OK, it is important because most index investors think they are immune to behavioral risk. But that is only true if the underlying index for the ETF is constructed mechanically and adheres to its own rules. What for you have rules if you don’t adhere to it or change it for no good reason?

I did read the SP500 example in a book recently, will do some more research, even if that means I probably have to mention it for the 11th time, sorry.

Actually this kind of research should be done by everybody who invests in an index ETF, as I said. I don’t, but as a favor I’ll try to find time for some research.

OK, before I search for the examples the google AI gives quiet good answer to the question “how does SP500 stock selection work”. It is a combination of objective criteria and subjective decisions of a committee, while the subjective decisions overweight the objective criteria.

In other words: you replace your own bias with the bias of that committee and it has nothing to do with an average, what is what most index investors look for. The committee has proven that it falls for FOMO in bubbles and that hurts performance.

Not world ending, but unnecessary losses due to behavioral risk that is not compensated.

Are you sure that Yahoo and Tesla are the only examples? Anyhow, the committee should not only be unbiased and adhere to the rules… if the rules are robust enough there is absolutely no need for a committee. I think the Nasdaq100 works that way (there are other problems there…).

I think at the end of the internet bubble the rule that companies must have been profitable for 12 months was overruled, probably several times. Will check the book where I did read those samples later. Typical FOMO bias error, you would not expect this as an index investor.

Wow, computers make life easy. Found the book, “The Laws of Wealth” by Daniel Crosby. In part 2 he explains why the SP500 is far from being passive, passive in name only. Even the membership of its committee is a secret. They did public some of their rules, but constantly did break them. The SP500 is even compared with an actively managed fund!

1995, when it would have made a lot of money to include Nasdaq stocks, only 4 were contained in the SP500. However, 2000 at the high of the bubble almost half of the additions, 24 of 58, were tech stocks at its high. FOMO in action. Many of those stocks did not adhere to the rule of at least 12 months of profitable business.

That is exactly what I meant. With SP500 you buy a black box with a proven record of behavioral bias. It is not an average and it is far from being passive. But, as most of the investment community (including myself) compare performance to this index, it does not really matter. Or does it?

Follow momentum strategy (self made)

Follow S&P momentum index

Follow S&P 500

For World ETF

I don’t think anyone is going to get more than 4-6% per annum real returns over a 20-30 year period . And if they do then they should consider themselves lucky and not anything else. In fact I think it would be even lower because everyone seems to think Stocks are Fixed deposits and pay high and high multiples for earnings

So I think the there shouldn’t be debate about what’s better (index, rules based investment, fundamentals driven investing , technical trading). In the end the question is what’s better for you as an investor. Whatever works , works

But you should know what you are betting on. That is exactly what i meant by “you should do your research”. If you want to be a passive investor look for a real passive index. A rule based index without a biased committee. The committee is either biased or it is unneeded. It is biased because we all are, there is no way we can get rid of the over 100 bias that hurt our performance when investing.

I did choose mechanical investment, I create my own index. But there are more index than stocks, as I mentioned before. Many of those index are constructed mechanically. That is what I would look for as an index investor.

However, this is only applicable to the US portion of your stocks. If your portfolio is diversified across other countries, wouldn’t it make more sense to use a MSCI World or ACWI index (or comparable FTSE indices) for comparison? Alternatively, you could use a world momentum or world dividend index for your strategies as comparison.

Actually any comparison does not make sense, as I construct my own index. I compare just for fun and it is not always fun. Remember, I had a loss in 2020 in my momentum strategy when the indices made tons of money.

A bit action today in my momentum strategy. Sold Fresh Del Monte and Pulte Homes (0.5% thanks to dividend and the last lot of Pulte with still 81.9% gain).

They were pushed out by the new entry, the Brazilian Fintec PagSeguro (PAGS):

And my dividend strategy did deliver a nice market dividend from Broadcom today. I did pay off the rest of the debt in this strategy and with the rest I bought more HST and PFG according to my mechanical rules.

