Today my momentum system made me do things I hate: sell perfectly good stocks! I had to sell two financial companies, Bread financial and Allstate. Both with a nice gain of 30% each and both I really liked. Easy, no problem stocks. And I have a lot of stocks I would have liked to sell in an instant but they either are with me less than 6 months or they are still on “buy”.

So I did what my captain said and probably it will be the same as ever: the more I hate what I have to do the more money I make.

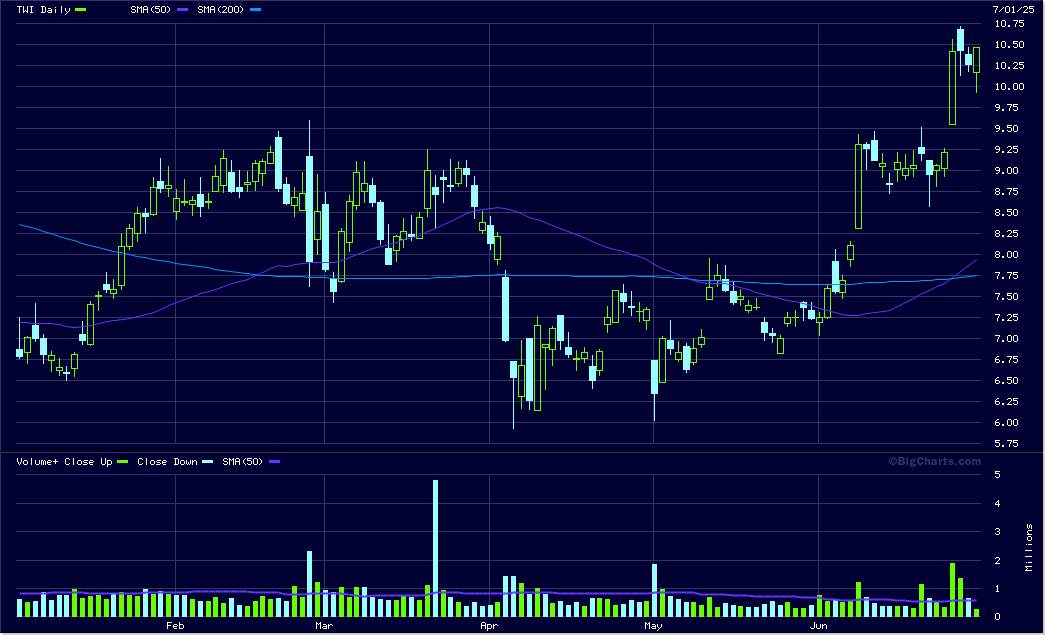

BFH and ALL were pushed out by Titan international, TWI. Big big tires:

Do you sometimes change your momentum strategy, or least analyse its performance compared to tweaked models?

I understand sticking to the plan and not letting emotions override sense, but maybe your gut feeling has something to it? Do you do some reviews compared to “what you would like to have done” and adjust if it makes sense?

No, absolutely not. The biggest gains (2000% and more) came from exactly such situations, stocks I would never touch if listening to my guts.

Sticking to the plan is essential. I did backtests, but backtests are basically useless. Then I did forward tests for almost a decade. I did not want to start before I was sure I understand what will happen. And, of course, before I had money that I could afford to lose but still enough that it is worth the effort.

The first year, 2020, was a loss while all the index made tons of money. I knew that can happen, low correlation to index. I did stuck to the plan and it paid out very nice. It is only 5.5 years, but even such a short time at 27.41% XIRR has a very nice compounding effect.

The risk is extreme, don’t do this at home! Many experts will tell you that using margin on stocks is suicide. I have quite an original way of using margin, the cheaper stocks are the more margin I use. That is contrarian investing, exactly the opposite that the crowd does. Contrarian investing in a momentum strategy… works.

Everything can be improved, always. I did some small changes, mainly in money management. For example, I do now partial sells after 500%, 1000%, 1500% and so on. Wish I would have done that earlier.

The strategy is optimized for my personal situation, I need some form of cash flow. I think everybody should construct a mechanical strategy for the personal situation. One or more, as I do. The strategy may not be perfect but it is a perfect complement to my dividend strategy and both together are perfect for my personal situation.

Just to repeat, how to construct a mechanical strategy: 1. Define a vision. 2. Define money and position management. 3. Define stock picking.

Test, test, test. And then, most important: stick to it!

Curious on specifically this -

How did you size up the portions to sell at these thresholds?

(I did something similar as some of individual stocks grew, but more of with an approx principle of "let’s get back what I invested x2 and let the rest run)

I sell so the position still grows a little. Obviously the first mark is the most difficult to reach. 500% is usually a windfall profit. My table goes like this:

But I actually never reached 2600%. At those marks I can sell 20% and the position still grows a little. Of course after the first sell I already get back my initial investment. Those tend to be very volatile stocks and this way at least I have the illusion that I cannot lose anymore. Which of course is not true…

Today the captain told me to do things I like more: for my momentum portfolio I sold Marcus which was a loser and I bought an obscure and very small tech, that in theory is in a place that should have worked out fine for many years. Seems it starts to work out now, but who knows.

And again I had to re-invest dividends in the dividend strategy. As you all know I don’t like cash. Bought JNJ at close for $155.27.

