Same for IBKR. So annoying. And stupid from Vanguard to have moved the payment dates of their ETF.

Let’s see how ICTax will handle this dividend.

Same for IBKR. So annoying. And stupid from Vanguard to have moved the payment dates of their ETF.

Let’s see how ICTax will handle this dividend.

Realistically and officially it’s the ex-dividend date that matters though.

From the Swiss tax perspective, it seems it’s actually the official payment date that matters, not the ex-dividend date. However, as the official payment date is still in the same tax year as the ex-dividend date, this doesn’t change anything in this case.

Right, they showed on the account today but the transaction document was generated on the 31st. Doesn’t really matter ![]()

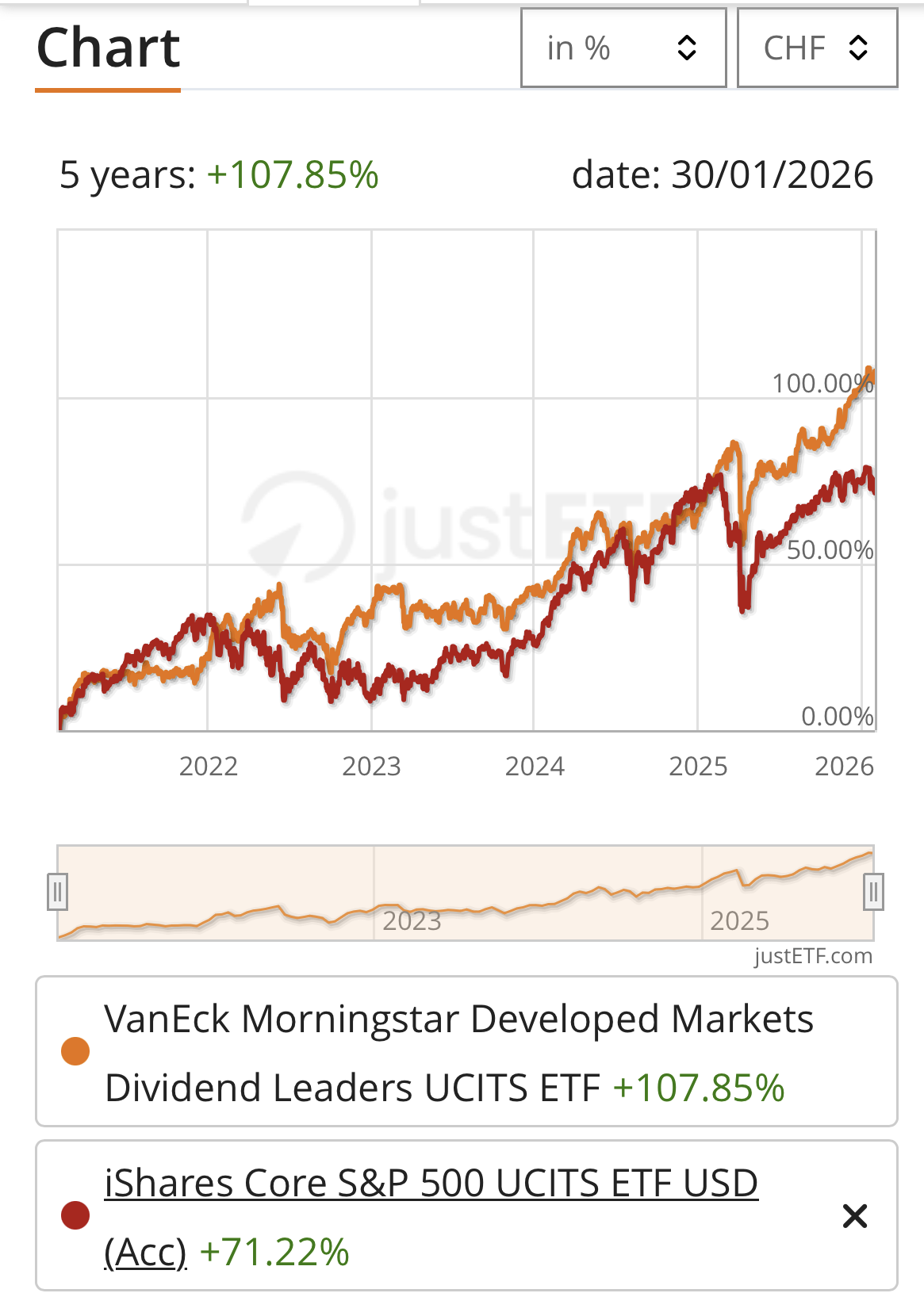

Surprised how TDIV, a dividend world etf, crushed SP500, more growth oriented and us-only, on perf, vol, for the last 5 years. Same compared with nasdaq.