This year only IBM and Broadcom did deliver a market dividend until now. Market dividends are positions that reach 6% of my portfolio value and I then sell down to 5%.

Don’t like it too much, now I need to buy something more with the next dividends. Or takeout some money. Luxury problems…

Depends on the strategy. In my dividend strategy I only take on debt when I need to take out money or in a bear market, the crash recovery protocol as described earlier. The debt is then paid off by dividends, market dividends and sales.

In my risky momentum strategy I always have debt. The size depends on the actual SP500 compared with its last high. I calculate two margin multipliers, one with and one without unrealized gains. The formula then goes like this:

- Leverage: MIN(150% + ((SP500 high - SP500 actual) * 3), 300%).

sell:

margin 1 = without unrealized gains, margin 2 = with unrealized gains.

when over margin 2 sell until under margin 2.

when over margin 1 but still under margin 2 sell same amount as buying

Actually the momentum strategy is at a margin multiplier of only 133% because there is quiet some unrealized gain.

And a wonderful stock market june finished right now. Portfolio and many positions at all-time high. Here my monthly report:

Dividend strategy: as I have no more debt I did need to buy something today, I don’t like cash. My system made me buy some General Mills. Tons of dividends this month, that are the symbols that paid: F,CMI,EMR,IBM,JNJ,MET,TRI,PRU,O,KLG.DD,VTRS,GILD,LMT,PFG and AVGO.

The net performance YTD is at 5.78%, XIRR since 2014 10.35% and since 2020 12.86%

With the buy today the margin multiplier is at 100.13%, almost no debt. The carry premium is at 5.23% of the actual value of this portfolio. The carry premium is dividends minus tax minus debt interest plus market dividends per year in percentage of the actual portfolio value.