I thought I need a new car, so I would get a little debt and not need to reinvest dividends every few days. But I drive my current car now only for 21 years and I really like that car. I will continue driving it. My mechanic says it will make a million kilometers and it has only 220’000 now…

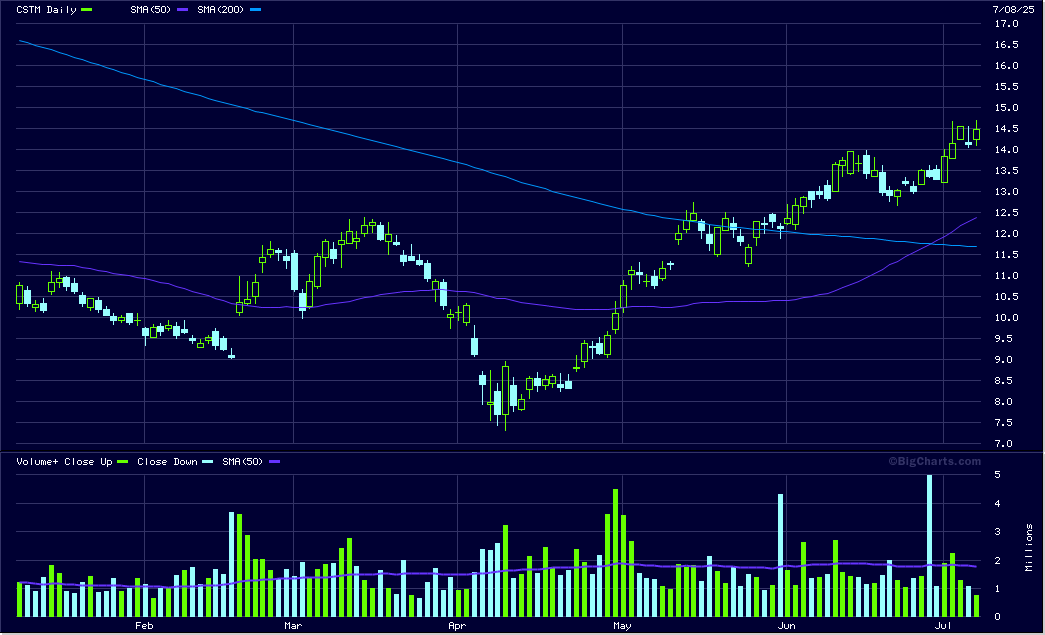

Today I had to buy for my momentum strategy Constellium (CSTM). The aluminium giant to which ex Alusuisse belongs almost doubled in price the last months, nice momentum.

e-Health (ehth) was pushed out… finally. I hate Kreisschreiben 36 sometimes, having to hold such a loser for 6 months is hard. Lost like 57% on it.

I did read a few good books about investments last months. I did read hundreds of books about this theme during the last 45 years.

I was wondering if there are some good books about mechanical investment strategies. I searched the Internet and found some, but they are far from describing how to construct a real world mechanical investment strategy as I did here.

In my opinion you need mechanical money- and position management and mechanical or half mechanical stock picking. No book I found describes the complete story. Probably it is because it works; whatever you may gain from writing a book about it is peanuts compared with what you gain using it.

Hedge funds do it, index do it, ETF do it. I do it. Why there are no books about it? Because it works.

Today I love the taxman! Because of Kreisschreiben 36 I kept holding KLG which was on sell since a few months. Seems it will be bought by Ferrero, price appreciated 50% tonight.

Thanks Kaspar Villiger, you were the best (after the Appenzeller Hansruedi Merz with the Bündnerfleisch, of course) !

I defined a vision: Accumulate savings and achieve long-term returns above saving account interest rates or government bonds.

Defined money/position management: I have money each month from salary that gets invested; position is world ETF (market cap based). Gets sold once I do not receive salary anymore or decide that in the foreseeable future I will want to spend some of the money

I let the ETF managers do the stock picking of what to include or what not (I know you criticized how they do this a few times on this forum; but I believe it is still better than me spending time trying to be more clever than them.

Now would you still call my strategy “mechanical”? Or if not, due to imperfect rule following by the fund managers, would you call it “mechanical” if they did 100% follow transparent rule sets? Or is a mechanical investor only someone who does come up with the rules themselves?

You avoid behavioral errors from your site. So yes, I would call it mechanical.

I don’t know about the ETF you are using, but I suppose it uses mechanical stock picking based on some diversification rules and market cap? But that you should probably investigate before you start investing in it.

As I said before, I am absolutely not against ETF investing. For many people it is the best they can do. You avoid expensive errors all of us commit, even I did.

And it seems you have a mechanical money and position management.

Just got my account from AHV with all the nice numbers. Couldn’t help but do some statistics: per year I made 185% from my mechanical investment strategies of what I made working. Just simple average, total money made divided by years. OK, not simple because on the stocks income the tax is already deducted while the AHV account is gross, social security and tax would have to be deducted. And of course it was a lot of years working and the investments I only count since 2014, after investing my 2nd and 3rd pillar money myself. It is not inflation adjusted. Just playing around.

Nice, stopping to work gave me a theoretical raise of 85% of my salary.

Please don’t remind us again of the horrible performance of the second pillar. My 3A is outpacing my PF by a large margin while receiving much smaller contributions (Yes I know 3A doesn’t have the insurance built-in but still)…

Depends on the pension fund. I hate that I have/had no control over it. I did add tons of risk when I could because my individual situation allows me to.

And we did only have 3 losing years since I started. Pension funds per definition have none. That insurance does not come for free.

Wouldn’t it be nice everybody could decide for himself? I did, but I had to stop working and leave Switzerland to do so…

Back to topic: my strategies performed nice, but nobody knows the future. I still have heaps of risk, but I sleep like a baby.

How do you know when the risk is right? You make a lot of money and you sleep at night!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.