A longer history shows different, but 2022 and 2025 went well.

I’m on ISPA and thinking about switching to TDIV

How y’all justify your alloc in Tdiv/schd/dividend products in addition to an existing world allocation? You certainly hold and overlap stocks? A tilt to feed the monkey brain? Any other targets when buying this?

TDIV for me would be sexy for all the wrong reasons:

EUR dividends may be practical for me… mid term future => if it’s not of use today, I should not care.

I hold EUR in a fixed term deposit part of my cash allocation (bit of history here, they’ve never been something else), and TDIV is mostly traded in EUR if I want to invest them => may as well switch currency to whatever is convenient to trade/hold, incl. consider feeding chf cash allocation if I don’t want to change my asset allocation (but I definitely trust CHF better for cash).

I like the recent past performance => which of course predicts the near and far future (irony inside).

monkey brain income

Longterm, I aim to have 25% SCHD, 25% SCHY and 50% VT.

Currently, half of my portfolio is in META and AMD, I plan to sell them in couple of years and put them into the above mentioned ETFs.

When checking the TER, the diversification, the balance of growth and quality, and other factorys - for me - this is the perfect set-up. I also checked other ratios, but 25/25/50 is quite perfect.

Focus for SCHD and SCHY are quality companies, and not high dividends per se. The ex-USA of SCHY is a welcomed construct.

Of my US IRA rollover account (dividends should not be taxed as it is pension fund with access restrictions), I have about 11% of my porfolio in SCHD and 11% in SCHY. SCHD was purchased just before the April mini-crash and has gained 13.1%, SCHY in early November and gained 13.6%. Both yields are similar.

I purchased both not for the dividends per-se, but the quality aspects of the constituent companies as a hedge against over-valued tech companies. I’m hoping to trade reduced returns with reduced volatility. But in fact, the returns of these fund are quite good. Similarly I have about 13% of the portfolio in BRK.B but this has been pretty dire, down 8% in 1Y, but it might soften the blow in a crash.

Indeed. And if you consider also the tax drag of almost 5% dividend (not counted below) things are even worse.

But OK… this is not an apples to apples comparison.

PS interesting to see that if you click on the 1Y, 3Y, 5Y, MAX buttons the lines swap every time. Once again the power of cherry picking the start time!

My justification for also buying this ETF although there is some overlap with other ETFs I have (VT) is that I use it from time to pay tax bills and the EUR dividend is practical for holidays in Europe. I also very much like the aspect that it works so far as growth+income ETF. A lot of other dividend focused ETFs are pretty much stagnating. Let’s see if it continues like that, my wild guess for the recent out-performance last 2 years would maybe be because this ETF holds quite some European stocks which went well (and even a bunch of JP).

Look at the thread title!

No, seriously, the dividend CAGR of SCHD is extremely attractive if one hasn’t got the skill or the guts to pick stocks. The narrative of “buy, reinvest, switch to consuming when the time comes” is extremely powerful for some people (myself included) who find the prospect of selling very stressful!

@mabi what are WHTs like? Do you (manage to) reclaim WHTs? I remember looking at it at some point but it looked complicated and iffy.

I never really had the courage let’s say it like that to look into this topic. For now all I know is that the dividends get taxed 15% directly but no clue how to reclaim that or even possible. For now I didn’t bother mostly because the amount is not too much but as a mustachian would say it’s another story over 10+ years….

I see, if you scroll above here and around there’s some discussion, I even see I asked you this before, sorry for that!