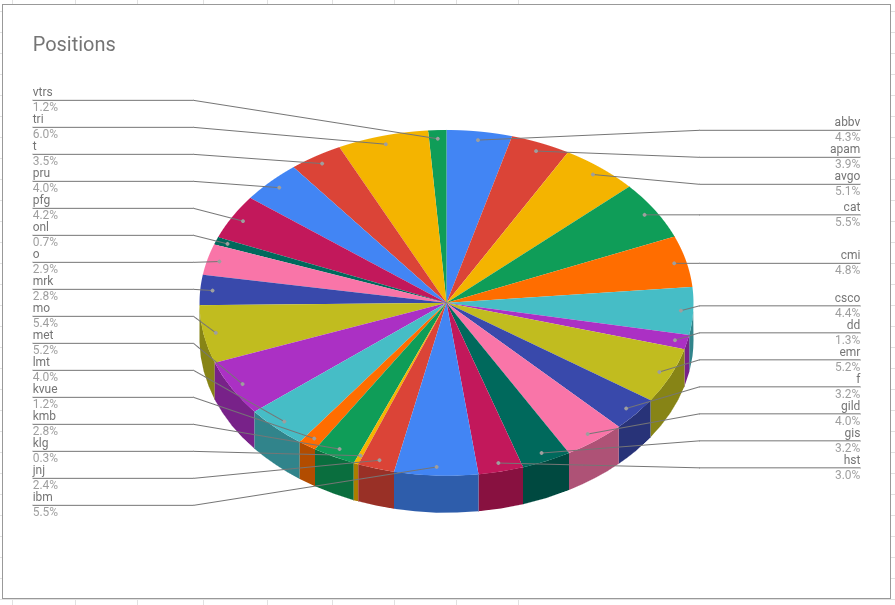

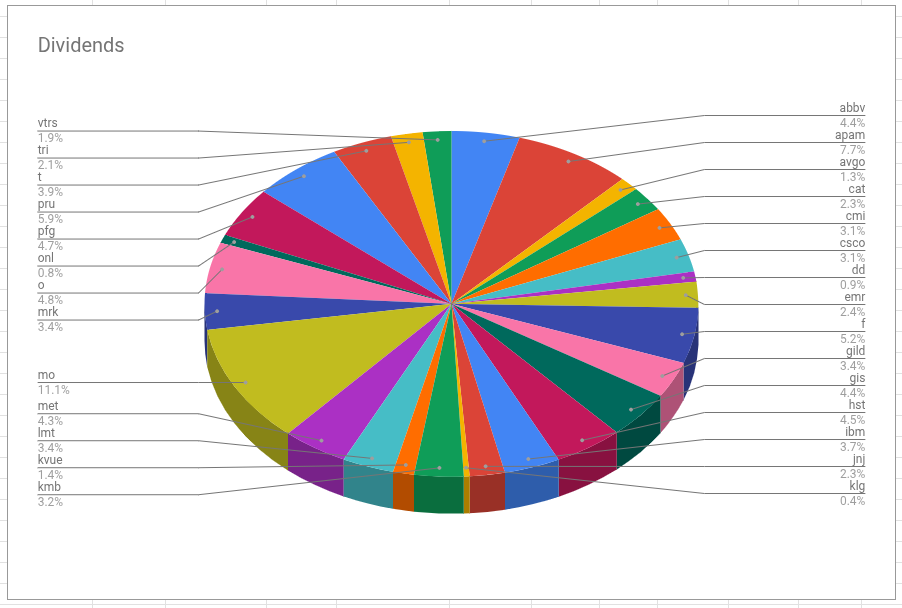

Here are the wheels of fortune of the dividend income and of the positions:

The momentum strategy runs nice too. Performance YTD is at 11.74%, XIRR since 2020 is at breathtaking 27.55%. The actual margin multiplier is at 131.72%. That is relatively low for this strategy because we are at highs. For every percent the SP500 goes down I can add 3% of margin debt multiplier, as the formula in my last post shows.

