stock portfolio continually outrun the mounting debt.

2 Likes

but with some dynamic CC ETFs (NEOS, GS) the yields are much higher (~10%) and their call writing strategy is more dynamic than a fixed one with (JEPI etc.)

the Ben Felix video compares the fixed (100% call writing on assets) to buy and hold ETFs (again I am not an expert here so can miss on nuances)

But let’s say if someone invests 100k in both of these options - CC ETFs and periodic withdrawal using a robo advisor (the idea being it should be automatic to get the cash flows), which one would be better say for a 5 year horizon and 10 year horizon?

I still think CC would provide a better outcome as taking 10% from a buy and hold is diluting the underlying too much too quickly.

For a 3-4% return, the winning strategy could be different.