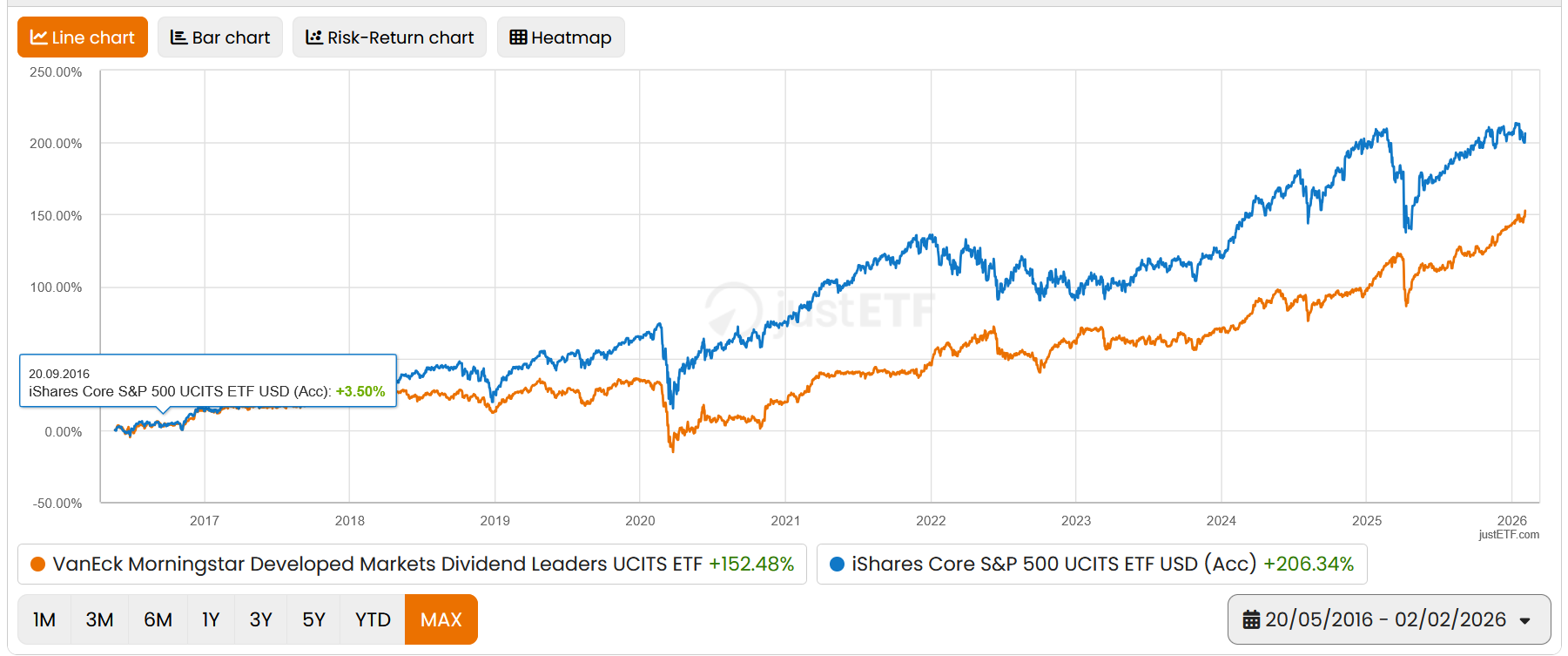

You have dividend tax also with s&p500. But yes, sp500 10y beats TDIV on NAV by almost x3.

5Y VanEck is still ahead though, not counting distribution ![]()

Assuming 30% marginal rate (and no other taxes, for simplicity)

S&P 500 tax drag: ~1.5% *30% = -0.45%

TDIV tax drag: ~5.0% *30% = -1.5%

You lose ~1% per year.

Totally worth it if one cannot stay invested without the dividends kicking in.

(I am in the Monkey-brain ETFs: Dividend ETFs topic. I don’t want to start a war I will lose ![]() )

)

That makes me think I should avoid dividends with my marginal tax rate. Even Swiss wht looks sexy comparing to what’s coming afterwards ![]()

Maybe I should buy JEPG ![]()

That is my main point about “high dividends investing”. Paying too much without personally providing a behavior safety net.

PS Thinking about it - that remains to be seen next time we have -50% drop and/or we are in red for 10 years… ![]()

Basically what attracts me is more likely this:

(That’s also why I won’t buy JEPG)

Likewise, the often missed nuance among less sophisticated people (not here!) is that the only similarity of covered calls and dividends is that they’re paid in cash.