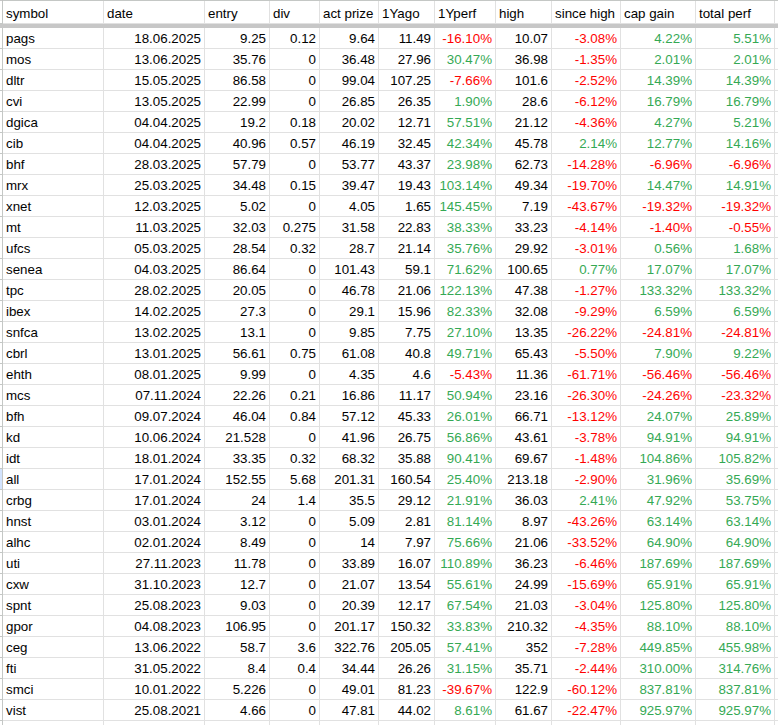

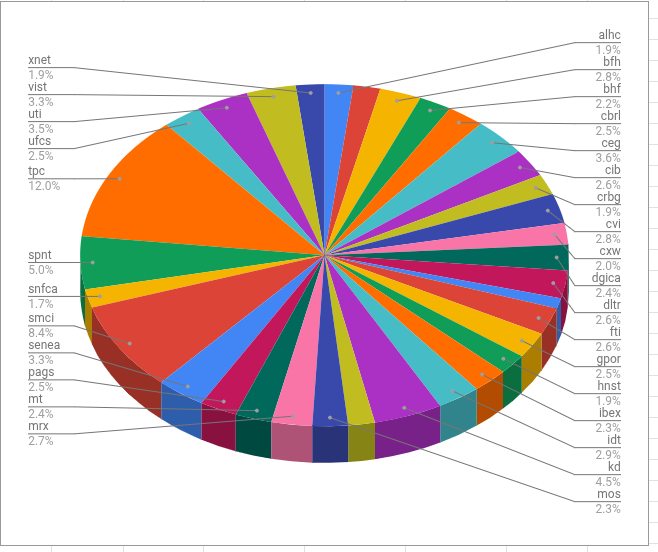

Here is a table with some data I keep of this strategy:

I spend USD, CHF, EUR and a few smaller currencies. Usually I take out on credit whatever I need and pay the credit back sometimes by exchanging USD to whatever currency it was, raising the USD debt (I always have USD debt).

As mentioned, I don’t like cash and the debt protects me from inflation. The USD is now as low as about 14 years ago but the fluctuation is peanuts compared with the performance of the stocks I hold.

I think there was a thread here a short time ago that explained why it is a bad idea to hedge investments currencies. I think it is a really bad idea; depending how you implement it it is expensive or it is a speculation that adds risk.

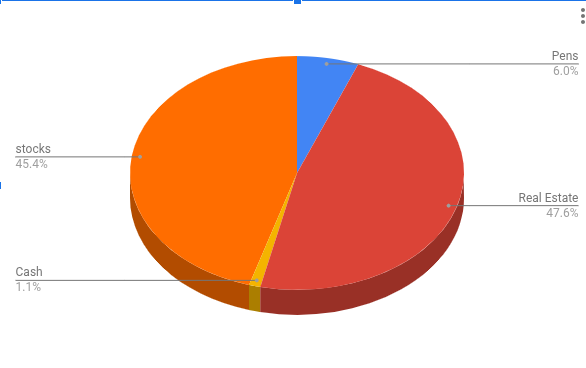

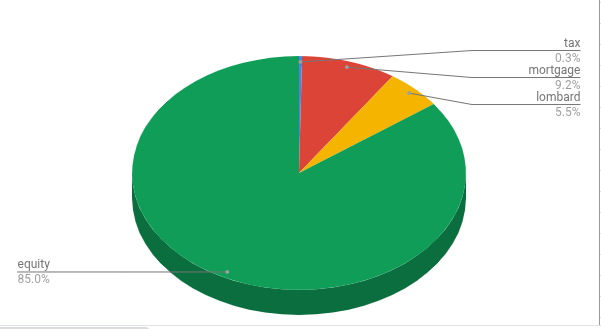

Addendum: I have a balance sheet that I display in various currencies and that includes all my belongings and debt, did not look at it for a long time. CHF, USD and EUR are at all-time highs, but last time I checked was march 2024. Very nice numbers, the real estate is there only at insurance value that did go up last year. Actually I am quiet diversified with currencies, I hold real estate valued in CHF and EUR and stocks valued in USD. I have debt in CHF and USD, but only very little debt in EUR, maybe I should change that.

Did “wheels of fortune” with assets and liabilities and equity, all in CHF, here they are (“pens” is my wife’s 2nd pillar, she still works):

Own use. Did rent out the vacation home when I was younger, but too much work, even it is quiet some money. I like it that I can spontaneously decide where to spend my time.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.